Microdynamics • 227

competition. Finally, we consider how the structure of an industry emerges from the competitive interplay of its member firms.

MICRODYNAMICS

We use the term microdynamics to refer to the unfolding of competition, over time, among a small number of firms. This contrasts with macrodynamics, a term we use to describe the evolution of overall market structure. Chapter 5 discussed two important models of competition among small numbers of firms—the Cournot model of quantity competition and the Bertrand model of price competition. Both of these models were static; firms made decisions simultaneously. Though unrealistic, the models did provide insights into important strategic concepts such as the revenue destruction effect, and the impact of capacity constraints and consumer loyalty on competition. But the static nature of the models clearly limits their ability to help us understand strategic decision making in the real world, where strategies unfold over time. In the first part of this chapter we explore how adding a time dimension affects strategic options, by focusing on the following aspects of microdynamics:

•The Strategic Benefits of Commitment

•The Informational Benefits of Flexibility

•Competitive Discipline

Strategic Commitment

A strategic commitment alters the strategic decisions of rivals.1 As such, it must involve an irreversible decision that is visible, understandable, and credible. The commitment must be irreversible or it carries no commitment weight: the firm can back down if the commitment does not have the desired strategic effect. It must be visible and understandable or rivals will have nothing to react to. It must be credible so that rivals believe the firm will actually carry out the commitment.2

The famous example of Hernán Cortés’s conquest of the Aztec Empire in Mexico illustrates these concepts. When he landed in Mexico in 1518, Cortés ordered his men to burn all but one of his ships. What appeared to be a suicidal act was in fact a move that was purposeful and calculated: by eliminating their only method of retreat, Cortés committed his men to the battle. According to Bernal Diaz del Castillo, who chronicled Cortés’s conquest of the Aztecs, “Cortés said that we could look for no help or assistance except from God for we now had no ships in which to return to Cuba. Therefore we must rely on our own good swords and stout hearts.”3

To explore commitment in the context of models of competition, we shall revisit the Cournot model of quantity competition described in Chapter 5. Recall that the basic facts in that model are as follows: there are two firms (1 and 2) with identical cost functions: TC1 5 10Q1 and TC2 5 10Q2. Market demand is given by P 5 100 2 (Q1 1 Q2). Each firm chooses its output simultaneously and treats its rival’s output choice as fixed. We calculated that the resulting equilibrium quantities, prices, and

profits are Q1 5 Q2 5 30; P1 5 P2 5 40; and 1 5 2 5 $900.

Suppose that instead of choosing quantities simultaneously, firm 1 can commit to Q1 before firm 2 selects Q2. This could occur if firm 1 builds a new factory or signs contracts with workers and suppliers prior to firm 2 taking similar actions. In this

228 • Chapter 7 • Dynamics: Competing Across Time

situation, known as a Stackelberg model, firm 1’s choice of Q1 can influence firm 2’s choice of Q2. To see why, recall that firm 2 chooses Q2 according to the reaction function: Q2 5 45 2 0.5Q1. (See Chapter 5 for the derivation of the reaction function.) The important difference between the Stackelberg model and the Cournot model is that firm 2 does not have to guess the value of Q1. By building its factory first, firm 1 has committed to Q1 and firm 2 knows it.

Because firm 1 can compute firm 2’s reaction function, it knows exactly how much firm 2 will produce in response to any choice of Q1. In other words, firm 1’s initial choice of Q1 completely determines total quantity and the market price. This is enough to allow firm 1 to compute its profits for any choice of Q1. In particular, firm 1 knows that the market price and profits will be:

Price: P 5 100 2 (Q1 1 Q2) 5 100 2 (Q1 1 (45 2 0.5Q1)) 5 55 2 0.5Q1 Profits: 1 5 Revenue 2 Cost 5 PQ1 2 10Q1 5 (55 2 0.5Q1) ? Q1 2 10Q1

Some calculus reveals that the profit-maximizing value of Q1 5 45.4 In response, firm 2 chooses Q2 5 22.5 and the market price is 32.5. Profits are 1 5 $1,012.5 and2 5 $506.25. Firm 1 is doing much better than in the Cournot simultaneous choice model, while firm 2 is doing much, much worse.

By committing to produce 45 units of output instead of 30, firm 1 has forced its rival to cut back production to 22.5; this prevents price from falling too rapidly and makes expansion more profitable for firm 1 than it was in the Cournot model, where firm 2’s output was fixed.

As with the Cournot model, it is unrealistic to expect firms to compute such detailed equations and perform the required calculus. But it is completely believable that firm 1 would anticipate that its commitment to expand output would lead firm 2 to cut back production, providing exactly the incentive for expansion that the formal model demonstrates.

Strategic Substitutes and Strategic Complements

In the Stackelberg game, firm 1’s decision to expand output caused firm 2 to contract output. When one firm chooses more of some action, such as an output decision, and its rival firm cuts back on the same action, we say that the actions are strategic substitutes.5 Quantities in the Stackelberg game are strategic substitutes. When one firm chooses more of an action and its rival chooses more as well, the actions are strategic complements. Prices are usually strategic complements; when one firm raises its price, its rivals may respond by raising theirs. Certainly when one firm lowers its price, we expect its rivals to do so as well. The concepts do not just apply to prices and quantities. If Burger King launches an ad campaign and McDonald’s responds in kind, then advertising is a strategic complement. If Glaxo increases R&D investments in cardiovascular products and Merck scales back its cardio R&D spending in response, then R&D is a strategic substitute.

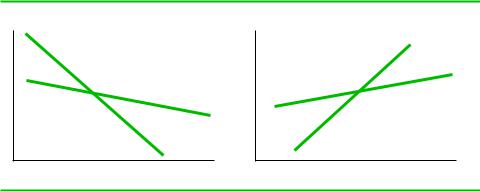

To formalize the concepts of strategic complements and substitutes, we return to the Cournot model of quantity setting and the Bertrand model of price setting. Recall that in the Cournot model it was convenient to represent the equilibrium using reaction functions. In a two-firm Cournot industry, a firm’s reaction function shows its profitmaximizing quantity as a function of the quantity chosen by its competitor. In the Cournot model, reaction functions are downward sloping, as Figure 7.1a shows. Reaction functions in the Bertrand model with horizontally differentiated products are defined analogously.6 In this case, however, the reaction functions are upward sloping, as in Figure 7.1b.

Microdynamics • 229

FIGURE 7.1

Strategic Substitutes and Complements

q2 |

|

p2 |

|

|

R1 |

|

|

R2 |

|

R2 |

|

R1 |

q1 |

p1 |

|

||

(a) |

|

(b) |

Panel (a) shows the relation functions in a Cournot market. The reaction functions R1 and R2 slope downward, indicating that quantities are strategic substitutes. Panel (b) shows the reaction functions in a Bertrand market with differentiated products. The reaction functions slope upward, indicating that prices are strategic complements.

In general, when reaction functions are upward sloping, the firm’s actions (e.g., prices) are strategic complements. When actions are strategic complements, the more of the action one firm chooses, the more of the action the other firm will also optimally choose. In the Bertrand model, prices are strategic complements because when one firm reduces prices, the other firm finds it profitable to reduce prices as well. When reaction functions are downward sloping, the actions are strategic substitutes. When actions are strategic substitutes, the more of the action one firm takes, the less of the action the other firm optimally chooses. In the Cournot model, quantities are strategic substitutes because when one firm increases its quantity, the other firm finds it profitable to also increase quantity.

The Strategic Effect of Commitments

Commitments have both a direct and a strategic effect on a firm’s profitability. The direct effect of the commitment is its impact on the present value of the firm’s profits if the competitor’s behavior does not change. This is analogous to thinking about quantity and price choices in the static Cournot and Bertrand models. For example, if Nucor invests in a process that reduces the average variable cost of producing sheet steel, the direct effect of the investment is the present value of the increase in Nucor’s profit due to the reduction in its average variable costs, less the upfront cost of the investment. The increase in profit would come not only from cost savings on existing units produced, but also from any benefits Nucor gets from lowering its price or increasing its output.

The strategic effect takes into account the competitive side effects of the commitment. How does the commitment alter the tactical decisions of rivals and, ultimately, the market equilibrium? In the Stackelberg game, the increase in production by firm 1 caused its rival to scale back production, which helped support pricing and increase firm 1’s profits. Nucor’s investment would have a strategic effect if it caused rivals to adjust their investment plans (or any other business decisions, for that matter). If a firm takes the long view when making its commitment decision, as we believe it should, then it must take into account how the commitment alters the nature of the equilibrium.

230 • Chapter 7 • Dynamics: Competing Across Time

EXAMPLE 7.1 LOBLAW VERSUS WAL-MART CANADA7

If you have ever gone grocery shopping in Canada, chances are that you have encountered a store owned by Loblaw. With more than 1,050 stores, Loblaw Companies Limited is the largest grocery chain in Canada. Among the stores in its stable of properties are Loblaws, Fortinos, Zehrs Markets, and Your Independent Grocer. In total, Loblaw’s various stores account for about 33 percent of Canada’s grocery market.

Loblaw’s most recent strategic initiative is to construct large superstores that bear the name “The Real Canadian Superstore” or RCSS. These stores, which have 135,000 square feet of selling area, contain a pharmacy– drugstore, a home electronics department, an optical department, a dry cleaner store, apparel and shoe departments, a photo studio, a financial services counter, and, of course, groceries, including the 5,000-plus private label items sold under Loblaw’s “President’s Choice” brand.

The commitment to build RCSS stores was launched in late 2002. Loblaw’s management announced that it would cease building large grocery stores under the names Loblaws, Fortinos, and Zehrs, and would instead embark on a plan to build RCSS stores throughout Canada. Loblaw was very clear about its intentions: it wanted to preempt Wal-Mart Canada from building its own megastores, Wal-Mart Supercenters. Wal-Mart had already built five Sam’s Clubs stores in Ontario, but as of 2002, it had yet to build any Wal-Mart Supercenters.

Loblaw took a number of steps to enhance the credibility of its strategic commitment. First, starting in early 2003, Loblaw opened

talks with the United Food and Commercial Workers (UFCW) union in an attempt to negotiate wage rollbacks for employees transferring to newly opened RCSS stores. The resulting deal was complex, but Loblaw was ultimately successful in achieving a deal for lower wages in RCCS stores. In addition, Loblaw’s management was very public about its ambitions to open RCSS stores throughout Canada. For example, at its annual meeting in May 2004, Loblaw’s president, John Lederer, announced that the company had set aside a $1.4 billion capital budget to construct new RCSS stores during 2004.

A case can be made that Loblaw’s commitment to build multiple RCSS stores has successfully preempted Wal-Mart. The first RCSS store was opened in late 2003; 13 stores were added in 2004, and 7 were slated to be opened in 2005. By contrast, as of mid-2005, Wal-Mart Canada had yet to open any Supercenters and reputedly had no immediate plans to do so. But even if Loblaw ends up merely delaying WalMart’s entry into the megastore segment in Canada, Loblaw’s preemptive commitment might still be considered a success. For one thing, by moving first, Loblaw may be able to lock up the best locations in high-population areas, such as Toronto. For another thing, the high publicity surrounding the opening of RCSS stores, coupled with the enormous selection of grocery and nongrocery items, and an ambience that is reportedly “appealing to all the senses,” may make an RCSS a destination store that shoppers go out of their way to visit despite the presence of lower-priced stores nearby.

Tough and Soft Commitments

Firms do not always benefit from the strategic effects of their commitments. Whether a commitment has a profitable strategic effect depends on whether the commitment is tough or soft and whether the choices involve strategic complements or strategic substitutes.8 Conceptually, a firm’s tough commitment is bad for competitors, whereas a soft commitment is good for its competitors. Capacity expansion usually represents a tough commitment, whereas the elimination of production facilities usually represents