Market Structure and Threats to Sustainability • 365

costs. If incumbent sellers are making profits, and there is free entry into the market, new firms will enter. By slightly differentiating themselves from incumbents, these entrants will find their own niches but will inevitably take some business from incumbents. Chapter 6 explained how entry will continue in this way until incremental profits just cover fixed costs. The fast-food market shows how entry by differentiated sellers (e.g., Taco Bell) ate into the profits of the successful incumbent (McDonald’s). There are countless other examples across many industries.

Successful incumbents in both competitive and monopolistically competitive markets can do little to preserve profits unless they can deter entry. We discussed strategies for doing this in Chapter 6 and in the last part of Chapter 7, where we emphasized how incumbents can create endogenous sunk costs through branding and other strategies. Note that the conditions that tend to facilitate entry deterrence, such as high fixed costs and a dominant firm willing to enforce strategies such as limit pricing, tend to be absent in competitive and monopolistically competitive markets. Although competitive and monopolistically competitive markets do not tend to enjoy sustained periods of profits, individual firms within these markets can prosper by finding uniquely efficient production processes or product enhancements.

Threats to Sustainability under All Market Structures

Even in oligopolistic or monopolistic markets, where entry might be blockaded or deterred, a successful incumbent may not stay successful for long. Sometimes luck plays a role, as when success is due to factors that the incumbent cannot control, such as the weather or general business conditions. For example, the 2011 Japanese earthquake devastated the supply chain of Japanese car makers, allowing U.S. and Korean competitors to increase their market shares. Over time, parts suppliers returned to normal production and the Japanese car makers regained the share they had lost, and U.S. and Korean car makers lost the share they had gained. This is an example of how outlier performance can regress to the mean. The general point about regression to the mean is as follows. Whenever a firm does exceedingly well, one must consider whether it benefited from unusually good luck. Conversely, an underperforming firm might have had bad luck. Since good luck is unlikely to persist (or it would not have been luck), one should not always expect firms to repeat extreme performances, whether good or bad, for long.

Extremely good or bad performance may not always be the result of luck. (If it was, there would be little point in pursuing a business education!) As we discuss later in this chapter, firms may develop genuine advantages that are difficult for others to duplicate. Even this does not guarantee a sustainable flow of profits, however. Although the advantage may be inimitable, so that the firm is protected from the forces of rivalry and entry, the firm may not be protected from powerful buyers and suppliers. Chapter 8 described how powerful buyers and suppliers can use their bargaining leverage to extract profits from a thriving firm. By the same token, they will often give back some of their gains when the firm is struggling. This tends to even out the peaks and valleys in profits that might be experienced by firms that lack powerful buyers and suppliers.

A good example of where supplier power has threatened sustainability is Major League Baseball in the United States. As discussed in Chapter 8, Major League Baseball has enjoyed monopoly status thanks in part to economies of scale and an

366 • Chapter 11 • Sustaining Competitive Advantage

exemption from the U.S. antitrust laws. Even so, many team owners struggle to turn a profit. One reason is the powerful Major League Baseball Players’ Association which, through litigation and a series of successful job actions in the 1970s and 1980s, earned full union rights and elevated the average annual salary of its players from $400,000 in 1987 to $3.3 million in 2011.

Evidence: The Persistence of Profitability

If the forces threatening sustainability were pervasive, economic profits in most industries would quickly converge to zero. By contrast, if there are impediments to the competitive dynamic (e.g., entry barriers discussed in Chapter 6 or barriers to imitation as we discuss later in this chapter), then profits would persist: firms earning above-average profits today continue to do so in the future, while today’s low-profit firms remain low-profit firms in the future. What pattern of profit persistence do we actually observe?

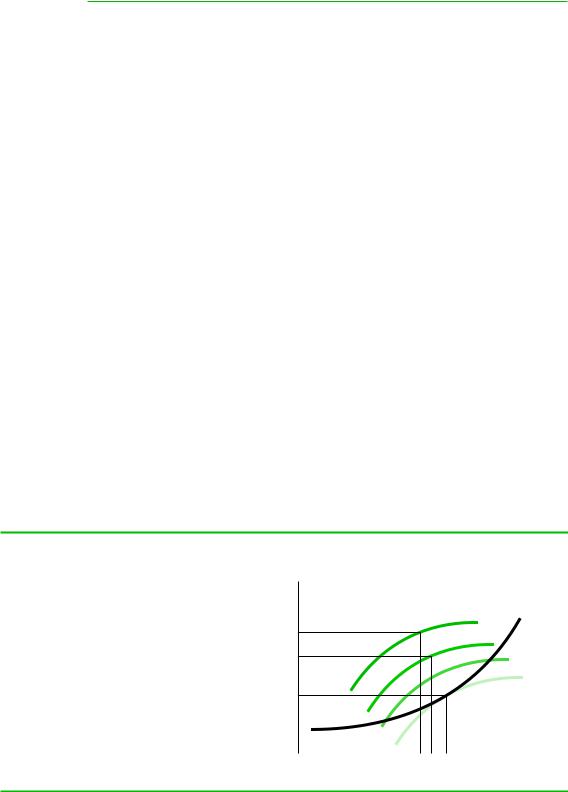

The economist Dennis Mueller has done the most comprehensive study of profit persistence.1 Though dated, the findings should resonate with today’s managers. For a sample of 600 U.S. manufacturing firms for the years 1950–1972, Mueller used statistical techniques to measure profit persistence. Perhaps the easiest way to summarize Mueller’s results is to imagine two groups of U.S. manufacturing firms. One group (the “high-profit” group) has an after-tax accounting return on assets (ROA)—that is, on average, 100 percent greater than the accounting ROA of the typical manufacturing firm. If the typical manufacturing firm had an ROA of 6 percent in 2012, the average ROA of the high-profit group would be 12 percent.2 The other group (the “low-profit” group) has an average ROA of 0 percent. If profit follows the pattern in Mueller’s sample, by 2015 (three years later), the high-profit group’s average ROA would be about 8.6 percent, and by 2022 its average ROA would stabilize at about 7.8 percent. Similarly, by 2015 the low-profit group’s average ROA would be about 4.4 percent, and by 2022 its average ROA would stabilize at about 4.9 percent. Thus, the profits of the two groups get closer over time but do not converge toward a common mean, as the theory of perfect competition would predict.

Mueller’s results suggest that firms with abnormally high levels of profitability tend, on average, to decrease in profitability over time, while firms with abnormally low levels of profitability tend, on average, to experience increases in profitability over time. However, as Figure 11.2 illustrates, the profit rates of these two groups of firms do not converge to a common mean. Firms that start out with high profits converge, in the long run, to rates of profitability that are higher than the rates of profitability of firms that start out with low profits.

Mueller’s work implies that market forces are a threat to profits, but only up to a point. Other forces appear to protect profitable firms. Michael Porter’s five forces, summarized in Chapter 8, are an important class of such forces that mainly apply to entire industries. In this chapter we are concerned with a different class of forces: those that protect the competitive advantage of an individual firm and allow it to persistently outperform its industry. These forces are, at least in principle, distinct from Porter’s five forces. A firm may prosper indefinitely in an otherwise unprofitable industry beset by intense pricing rivalry and low entry barriers (e.g., Southwest Airlines). The sources of its competitive advantage may be so difficult to understand or to imitate that its advantage over its competitors is secure for a long time.