- •Table of Contents

- •What’s New in EViews 5.0

- •What’s New in 5.0

- •Compatibility Notes

- •EViews 5.1 Update Overview

- •Overview of EViews 5.1 New Features

- •Preface

- •Part I. EViews Fundamentals

- •Chapter 1. Introduction

- •What is EViews?

- •Installing and Running EViews

- •Windows Basics

- •The EViews Window

- •Closing EViews

- •Where to Go For Help

- •Chapter 2. A Demonstration

- •Getting Data into EViews

- •Examining the Data

- •Estimating a Regression Model

- •Specification and Hypothesis Tests

- •Modifying the Equation

- •Forecasting from an Estimated Equation

- •Additional Testing

- •Chapter 3. Workfile Basics

- •What is a Workfile?

- •Creating a Workfile

- •The Workfile Window

- •Saving a Workfile

- •Loading a Workfile

- •Multi-page Workfiles

- •Addendum: File Dialog Features

- •Chapter 4. Object Basics

- •What is an Object?

- •Basic Object Operations

- •The Object Window

- •Working with Objects

- •Chapter 5. Basic Data Handling

- •Data Objects

- •Samples

- •Sample Objects

- •Importing Data

- •Exporting Data

- •Frequency Conversion

- •Importing ASCII Text Files

- •Chapter 6. Working with Data

- •Numeric Expressions

- •Series

- •Auto-series

- •Groups

- •Scalars

- •Chapter 7. Working with Data (Advanced)

- •Auto-Updating Series

- •Alpha Series

- •Date Series

- •Value Maps

- •Chapter 8. Series Links

- •Basic Link Concepts

- •Creating a Link

- •Working with Links

- •Chapter 9. Advanced Workfiles

- •Structuring a Workfile

- •Resizing a Workfile

- •Appending to a Workfile

- •Contracting a Workfile

- •Copying from a Workfile

- •Reshaping a Workfile

- •Sorting a Workfile

- •Exporting from a Workfile

- •Chapter 10. EViews Databases

- •Database Overview

- •Database Basics

- •Working with Objects in Databases

- •Database Auto-Series

- •The Database Registry

- •Querying the Database

- •Object Aliases and Illegal Names

- •Maintaining the Database

- •Foreign Format Databases

- •Working with DRIPro Links

- •Part II. Basic Data Analysis

- •Chapter 11. Series

- •Series Views Overview

- •Spreadsheet and Graph Views

- •Descriptive Statistics

- •Tests for Descriptive Stats

- •Distribution Graphs

- •One-Way Tabulation

- •Correlogram

- •Unit Root Test

- •BDS Test

- •Properties

- •Label

- •Series Procs Overview

- •Generate by Equation

- •Resample

- •Seasonal Adjustment

- •Exponential Smoothing

- •Hodrick-Prescott Filter

- •Frequency (Band-Pass) Filter

- •Chapter 12. Groups

- •Group Views Overview

- •Group Members

- •Spreadsheet

- •Dated Data Table

- •Graphs

- •Multiple Graphs

- •Descriptive Statistics

- •Tests of Equality

- •N-Way Tabulation

- •Principal Components

- •Correlations, Covariances, and Correlograms

- •Cross Correlations and Correlograms

- •Cointegration Test

- •Unit Root Test

- •Granger Causality

- •Label

- •Group Procedures Overview

- •Chapter 13. Statistical Graphs from Series and Groups

- •Distribution Graphs of Series

- •Scatter Diagrams with Fit Lines

- •Boxplots

- •Chapter 14. Graphs, Tables, and Text Objects

- •Creating Graphs

- •Modifying Graphs

- •Multiple Graphs

- •Printing Graphs

- •Copying Graphs to the Clipboard

- •Saving Graphs to a File

- •Graph Commands

- •Creating Tables

- •Table Basics

- •Basic Table Customization

- •Customizing Table Cells

- •Copying Tables to the Clipboard

- •Saving Tables to a File

- •Table Commands

- •Text Objects

- •Part III. Basic Single Equation Analysis

- •Chapter 15. Basic Regression

- •Equation Objects

- •Specifying an Equation in EViews

- •Estimating an Equation in EViews

- •Equation Output

- •Working with Equations

- •Estimation Problems

- •Chapter 16. Additional Regression Methods

- •Special Equation Terms

- •Weighted Least Squares

- •Heteroskedasticity and Autocorrelation Consistent Covariances

- •Two-stage Least Squares

- •Nonlinear Least Squares

- •Generalized Method of Moments (GMM)

- •Chapter 17. Time Series Regression

- •Serial Correlation Theory

- •Testing for Serial Correlation

- •Estimating AR Models

- •ARIMA Theory

- •Estimating ARIMA Models

- •ARMA Equation Diagnostics

- •Nonstationary Time Series

- •Unit Root Tests

- •Panel Unit Root Tests

- •Chapter 18. Forecasting from an Equation

- •Forecasting from Equations in EViews

- •An Illustration

- •Forecast Basics

- •Forecasting with ARMA Errors

- •Forecasting from Equations with Expressions

- •Forecasting with Expression and PDL Specifications

- •Chapter 19. Specification and Diagnostic Tests

- •Background

- •Coefficient Tests

- •Residual Tests

- •Specification and Stability Tests

- •Applications

- •Part IV. Advanced Single Equation Analysis

- •Chapter 20. ARCH and GARCH Estimation

- •Basic ARCH Specifications

- •Estimating ARCH Models in EViews

- •Working with ARCH Models

- •Additional ARCH Models

- •Examples

- •Binary Dependent Variable Models

- •Estimating Binary Models in EViews

- •Procedures for Binary Equations

- •Ordered Dependent Variable Models

- •Estimating Ordered Models in EViews

- •Views of Ordered Equations

- •Procedures for Ordered Equations

- •Censored Regression Models

- •Estimating Censored Models in EViews

- •Procedures for Censored Equations

- •Truncated Regression Models

- •Procedures for Truncated Equations

- •Count Models

- •Views of Count Models

- •Procedures for Count Models

- •Demonstrations

- •Technical Notes

- •Chapter 22. The Log Likelihood (LogL) Object

- •Overview

- •Specification

- •Estimation

- •LogL Views

- •LogL Procs

- •Troubleshooting

- •Limitations

- •Examples

- •Part V. Multiple Equation Analysis

- •Chapter 23. System Estimation

- •Background

- •System Estimation Methods

- •How to Create and Specify a System

- •Working With Systems

- •Technical Discussion

- •Vector Autoregressions (VARs)

- •Estimating a VAR in EViews

- •VAR Estimation Output

- •Views and Procs of a VAR

- •Structural (Identified) VARs

- •Cointegration Test

- •Vector Error Correction (VEC) Models

- •A Note on Version Compatibility

- •Chapter 25. State Space Models and the Kalman Filter

- •Background

- •Specifying a State Space Model in EViews

- •Working with the State Space

- •Converting from Version 3 Sspace

- •Technical Discussion

- •Chapter 26. Models

- •Overview

- •An Example Model

- •Building a Model

- •Working with the Model Structure

- •Specifying Scenarios

- •Using Add Factors

- •Solving the Model

- •Working with the Model Data

- •Part VI. Panel and Pooled Data

- •Chapter 27. Pooled Time Series, Cross-Section Data

- •The Pool Workfile

- •The Pool Object

- •Pooled Data

- •Setting up a Pool Workfile

- •Working with Pooled Data

- •Pooled Estimation

- •Chapter 28. Working with Panel Data

- •Structuring a Panel Workfile

- •Panel Workfile Display

- •Panel Workfile Information

- •Working with Panel Data

- •Basic Panel Analysis

- •Chapter 29. Panel Estimation

- •Estimating a Panel Equation

- •Panel Estimation Examples

- •Panel Equation Testing

- •Estimation Background

- •Appendix A. Global Options

- •The Options Menu

- •Print Setup

- •Appendix B. Wildcards

- •Wildcard Expressions

- •Using Wildcard Expressions

- •Source and Destination Patterns

- •Resolving Ambiguities

- •Wildcard versus Pool Identifier

- •Appendix C. Estimation and Solution Options

- •Setting Estimation Options

- •Optimization Algorithms

- •Nonlinear Equation Solution Methods

- •Appendix D. Gradients and Derivatives

- •Gradients

- •Derivatives

- •Appendix E. Information Criteria

- •Definitions

- •Using Information Criteria as a Guide to Model Selection

- •References

- •Index

- •Symbols

- •.DB? files 266

- •.EDB file 262

- •.RTF file 437

- •.WF1 file 62

- •@obsnum

- •Panel

- •@unmaptxt 174

- •~, in backup file name 62, 939

- •Numerics

- •3sls (three-stage least squares) 697, 716

- •Abort key 21

- •ARIMA models 501

- •ASCII

- •file export 115

- •ASCII file

- •See also Unit root tests.

- •Auto-search

- •Auto-series

- •in groups 144

- •Auto-updating series

- •and databases 152

- •Backcast

- •Berndt-Hall-Hall-Hausman (BHHH). See Optimization algorithms.

- •Bias proportion 554

- •fitted index 634

- •Binning option

- •classifications 313, 382

- •Boxplots 409

- •By-group statistics 312, 886, 893

- •coef vector 444

- •Causality

- •Granger's test 389

- •scale factor 649

- •Census X11

- •Census X12 337

- •Chi-square

- •Cholesky factor

- •Classification table

- •Close

- •Coef (coefficient vector)

- •default 444

- •Coefficient

- •Comparison operators

- •Conditional standard deviation

- •graph 610

- •Confidence interval

- •Constant

- •Copy

- •data cut-and-paste 107

- •table to clipboard 437

- •Covariance matrix

- •HAC (Newey-West) 473

- •heteroskedasticity consistent of estimated coefficients 472

- •Create

- •Cross-equation

- •Tukey option 393

- •CUSUM

- •sum of recursive residuals test 589

- •sum of recursive squared residuals test 590

- •Data

- •Database

- •link options 303

- •using auto-updating series with 152

- •Dates

- •Default

- •database 24, 266

- •set directory 71

- •Dependent variable

- •Description

- •Descriptive statistics

- •by group 312

- •group 379

- •individual samples (group) 379

- •Display format

- •Display name

- •Distribution

- •Dummy variables

- •for regression 452

- •lagged dependent variable 495

- •Dynamic forecasting 556

- •Edit

- •See also Unit root tests.

- •Equation

- •create 443

- •store 458

- •Estimation

- •EViews

- •Excel file

- •Excel files

- •Expectation-prediction table

- •Expected dependent variable

- •double 352

- •Export data 114

- •Extreme value

- •binary model 624

- •Fetch

- •File

- •save table to 438

- •Files

- •Fitted index

- •Fitted values

- •Font options

- •Fonts

- •Forecast

- •evaluation 553

- •Foreign data

- •Formula

- •forecast 561

- •Freq

- •DRI database 303

- •F-test

- •for variance equality 321

- •Full information maximum likelihood 698

- •GARCH 601

- •ARCH-M model 603

- •variance factor 668

- •system 716

- •Goodness-of-fit

- •Gradients 963

- •Graph

- •remove elements 423

- •Groups

- •display format 94

- •Groupwise heteroskedasticity 380

- •Help

- •Heteroskedasticity and autocorrelation consistent covariance (HAC) 473

- •History

- •Holt-Winters

- •Hypothesis tests

- •F-test 321

- •Identification

- •Identity

- •Import

- •Import data

- •See also VAR.

- •Index

- •Insert

- •Instruments 474

- •Iteration

- •Iteration option 953

- •in nonlinear least squares 483

- •J-statistic 491

- •J-test 596

- •Kernel

- •bivariate fit 405

- •choice in HAC weighting 704, 718

- •Kernel function

- •Keyboard

- •Kwiatkowski, Phillips, Schmidt, and Shin test 525

- •Label 82

- •Last_update

- •Last_write

- •Latent variable

- •Lead

- •make covariance matrix 643

- •List

- •LM test

- •ARCH 582

- •for binary models 622

- •LOWESS. See also LOESS

- •in ARIMA models 501

- •Mean absolute error 553

- •Metafile

- •Micro TSP

- •recoding 137

- •Models

- •add factors 777, 802

- •solving 804

- •Mouse 18

- •Multicollinearity 460

- •Name

- •Newey-West

- •Nonlinear coefficient restriction

- •Wald test 575

- •weighted two stage 486

- •Normal distribution

- •Numbers

- •chi-square tests 383

- •Object 73

- •Open

- •Option setting

- •Option settings

- •Or operator 98, 133

- •Ordinary residual

- •Panel

- •irregular 214

- •unit root tests 530

- •Paste 83

- •PcGive data 293

- •Polynomial distributed lag

- •Pool

- •Pool (object)

- •PostScript

- •Prediction table

- •Principal components 385

- •Program

- •p-value 569

- •for coefficient t-statistic 450

- •Quiet mode 939

- •RATS data

- •Read 832

- •CUSUM 589

- •Regression

- •Relational operators

- •Remarks

- •database 287

- •Residuals

- •Resize

- •Results

- •RichText Format

- •Robust standard errors

- •Robustness iterations

- •for regression 451

- •with AR specification 500

- •workfile 95

- •Save

- •Seasonal

- •Seasonal graphs 310

- •Select

- •single item 20

- •Serial correlation

- •theory 493

- •Series

- •Smoothing

- •Solve

- •Source

- •Specification test

- •Spreadsheet

- •Standard error

- •Standard error

- •binary models 634

- •Start

- •Starting values

- •Summary statistics

- •for regression variables 451

- •System

- •Table 429

- •font 434

- •Tabulation

- •Template 424

- •Tests. See also Hypothesis tests, Specification test and Goodness of fit.

- •Text file

- •open as workfile 54

- •Type

- •field in database query 282

- •Units

- •Update

- •Valmap

- •find label for value 173

- •find numeric value for label 174

- •Value maps 163

- •estimating 749

- •View

- •Wald test 572

- •nonlinear restriction 575

- •Watson test 323

- •Weighting matrix

- •heteroskedasticity and autocorrelation consistent (HAC) 718

- •kernel options 718

- •White

- •Window

- •Workfile

- •storage defaults 940

- •Write 844

- •XY line

- •Yates' continuity correction 321

658—Chapter 21. Discrete and Limited Dependent Variable Models

Note that the header information indicates that the model is a truncated specification, and that the sample information at the bottom of the screen shows that there are no left and right censored observations.

Count Models

Count models are employed when y takes integer values that represent the number of events that occur—examples of count data include the number of patents filed by a company, and the number of spells of unemployment experienced over a fixed time interval.

EViews provides support for the estimation of several models of count data. In addition to the standard poisson and negative binomial maximum likelihood (ML) specifications, EViews provides a number of quasi-maximum likelihood (QML) estimators for count data.

Estimating Count Models in EViews

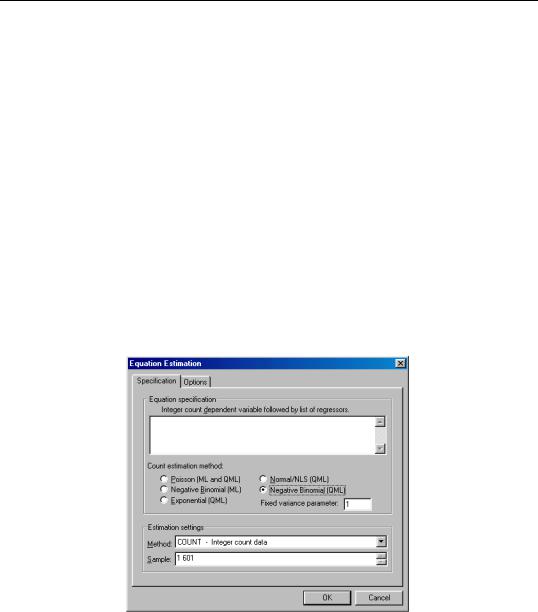

To estimate a count data model, select Quick/Estimate Equation… from the main menu, and select COUNT as the estimation method. EViews displays the count estimation dialog into which you will enter the dependent and explanatory variable regressors, select a type of count model, and if desired, set estimation options.

There are three parts to the specification of the count model:

•In the upper edit field, you should list the dependent variable and the independent variables. You must specify your model by list. The list of explanatory variables specifies a model for the conditional mean of the dependent variable:

m( xi, β) = E( yi |

|

xi, β) = exp ( xi′β) . |

(21.38) |

|

Count Models—659

•Next, click on Options and, if desired, change the default estimation algorithm, convergence criterion, starting values, and method of computing the coefficient covariance.

•Lastly, select one of the entries listed under count estimation method, and if appropriate, specify a value for the variance parameter. Details for each method are provided in the following discussion.

Poisson Model

For the Poisson model, the conditional density of yi given xi |

is: |

|

|||||

f( y |

i |

|

x , β) |

= |

e−m(xi, β)m( x , β)yi ⁄ |

y ! |

(21.39) |

|

|||||||

|

|

i |

|

i |

i |

|

|

where yi is a non-negative integer valued random variable. The maximum likelihood estimator (MLE) of the parameter β is obtained by maximizing the log likelihood function:

N |

|

l( β) = Σ yilog m( xi, β) − m( xi, β) − log ( yi!) . |

(21.40) |

i = 1

Provided the conditional mean function is correctly specified and the conditional distribu-

|

ˆ |

|

|

|

|

|

|

|

|

|

|

tion of y is Poisson, the MLE β is consistent, efficient, and asymptotically normally dis- |

|||||||||||

tributed, with variance matrix consistently estimated by: |

|

|

|

|

|||||||

|

ˆ |

|

|

N |

|

ˆ |

ˆ |

|

|

|

−1 |

|

|

|

∂mi ∂mi |

ˆ |

|

||||||

|

V = var(β ) |

= |

|

--------- --------- |

(21.41) |

||||||

|

|

Σ |

|

⁄ m |

i |

||||||

|

|

|

∂β ∂β′ |

|

|

||||||

|

|

|

|

i = 1 |

|

|

|

|

|

|

|

ˆ |

ˆ |

|

|

|

|

|

|

|

|

|

|

where mi = |

m( xi, β) . |

|

|

|

|

|

|

|

|

|

|

The Poisson assumption imposes restrictions that are often violated in empirical applications. The most important restriction is the equality of the (conditional) mean and variance:

v( xi, β) = var( yi |

|

xi, β) = E( yi |

|

xi, β) = m( xi, β) . |

(21.42) |

|

|

If the mean-variance equality does not hold, the model is misspecified. EViews provides a number of other estimators for count data which relax this restriction.

We note here that the Poisson estimator may also be interpreted as a quasi-maximum likelihood estimator. The implications of this result are discussed below.

Negative Binomial (ML)

One common alternative to the Poisson model is to estimate the parameters of the model using maximum likelihood of a negative binomial specification. The log likelihood for the negative binomial distribution is given by:

660—Chapter 21. Discrete and Limited Dependent Variable Models

N |

|

l( β, η) = Σ yilog ( η2m( xi, β) ) |

(21.43) |

i= 1

−( yi + 1 ⁄ η2) log ( 1 + η2m( xi, β) )

+ log Γ( yi + 1 ⁄ η2) −log ( yi!) − log Γ( 1 ⁄ η2)

where η2 is a variance parameter to be jointly estimated with the conditional mean parameters β . EViews estimates the log of η2 , and labels this parameter as the “SHAPE” parameter in the output. Standard errors are computed using the inverse of the information matrix.

The negative binomial distribution is often used when there is overdispersion in the data, so that v( xi, β) > m( xi, β) , since the following moment conditions hold:

E( yi xi, β) = m( xi, β)

(21.44)

var( yi xi, β) = m( xi, β) ( 1 + η2m( xi, β) )

η2 is therefore a measure of the extent to which the conditional variance exceeds the conditional mean.

Consistency and efficiency of the negative binomial ML requires that the conditional distribution of y be negative binomial.

Quasi-maximum Likelihood (QML)

We can perform maximum likelihood estimation under a number of alternative distributional assumptions. These quasi-maximum likelihood (QML) estimators are robust in the sense that they produce consistent estimates of the parameters of a correctly specified conditional mean, even if the distribution is incorrectly specified.

This robustness result is exactly analogous to the situation in ordinary regression, where the normal ML estimator (least squares) is consistent, even if the underlying error distribution is not normally distributed. In ordinary least squares, all that is required for consistency is a correct specification of the conditional mean m( xi, β) = xi′β . For QML count models, all that is required for consistency is a correct specification of the conditional mean m( xi, β) .

The estimated standard errors computed using the inverse of the information matrix will not be consistent unless the conditional distribution of y is correctly specified. However, it is possible to estimate the standard errors in a robust fashion so that we can conduct valid inference, even if the distribution is incorrectly specified.

Count Models—661

EViews provides options to compute two types of robust standard errors. Click Options in the Equation Specification dialog box and mark the Robust Covariance option. The Huber/White option computes QML standard errors, while the GLM option computes standard errors corrected for overdispersion. See “Technical Notes” on page 667 for details on these options.

Further details on QML estimation are provided by Gourioux, Monfort, and Trognon (1994a, 1994b). Wooldridge (1996) provides an excellent summary of the use of QML techniques in estimating parameters of count models. See also the extensive related literature on Generalized Linear Models (McCullagh and Nelder, 1989).

Poisson

The Poisson MLE is also a QMLE for data from alternative distributions. Provided that the conditional mean is correctly specified, it will yield consistent estimates of the parameters β of the mean function. By default, EViews reports the ML standard errors. If you wish to compute the QML standard errors, you should click on Options, select Robust Covariances, and select the desired covariance matrix estimator.

Exponential :

The log likelihood for the exponential distribution is given by:

N |

|

l( β) = Σ − log m( xi, β) − yi ⁄ ( m( xi, β) ) . |

(21.45) |

i = 1

As with the other QML estimators, the exponential QMLE is consistent even if the conditional distribution of yi is not exponential, provided that mi is correctly specified. By default, EViews reports the robust QML standard errors.

Normal

The log likelihood for the normal distribution is:

|

N |

1 |

|

y |

i |

− m( x , β) |

|

2 |

1 |

2 |

1 |

|

l( β) = |

Σ |

− -- |

|

-------------------------------- |

|

|

− --log ( σ |

|

) − --log ( 2π) . |

(21.46) |

||

|

2 |

|

|

σ |

|

2 |

|

2 |

|

|||

|

i = 1 |

|

|

|

|

|

|

|

|

|

|

|

For fixed σ2 and correctly specified mi , maximizing the normal log likelihood function provides consistent estimates even if the distribution is not normal. Note that maximizing the normal log likelihood for a fixed σ2 is equivalent to minimizing the sum of squares for the nonlinear regression model:

yi = m( xi, β) + i . |

(21.47) |

EViews sets σ2 = 1 by default. You may specify any other (positive) value for σ2 |

by |

changing the number in the Fixed variance parameter field box. By default, EViews reports the robust QML standard errors when estimating this specification.