408 Public Administration in Southeast Asia

visionary and reform-minded local chief executives to implement innovative programs in pursuit of local development objectives and raise the performance levels of their respective LGUs.

A number of these initiatives are widely acclaimed and multi-awarded within and outside the country, such as the performance and transformation of Naga City under the leadership of Mayor Jesse Robredo. The Naga City government demonstrated how the full potential of the various offices and of the entire city can be tapped for effective and efficient delivery of public services that meet the requirements of the population. It focused on getting optimum outputs with minimum expenditures and producing desired quality results as planned. It succeeded in making services not only accessible, but also acceptable on the basis of the greatest good for the greatest number (UNDESA, 1997: 105–6).

Mandaluyong City embarked on a BOT scheme to construct a public market. In partnership with the private sector, the LGU built a public market with a mall that approaches world-class standards. It provided the land while the private sector built and operated the market. The revenues of the city increased because of the numerous business and license taxes collected from the establishments in the market/mall (UNDESA, 1997: 105). These innovations are reflective of NPM, which encourages private sector methods and broadening citizen participation.

20.4.1.5 Improving Work Processes

To seize the potentials of information and communication technology for national development, President Ramos approved and adopted the National Information Technology Plan (NITP) 2000 and established the National Information Technology Council in 1994 (RP, 1994). In October 1997, he further adopted the updated NITP 2000 that reoriented and revitalized public service delivery through information technology (IT). The computerization of the Bureau of Internal Revenue (BIR) and the Bureau of Customs (BOC), the revenue generating arms of government, contributed a great deal to the improvement of their operations (Carlos, 2004: 58).

To standardize the processing time for the bidding and award process for infrastructure, construction work, and consultancy service contracts of the national government, President Ramos issued Administrative Order No. 129 on May 16, 1994.

20.4.2 Performance Management Initiatives for the New Millennium

Government efforts to improve the performance of the bureaucracy that are reflective of NPM principles are anchored on the legal foundations built after the restoration of democracy in 1986.

20.4.2.1 Financial Management

There are four major processes in financial management: budget making; budget implementation; accounting; and audit (OECD, 2001: 17). Several oversight agencies share responsibility for financial management in the Philippines. Revenue generation, cash management, borrowings, and oversight over the finances of GOCCs and LGUs rest with the DOF and its agencies. The Department of Budget and Management (DBM), on the other hand, is responsible for the budget, organizational management, and compensation policy for the public sector. Meanwhile, in addition to its audit functions, the COA issues accounting rules and regulations. This fragmentation of responsibilities for financial management has put considerable strain on government agencies that have to deal with numerous, overlapping, and oftentimes conflicting policies, guidelines, and reportorial requirements (GOP, WB, ADB, 2003: 67).

© 2011 by Taylor and Francis Group, LLC

Performance Management Reforms in the Philippines 409

20.4.2.2 New Government Accounting System

To strengthen public fiscal accountability, the COA introduced a new accounting system (NGAS) in November 2001, to replace the “outmoded” 50-year-old accounting system. The COA mandated all national agencies and LGUs to implement the NGAS, which is based on a modified accrual accounting system that follows international accounting standards. The NGAS simplifies accounting concepts and procedures, ensures correct, complete, and timely recording of government financial transactions, facilitates the timely preparation of financial reports, and presents a clearer picture of the government’s financial position. It adopts responsibility accounting that is activity-based, a feature not present in the old system (Carague, 2009: 73–75; Carague, 2004: 46–47; GOP, WB, ADB, 2003: xi). In contrast to cash accounting, which registers costs when payments are made and revenues when they are received, accruals accounting records costs and revenues as they are incurred or earned. Advocates of accruals accounting argue that “it yields improved management information” and “facilitates a closer integration of financial and performance measures” (OECD, 2001: 19).

The old accounting system deviated from common accounting practices. It was complex and thus caused problems in compliance with reporting requirements. It did not accurately reflect the full cost of agency operations and was unable to allow benchmarking of costs with the private sector (NEDA, 2001: 262). It produced a balance sheet and a statement of operations, but the latter was neither an income statement nor a cash flow statement, much less a funds flow statement. By contrast, the NGAS produces a balance sheet, income statement, cash flow statement, and generates financial information in real time, which is vital to decision making.

Prior to the NGAS, the various agencies, the Bureau of Treasury, and the COA kept separate sets of accounting records. The lack of regular reconciliation procedures resulted in large amounts of unreconciled balances, “which cast doubt on the accuracy of the financial reports that the system produced” (NEDA, 2001: 262). The NGAS has harmonized the accounting systems of national agencies, LGUs, and GOCCs, thus facilitating evaluation of financial performance. The NGAS has made some report requirements of oversight agencies redundant (Carague, 2009: 73–79).

To guarantee correctness, reliability, completeness, and timeliness, the COA funded the development of electronic accounting software (e-NGAS) from its own savings. In October 2003, only the Office of the President, the CSC, the Department of Social Welfare and Development, and two LGUs applied the e-NGAS. By 2007, 207 national and local government agencies and GOCCs had the e-NGAS installed. This, however, represents only 10% of all government agencies. The rest are still using the manual version of the NGAS.

It is still too early to say whether the NGAS will be sustained after a change in the COA leadership without the required legislation. Furthermore, the estimated cost of shifting to e-NGAS for the remaining 90% of agencies is a staggering Php850 million (Carague, 2009: 79), something the government can ill afford at this time.

The COA has restructured its offices across the regions to strengthen the performance of its audit functions. It is also moving toward value-for-money auditing and developing a risk-based auditing model.

20.4.2.3 Public Expenditure Management

A key component of the Philippine government reform program is Public Expenditure Management (PEM). The government has been implementing reforms in PEM since 1998, as advocated by the World Bank, to pursue fiscal discipline, allocate resources efficiently, and obtain the best value for

© 2011 by Taylor and Francis Group, LLC

410 Public Administration in Southeast Asia

money. The DBM, the DOF, and the National Economic and Development Authority (NEDA), the highest economic planning agency of the government, are jointly responsible for PEM, which emphasizes the importance of performance-based or results-based budgeting.

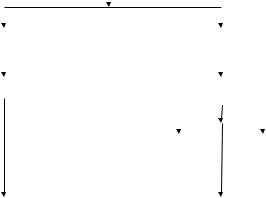

The MTPDP is the blueprint for Philippine development that guides the economy. To better support the government’s development strategy, PEM establishes a results-based MTEF, which involves the development of performance indicators and a performance measurement system, and consists of fiscal and investment components (Boncodin, 2004: 4). Figure 20.2 reflects the various components of the MTEF.

The fiscal component of the MTEF includes a more realistic medium-term fiscal plan (MTFP). The MTFP is the fiscal blueprint for a 6-year period. It is made up of an explicit statement of medium-term fiscal targets on a macro level in terms of deficit reduction, revenue and disbursement, and the overall debt management strategy. It includes an estimate of the cost of ongoing and committed programs that impact on the medium-term position of the government. This cost estimate is reflected in the annual budget submitted to and approved by Congress. PEM uses the budget as an instrument for ensuring desired results. A 3-year rolling budget was introduced in 2001 to cost ongoing as well as proposed programs, activities, and projects (PAPs) (Boncodin, 2004: 2–4; GOP, WB, ADB, 2003: xix). The 1-year budget has been criticized for its tendency to allocate resources for agency programs and for its lack of a system of prioritization. The multi-year budget links budgeting decisions to medium-term fiscal targets.

The MTFP establishes clear targets and assessment mechanisms, strengthens incentive structures, and enlists the support of civil society to monitor results. It includes a clear set of rules for updating revenue and cost estimates such as how to balance the national budget and reduce the public debt to GDP ratio.

The investment component consists of the medium-term public investment program (MTPIP). It lists the broad investment requirements to support growth, the programs and projects that

|

|

|

|

Medium-Term Philippine Development Plan |

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FISCAL |

|

|

|

|

|

INVESTMENT |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Medium–Term |

|

|

|

|

|

Medium-Term Public |

|

|

|

||||||||||

|

|

Fiscal Plan |

|

|

|

|

|

Investment Program |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Annual Budget |

|

|

|

|

Organizational Performance |

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Indicator Framework |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sectoral |

|

|

|

|

Agency |

|

|

||||

|

|

|

|

|

|

|

|

E ectiveness |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

Performance |

|

|

|||||||

|

|

|

|

|

|

|

|

and E ciency |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

Review |

|

|

||||||

|

|

|

|

|

|

|

|

|

Review |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Incentive Structure |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Figure 20.2 Medium-Term Expenditure Framework. (Boncodin, E. T., Introducing ResultsBased Approaches into Public Sector Management Processes: The Philippine Experience. Paper presented during the 2nd International Roundtable on Management for Development Results, Marrakech, Morocco, February 5, 2004, 3.)

© 2011 by Taylor and Francis Group, LLC

Performance Management Reforms in the Philippines 411

will be pursued over a 6-year period, and the possible modes of funding them. An important component of the MTPIP is the Organizational Performance Indicator Framework (OPIF). The OPIF identifies and prioritizes the investment programs that best contribute to the medium-term development goals. It shifts indicators from inputs to output/outcome performance indicators. It enables agencies to focus efforts and resources on core functions and undertake high impact activities at reasonable costs. A key element of the reform is the separation of administrative priority setting from political priority setting. Agency outputs are identified separately from the identification of the outcomes that result from these outputs.

The OPIF is a roadmap that defines where government and its instrumentalities should direct their development efforts. It focuses on objectives and the corresponding outcomes to be achieved and clarifies the expected performance and accountability of government agencies. The OPIF establishes an integrated performance management system (PMS) where organizational performance targets are cascaded down to lower level units and used as a basis for performance-based compensation. The PAPs of the different government departments and agencies should be able to show how these contribute to the achievement of the societal, sectoral, and organizational goals and objectives. The activities involved in the OPIF are outlined below (Boncodin, 2004: 2–6; GOP, WB, ADB, 2003):

(1)The oversight agencies and the line agencies identify desired outputs and outcomes on a parallel basis

(2)This includes the identification of major final outputs measured in terms of quality, quantity, timeliness, and cost

(3)Harmonization workshops level the understanding of these targets for both the oversight agencies and the line agencies

(4)Programs and projects that contribute to the realization of the major final outputs are identified

(5)The performance indicators for each major final output are identified

The OPIF is applied to only about 42% of the national budget, however, and does not include the Special Purpose Fund, which is Php850 billion. The 42% represents the budget of line agencies, not all of which are using the OPIF. It is tedious to apply, not to mention the difficulty of determining the major final outputs and identifying relevant performance indicators rather than simply process outputs or work counts. For instance, what would be a quality indicator for a justice program? In 2004, only six departments had completed their OPIF (Boncodin, 2004: 7) and by 2007, the number more than doubled.

The Sectoral Effectiveness and Efficiency Review (SEER) is a tool for regularly assessing the efficiency and effectiveness of ongoing PAPs of an agency and their actual contribution in attaining desired sectoral outcomes. It enables the government to review priorities to determine what will be discontinued, downscaled, or continued over the medium term and to redirect its resources and strategic programs. An assessment of the PEM revealed that oversight agencies have been more advanced than line agencies in implementing the SEERs because the former have better skills and greater capacity to do so. The implementation of the SEER has led to the termination of projects, restructuring of others, and the cancellation of excess fi nancing of projects.

The Agency Performance Review (APR) complements the SEERs through a more detailed assessment of the specific agency’s performance, particularly their budget utilization and whether funds should be released to them (Boncodin, 2004: 8).

© 2011 by Taylor and Francis Group, LLC