|

|

|

|

Does Prospect Theory Solve the Whole Problem? |

|

267 |

|

Does Prospect Theory Solve the Whole Problem?

Prospect theory is relatively effective in explaining the majority of decisions under risk observed in the laboratory and many behaviors observed in the field. However, most of these risks take on a very specialized form. The majority of risks presented in this chapter and in Chapter 9 are dichotomous choice problems. In other words, the decision maker can choose either to take the gamble or to reject it. Further, most of the gambles we have discussed can result in only a small set of discrete outcomes. In many cases there are only two or three possible outcomes. The majority of risky decisions that are studied by economists are not so simple. If we wished to study investment behavior, each investor has a nearly infinite choice of potential combinations of stocks, bonds, real assets, or commodities they can choose to invest their money in. Moreover, they may invest any amount of money they have access to. Thus, most interesting investment decisions are not dichotomous. Moreover, most investments have potential payoffs in a very wide range. One might lose all one’s investment, might double it, or might fall anywhere in between. The lack of realism in the laboratory has caused many to question the veracity of prospect theory and other behavioral models of decision under risk. Perhaps these models only work when facing this very specialized set of decision problems.

Graham Loomes was one of the first researchers to explore continuous-choice investment in a laboratory setting. He designed a special experiment to mirror, in a limited way, the common investment problem. In Decision 1, he endowed his participants with $20 that they could allocate between two investments, A1 and B1. In the standard investment problem, investors must invest their money in a wide array of investments that might have different payoffs depending on the outcome. Typically, investors reduce the amount of risk they face by diversifying their portfolio of investments. Participants in Loomes’ experiment had a probability of 0.6 of receiving the amount invested in A1 and a probability of 0.4 of receiving the amount invested in B1. An expected utility maximizer would solve

maxA1 ≤ 200.6U A1 + 0.4U 20 − A1 . |

10 18 |

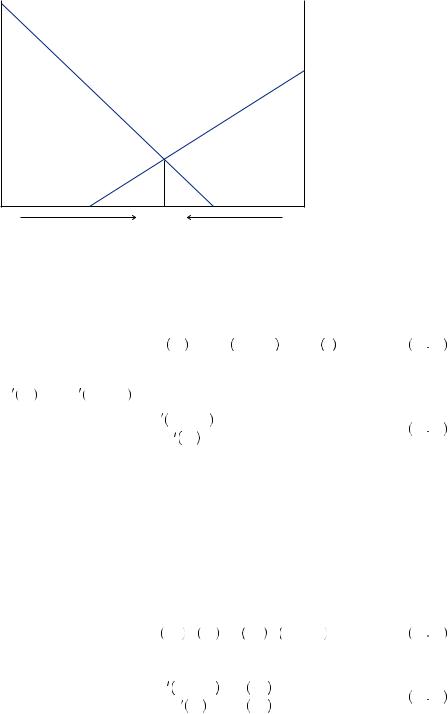

The solution to equation 10.18 occurs where the expected marginal utility between the two investments is equal. This is depicted in Figure 10.9, where the vertical axis is the marginal utility weighted by the probability of a particular outcome, and the horizontal axis measures the allocation between investments A1 and A2. As you move to the right in the figure, the allocation to A1 increases and the allocation to B1 decreases. The curve labeled 0.6U A1

A1 represents the probability of outcome A1, which is 0.6, multiplied by the marginal utility of wealth given the allocation,U

represents the probability of outcome A1, which is 0.6, multiplied by the marginal utility of wealth given the allocation,U A1

A1 . One should continue to increase the allocation to A1 until the weighted marginal utility from A1 is equal to the weighted marginal utility from B1, the curve labeled 0.4U

. One should continue to increase the allocation to A1 until the weighted marginal utility from A1 is equal to the weighted marginal utility from B1, the curve labeled 0.4U B1

B1 . This point is depicted in the figure as

. This point is depicted in the figure as  A*1, B*1

A*1, B*1 . This occurs where 0.6U

. This occurs where 0.6U A1

A1 = 0.4U

= 0.4U 20 − A1

20 − A1 , assuming that it is not optimal to put all of the money in one of the investments.

, assuming that it is not optimal to put all of the money in one of the investments.

These first-order conditions can be written as

U 20 − A1 |

= |

0.6 |

= 1.5. |

10 19 |

U A1 |

|

|||

0.4 |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

Prospect Theory and Risk Aversion in Small Gambles |

|

269 |

|

|||||

Decision 2 would have the decision maker solve |

|

|

|

|

|

|

|||

maxA2 ≤ 20π 0.3 U A2 + π 0.2 U 20 − A2 + π 0.5 U 0 , |

10 24 |

|

|

|

|||||

with solution given by |

|

|

|

|

|

|

|

|

|

U 20 − A2 |

= |

π |

0.3 |

. |

10 25 |

|

|

|

|

|

U A2 |

|

0.2 |

|

|

||||

|

π |

|

|

|

|

|

|||

Equations 10.23 and 10.25 imply different allocations in the decision problems owing to the distortion of probabilities through the probability-weighting function. However, probability-weighting functions are believed to cross the 45-degree line at somewhere between 0.3 and 0.4. Above this, the probability weight should be lower than the

probability, and below this it should be higher than the probability. Thus, |

π 0.6 |

< |

π 0.3 |

, |

||||

|

π 0.2 |

|||||||

π 0.4 |

||||||||

implying that |

U 20 − A1 |

< |

U 20 − A2 |

. Given that all outcomes are coded as gains, people |

||||

U A1 |

|

|||||||

|

|

U A2 |

|

|

|

|

||

should display risk aversion, meaning that marginal utility is declining for larger rewards. Thus, U 20 − A

20 − A gets larger for larger values of A, and U

gets larger for larger values of A, and U A

A gets smaller for

gets smaller for

larger values of A, implying that U 20 − A |

U A increases as A increases. Recall that |

|||

probability weights lead us to believe that |

U 20 − A1 |

< |

U 20 − A2 |

, so that A1 < A2, the |

U A1 |

|

|||

|

|

U A2 |

||

outcome observed in exactly 1 of 85 participants. The majority of participants behave in a way that is inconsistent with the probability-weighting model. Although no alternative theory has come to prominence to explain this anomaly, it may be a signal that con- tinuous-choice problems result from very different behaviors than the simple dichoto- mous-choice problems that are so common in the laboratory.

Prospect Theory and Risk Aversion

in Small Gambles

Further evidence that we might not fully understand how risky choices are made can be found by examining the small-risk problem identified by Matthew Rabin and discussed in Chapter 6. If we attempt to explain any risk-averse behavior using expected utility theory, the only tool with which we can explain it is diminishing marginal utility of wealth, or concavity of the utility function. The most fundamental principle of calculus is the observation that continuous functions are approximately linear over short intervals. Thus, when small amounts of money are at stake, a utility of wealth function should be approximately linear, implying local risk neutrality. If instead, we observe risk-averse behavior over very small gambles, this then implies that the utility function must be extremely concave, and unreasonably so. This led Rabin to derive the following theorem (see Chapter 6 for a full discussion and greater intuition).

is strictly increasing and weakly concave. Suppose there exists

is strictly increasing and weakly concave. Suppose there exists

, where

, where 10

10 26

26

is strictly increasing and weakly concave. Let

is strictly increasing and weakly concave. Let

. Suppose there exists

. Suppose there exists  1

1  probability of losing l. Then the person would also turn down a bet with

probability of losing l. Then the person would also turn down a bet with  1

1  probability of losing 2

probability of losing 2

, where

, where

is de

is de

|

|

|

|

|

|

|

|

|

Prospect Theory and Risk Aversion in Small Gambles |

|

271 |

|

|||

Table 10.2 Examples Applying Rabin’s Theorem |

|

|

|

|

|||

|

|

|

|

|

|

||

If You Would Turn Down |

|

Then You Should Also Turn Down |

|

|

|

||

|

|

|

|

|

|

|

|

Winning with |

Losing with 0.5 |

|

Winning with |

Losing with 0.5 |

|

|

|

0.5 Probability |

Probability |

|

0.5 Probability |

Probability |

|

|

|

|

|

|

|

|

|

|

|

$110 |

− $100 |

$555 |

− $400 |

|

|

|

|

|

|

$1,062 |

− $600 |

|

|

|

|

|

|

$ |

− $1,000 |

|

|

|

|

$550 |

− $500 |

$2,775 |

− $2000 |

|

|

|

|

|

|

$5313 |

− $3000 |

|

|

|

|

|

|

$ |

− $5000 |

|

|

|

|

$1,100 |

− $1,000 |

$5,551 |

− $4000 |

|

|

|

|

|

|

$10,628 |

− $6000 |

|

|

|

|

|

|

$ |

− $10,000 |

|

|

|

|

|

|

|

|

|

|

|

|

and Kahneman for the rank-dependent weighting function, a probability weight of 0.5 would correspond to a probability of 0.36 for the gain and 0.64 for the loss. Thus, anyone who would turn down a 0.36 probability chance of winning $120 and a 0.64 probability of losing $100 would also turn down any bet that had a 0.64 probability of losing $600 no matter how much they could win with the other 0.36 probability. Similar results would hold for all of the examples in Table 10.2.

By itself this might not seem damaging to prospect theory because we could still argue that this result is abolished by the kink at reference point. However, this only shifts the problem. Consider, for example, the case where the person has the choice between a gain of $600 or a gamble that would yield either $720 with probability 0.36 or $500 with probability 0.64. If they would choose the $600, and classify it as a $600 gain, then they would also rather have $600 than any gamble that would yield $0 with probability 0.64, no matter how much could be had with the other 0.36 probability. Note that this argument only holds if the $600 is considered a gain. If instead it is incorporated in the reference point, the problem goes away as it did before. One might therefore argue that the $600 would be treated as the new reference point. Nonetheless, it is possible to engineer clever gambles for which it would seem inappropriate for the $600 to be treated as the reference point and that produce similar results. One must remember that models are approximations and simplifications of how decisions are made. Thus, it is always possible to push the limits of the model beyond its reasonable application. This may be especially true of behavioral models that are not intended to provide a single unifying theory of behavior but rather a contextually appropriate description of regularly observed phenomena.

EXAMPLE 10.6 Sweating the Small Stuff

EXAMPLE 10.6 Sweating the Small Stuff

When purchasing a home, a buyer is most often required by the lending agency to purchase some form of homeowners insurance. However, the bank generally gives homeowners wide flexibility in the structure of the insurance they purchase, allowing applicants to choose what types of added coverage they would like as well as the

|

|

|

|

|

272 |

|

PROSPECT THEORY AND DECISION UNDER RISK OR UNCERTAINTY |

deductible if a claim is filed. When purchasing insurance, a homeowner agrees to pay the insurance company an annual premium. In return, the insurance company agrees to write a check to the homeowner in the event of damage due to a specified list of events. This check will be enough to pay for repairs to the home or items in the home that are covered, minus the insurance deductible. For example, a homeowner who suffered $35,000 of damage from a tornado and who carried insurance with a $1,000 deductible would receive a check for $34,000. The deductible can also have an impact on whether a claim is filed. For example, a homeowner who suffered only $700 worth of damage would not likely file a claim if the deductible was $1,000 because the claim would not result in any payment by the insurance company.

The deductible allows the homeowner to share some of the risk with the insurance company in return for a lower annual premium. Also, because homeowners are offered a schedule of possible premiums and deductibles, the choice of deductible can offer a window into the homeowner’s risk preferences. A homeowner who is risk loving might not want the insurance in the first place, only buying it because the lender requires it. In this case, she will likely opt for a very high deductible, sharing a greater portion of the risk in return for a much lower average cost. For example, a home valued at $181,700 would be covered for premiums of $504 with a $1,000 deductible. The same home could be insured for an annual premium of $773 with a $100 deductible. Standard policies specify a $1,000, $500, $250, or $100 deductible. Justin Snydor used data from 50,000 borrowers to examine how buyers choose the level of deductible and also to examine the risk tradeoffs involved. The plurality of buyers (48 percent) chose a policy with a $500 deductible. Another 35 percent chose a $250 deductible. A much smaller percentage (17 percent) chose the $1,000 deductible, and a vanishingly small 0.3 percent chose the $100 deductible.

Table 10.3 displays the average annual premium offered to homeowners by level of deductible. Consider a risk-neutral homeowner who is choosing between a $1,000 deductible and a $500 deductible. Choosing the $500 deductible means that the homeowner will pay about $100 more  $715 − $615

$715 − $615 with certainty to lower the cost of repairs by $500 (the difference in the deductibles) in the event of damage greater than $500. We do not know the probability of filing a claim greater than $500. However, if we call the probability of filing a $500 claim p500, then a risk-neutral buyer should prefer the $500 deductible to the $1,000 deductible if

with certainty to lower the cost of repairs by $500 (the difference in the deductibles) in the event of damage greater than $500. We do not know the probability of filing a claim greater than $500. However, if we call the probability of filing a $500 claim p500, then a risk-neutral buyer should prefer the $500 deductible to the $1,000 deductible if

p500 |

$500 > $100 |

10 27 |

This implies that p500 > 0.20. Although we don’t know the actual probability of filing a claim, we know that only 0.043 claims were filed per household, meaning that a

Table 10.3 Homeowners Insurance Policies

|

Average |

Annual Number of Paid |

Percentage |

|

Deductible |

Annual Premium |

Claims per Household |

Selecting |

|

|

|

|

|

|

$1,000 |

$615.82 |

0.025 |

17 |

|

$500 |

$715.73 |

0.043 |

48 |

|

$250 |

$802.32 |

0.049 |

35 |

|

$100 |

$935.54 |

0.047 |

0.3 |

|

|

|

|

|

|

$801 − $716

$801 − $716 a year for a p

a year for a p

|

|

|

|

|

|

|

|

|

|

|

274 |

|

PROSPECT THEORY AND DECISION UNDER RISK OR UNCERTAINTY |

||||||

|

|

|

|

V x = |

x |

if x ≥ 0 |

10 31 |

||

|

|

|

|

βx if x < 0 , |

|||||

|

|

where β > 1. If homeowners value money outcomes according to equation 10.31, and if |

|||||||

|

|

they regard premiums as a loss, then the homeowner will prefer the $500 deductible to |

|||||||

|

|

the $1,000 deductible if |

|

|

|

|

|

|

|

|

|

|

π q V − 500 − 715 + 1 − π q |

V |

− 715 |

||||

|

|

|

> π q V |

− 1000 − 615 + 1 − π q |

10 32 |

||||

|

|

|

V − 615 |

||||||

|

|

or, substituting equation 10.31 into equation 10.32 |

|

|

|||||

|

|

|

β π q |

− 1215 + 1 − π q |

− 715 |

||||

|

|

|

> β π q − 1615 + 1 − π q |

|

10 33 |

||||

|

|

|

|

− 615 . |

|||||

|

|

Simplifying, the homeowner will prefer the smaller deductible if |

|||||||

|

|

|

|

|

π q |

> 0.25. |

|

10 34 |

|

|

|

|

|

|

|

||||

|

|

|

|

|

1 − π q |

|

|||

But given that the probability of a loss is closer to 0.04, and given the parameters of the weighting function presented earlier in the chapter, π q

q

1 − π

1 − π q

q

0.11. Thus probability weighting alone cannot account for the severely risk-averse behavior.

0.11. Thus probability weighting alone cannot account for the severely risk-averse behavior.

Segregation may be the key to this puzzle. If the homeowner did not perceive the premium as a loss (segregating the payment), prospect theory would suggest that she would then prefer the $500 deductible if the difference in the expected value of V between the two outcomes exceeds the change in price. Or,

π q V |

− 500 + 1 − π q V 0 − 715 |

|

> π q |

V − 1000 + |

10 35 |

1 − π q V 0 − 615. |

||

Note here that the value paid for the premium is not considered in the value function because it is segregated. Homeowners do not consider it a loss because it is a planned expense. Substituting equation 10.31 into equation 10.35 we obtain

− π q β500 − 715 > − π q β1000 − 615 |

10 36 |

or |

|

βπ q > 0.2. |

10 37 |

If we assume q  0.4, then π

0.4, then π q

q

0.1. Additionally, the value of β is commonly thought to be just above 2, suggesting that prospect theory with segregation of the annual premium might explain some insurance behavior.

0.1. Additionally, the value of β is commonly thought to be just above 2, suggesting that prospect theory with segregation of the annual premium might explain some insurance behavior.