vk.com/id446425943

Where to hide if you are bearish

Renaissance Capital

1 April 2019

Metals & Mining

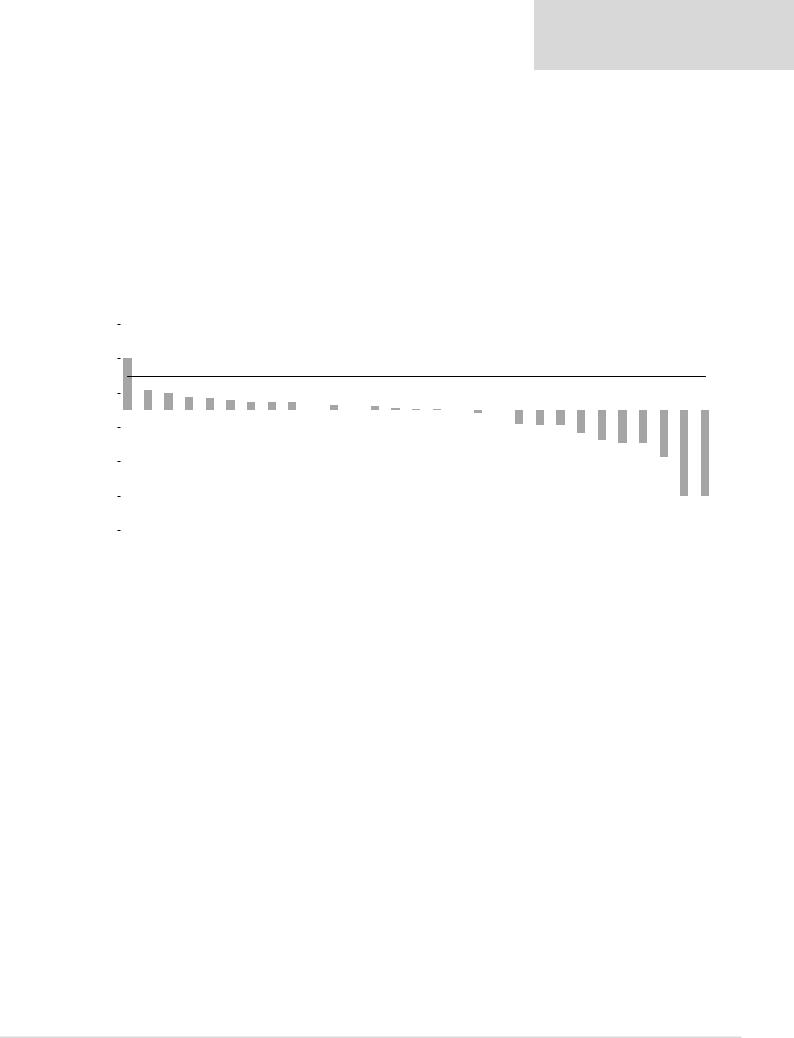

In a prolonged cyclical downturn in commodity prices, we believe capacity closures could be required to balance oversupplied markets. In this environment, we have a preference for companies with strong balance sheets and a competitive advantage through low-cost, long-life assets.

Figure 42 illustrates the CY21E FCF yields calculated using our trough commodity prices, which render around 50% of production cash-burning. 15 companies could be cash flow neutral or positive even at our trough commodity price assumptions due to their superior position on cost curves or defensive fixed margin type divisions.

In the analysis below, Rusal’s FCF yield is significantly higher than peers largely due to us using our base case dividends forecast from Norilsk Nickel. We only flex Rusal’s aluminium operations using trough prices.

Figure 42: CY21E FCF yields calculated using our trough commodity price assumptions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

25% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15%+ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6% |

5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Required rate of return, 10% |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

5% |

|

4% |

3% |

3% |

2% |

2% |

2% |

2% |

1% |

1% |

1% |

0% |

0% |

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

-5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1%- |

1%- |

|

|

4%- |

4%- |

5%- |

7%- |

9%- |

10%- |

10%- |

14%- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3%- |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-15% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-25% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-25%+ |

-25%+ |

|

|

-35% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Rusal |

Norilsk |

Polyus |

Vale |

Glencore |

Polymetal |

South32 |

Amplats |

Exxaro |

Diversified* |

Rio Tinto |

BHP |

Kumba |

Northam |

Sasol |

Assore |

Platinum* |

Anglo |

Gold* |

Impala |

Alrosa |

ARM |

Fortescue |

AngloGold |

RBPlats |

Gold Fields |

Sibanye |

Harmony |

Lonmin |

||||

|

|

||||||||||||||||||||||||||||||||

*Industry average. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Note: Priced as at market close on 26 March 2019.

Source: Thomson Reuters, Renaissance Capital estimates

23