vk.com/id446425943

Exxaro – BUY

Renaissance Capital

1 April 2019

Metals & Mining

Figure 115: Exxaro, ZARmn (unless otherwise noted)

|

|

|

|

Exxaro |

EXXJ.J |

Target price, ZAR: |

190 |

Market capitalisation, ZARmn: |

59,289 |

Last price, ZAR: |

164 |

Enterprise value, ZARmn: |

64,068 |

Potential 12-month return: |

26.5% |

Dec-YE |

2017 |

2018 |

2019E |

2020E |

2021E |

Income statement |

|

|

|

|

|

Revenue |

22,813 |

25,491 |

26,419 |

32,523 |

32,945 |

Underlying EBITDA |

7,207 |

7,280 |

7,151 |

8,266 |

8,285 |

Underlying EBIT |

5,814 |

5,699 |

5,330 |

6,219 |

6,328 |

Net operating profit |

975 |

5,703 |

5,330 |

6,219 |

6,328 |

Net interest |

-609 |

-316 |

-311 |

-391 |

-388 |

Equity accounted income |

3,952 |

3,259 |

5,721 |

4,837 |

4,182 |

Taxation |

-1,542 |

-1,653 |

-1,405 |

-1,632 |

-1,663 |

Minority interest in profit |

-50 |

-32 |

-82 |

-46 |

-24 |

Net profit for the year |

5,982 |

7,030 |

9,253 |

8,987 |

8,435 |

Headline earnings |

1,560 |

6,707 |

9,253 |

8,987 |

8,435 |

HEPS, ZAR |

5.02 |

26.72 |

36.85 |

35.79 |

33.59 |

Thomson Reuters consensus, ZAR |

|

|

27.09 |

25.49 |

24.40 |

Diluted HEPS, ZAR |

4.50 |

20.57 |

28.21 |

27.35 |

25.67 |

DPS declared, ZAR |

19.55 |

10.85 |

20.70 |

18.10 |

15.50 |

Underlying EBIT |

|

|

|

|

|

Eskom coal |

4,055 |

3,155 |

3,425 |

3,796 |

3,804 |

EBIT margin |

35% |

24% |

24% |

23% |

22% |

Export and other coal |

2,023 |

2,946 |

2,218 |

2,798 |

2,902 |

EBIT margin |

19% |

25% |

19% |

18% |

18% |

Ferrous |

46 |

14 |

6 |

6 |

6 |

Corporate and other |

-310 |

-416 |

-320 |

-380 |

-383 |

Underlying EBIT |

5,814 |

5,699 |

5,330 |

6,219 |

6,328 |

Group EBIT margin |

25% |

22% |

20% |

19% |

19% |

Pigment and mineral sands |

1,485 |

1,307 |

486 |

417 |

278 |

EBIT margin |

35% |

24% |

24% |

23% |

22% |

Iron ore |

3,334 |

3,293 |

6,600 |

5,240 |

4,415 |

EBIT margin |

35% |

24% |

24% |

23% |

22% |

Other equity accounted |

1,060 |

533 |

380 |

540 |

640 |

Proportionately consolidated EBIT |

11,693 |

10,832 |

12,796 |

12,416 |

11,661 |

Income statement ratios |

|

|

|

|

|

EBITDA margin |

32% |

29% |

27% |

25% |

25% |

EBIT margin |

25% |

22% |

20% |

19% |

19% |

HEPS growth |

-61% |

432% |

38% |

-3% |

-6% |

Dividend payout ratio on headline earnings |

327% |

41% |

80% |

72% |

66% |

Input assumptions |

|

|

|

|

|

ZAR/$ |

13.31 |

13.24 |

14.28 |

14.40 |

14.49 |

Iron ore fines (62% Fe, CIF China), $/t |

71 |

66 |

88 |

85 |

78 |

Thermal coal benchmark, $/t |

85 |

98 |

85 |

84 |

84 |

Export realisations, $/t |

69 |

77 |

67 |

69 |

73 |

Required breakeven price |

|

|

|

|

|

Export coal breakeven price, $/t |

77 |

82 |

75 |

72 |

72 |

Kumba Iron Ore breakeven price, $/t |

40 |

35 |

32 |

41 |

39 |

Sales volumes, kt |

|

|

|

|

|

Eskom coal - commercial |

15,151 |

12,361 |

14,961 |

17,408 |

15,700 |

GMEP Eskom |

8,500 |

12,500 |

12,500 |

12,500 |

12,500 |

Other domestic coal |

5,325 |

4,684 |

4,618 |

2,922 |

3,300 |

Export coal |

7,612 |

7,965 |

9,011 |

13,576 |

13,000 |

Iron ore - Sishen Iron Ore Company |

8,979 |

8,652 |

8,790 |

8,960 |

8,900 |

Copper equivalent volumes, kt |

537 |

464 |

496 |

546 |

533 |

Volume growth |

-1.7% |

-13.5% |

6.8% |

10.2% |

-2.4% |

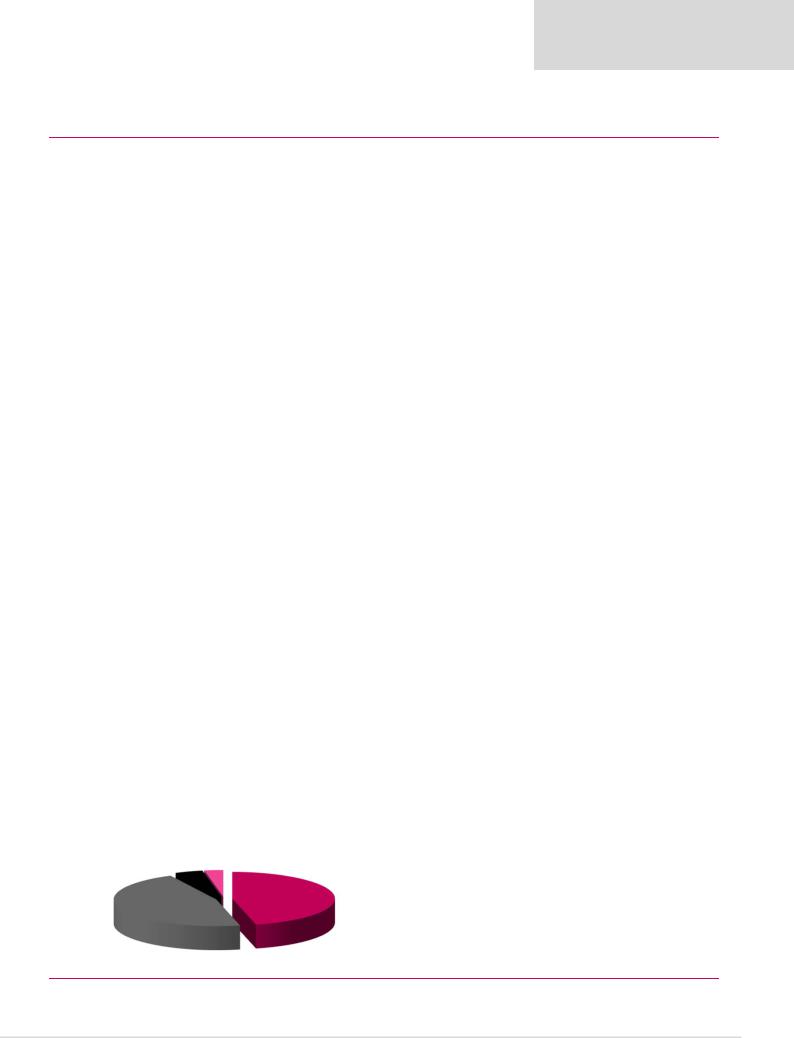

Contribution to proportionately consolidated FY19E attributable underlying EBITDA

Pigment & Sands |

Other |

|

|

3% |

Coal |

||

5% |

|||

|

|||

|

|

46% |

Iron ore 46%

Dec-YE |

|

|

|

|

2019E |

2020E |

2021E |

|

2017 |

2018 |

|

||||

Balance sheet |

|

|

|

|

|

|

|

Net operating assets |

|

21,702 |

28,100 |

|

31,047 |

33,013 |

34,178 |

Investment in associates |

|

17,289 |

17,046 |

|

16,660 |

16,552 |

16,729 |

Investments |

|

319 |

-134 |

|

-134 |

-134 |

-134 |

Equity |

|

40,103 |

41,846 |

|

45,467 |

47,838 |

50,444 |

Minority interest |

|

-738 |

-701 |

|

-685 |

-675 |

-671 |

Net debt |

|

-55 |

3,867 |

|

2,791 |

2,269 |

1,000 |

Balance sheet ratios |

|

|

|

|

|

|

|

Gearing (net debt/(net debt+equity)) |

|

-0.1% |

8.5% |

|

5.8% |

4.5% |

1.9% |

Net debt to EBITDA (<1.5x) |

|

0.0x |

0.4x |

|

0.2x |

0.2x |

0.1x |

RoCE |

|

25.7% |

21.4% |

|

22.8% |

20.8% |

18.8% |

RoIC |

|

18.4% |

15.3% |

|

19.3% |

17.0% |

13.5% |

RoE |

|

4.1% |

16.4% |

|

21.2% |

19.3% |

17.2% |

Cash flow statement |

|

|

|

|

|

|

|

Operating cash flow |

|

7,067 |

8,367 |

|

11,045 |

12,017 |

10,097 |

Capex (net of disposals) |

|

-3,921 |

-5,790 |

|

-6,447 |

-4,942 |

-3,142 |

Other cash flows |

|

2,233 |

-1,540 |

|

2,100 |

0 |

0 |

FCF |

|

5,379 |

1,037 |

|

6,698 |

7,075 |

6,955 |

Equity shareholders' cash |

|

5,110 |

1,561 |

|

6,708 |

7,138 |

7,098 |

Dividends and share buy-backs |

|

-3,715 |

-5,483 |

|

-5,632 |

-6,616 |

-5,829 |

Excess cash |

|

1,395 |

-3,922 |

|

1,076 |

522 |

1,269 |

Cash flow ratios |

|

|

|

|

|

|

|

Working capital days |

|

21 |

23 |

|

21 |

20 |

21 |

Capex/EBITDA |

|

54.4% |

79.5% |

|

90.2% |

59.8% |

37.9% |

FCF yield |

|

18.6% |

2.8% |

|

15.5% |

16.5% |

16.7% |

Cash conversion |

|

3.3x |

0.2x |

|

0.7x |

0.8x |

0.8x |

Equity shareholders' yield |

|

17.2% |

4.6% |

|

16.3% |

17.3% |

17.2% |

Valuation ratios |

|

|

|

|

|

|

|

P/E multiple |

|

26.2x |

6.6x |

|

5.8x |

6.0x |

6.4x |

Dividend yield |

|

16.6% |

8.0% |

|

12.6% |

11.0% |

9.4% |

EV/EBITDA |

|

3.3x |

3.8x |

|

3.9x |

3.2x |

3.4x |

P/B |

|

1.0x |

1.0x |

|

1.2x |

1.1x |

1.1x |

NAV per share, ZAR |

|

121 |

129 |

|

139 |

146 |

153 |

Valuation |

|

|

|

|

|

|

|

Calculation of target price |

|

|

|

|

ZARmn |

ZAR/sh |

|

Coal at DCF fair value |

|

|

|

|

29,302 |

87 |

|

Sishen Iron Ore Company at DCF fair value |

|

|

|

|

24,837 |

74 |

|

Tronox at market value |

|

|

|

|

6,479 |

19 |

|

50% interest in Moranbah South at $100mn |

|

|

|

|

1,440 |

4 |

|

Other at DCF fair value |

|

|

|

|

2,842 |

8 |

|

Attributable enterprise value |

|

|

|

|

64,900 |

192 |

|

Investments as at 31 December 2018 |

|

|

|

|

-134 |

-0 |

|

Net debt as at 31 December 2018 |

|

|

|

|

-3,867 |

-11 |

|

Share issues (buy-backs) during 2019E |

|

|

|

|

0 |

0 |

|

Other |

|

|

|

|

996 |

3 |

|

Equity value |

|

|

|

|

61,895 |

184 |

|

Plus: one-year forward equity shareholders' cash |

|

|

|

|

20 |

||

Less: dividends paid |

|

|

|

|

|

-18 |

|

One-year forward equity value |

|

|

|

|

|

186 |

|

TP, rounded to |

|

|

|

|

|

190 |

|

Share price on 26/3/2019 |

|

|

|

|

|

164 |

|

Expected share price return |

|

|

|

|

|

15.7% |

|

Plus: expected dividend yield |

|

|

|

|

|

10.7% |

|

Total implied one-year return |

|

|

|

|

|

26.5% |

|

Share price range, ZAR: |

|

|

|

|

|

|

|

12-month high on 19/3/2019 |

175 |

12-month low on 4/4/2018 |

103 |

||||

Price move since high |

-5.9% |

Price move since low |

|

60.1% |

|||

Calculation of discount rate |

|

|

|

|

|

|

|

WACC |

14.7% |

Cost of debt |

|

|

10.0% |

||

Risk-free rate |

9.0% |

Tax rate |

|

|

28% |

||

Equity risk premium |

5.0% |

After-tax cost of debt |

|

7.2% |

|||

Beta |

1.30 |

Debt weighting |

|

10% |

|||

Cost of equity |

15.5% |

Terminal growth rate |

|

3% |

|||

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

69