vk.com/id446425943

African Rainbow Minerals – BUY

Renaissance Capital

1 April 2019

Metals & Mining

Figure 110: African Rainbow Minerals, ZARmn (unless otherwise noted)

|

|

|

|

African Rainbow Minerals |

ARIJ.J |

Target price, ZAR: |

190 |

Market capitalisation, ZARmn: |

36,833 |

Last price, ZAR: |

166 |

Enterprise value, ZARmn: |

39,928 |

Potential 12-month return: |

23.1% |

Jun-YE |

2017 |

2018 |

2019E |

2020E |

2021E |

Income statement |

|

|

|

|

|

Revenue |

8,158 |

8,142 |

9,048 |

11,701 |

13,028 |

Underlying EBITDA |

922 |

1,799 |

2,333 |

4,250 |

5,098 |

Underlying EBIT |

214 |

1,058 |

1,579 |

3,487 |

4,192 |

Net interest |

-185 |

-183 |

-16 |

164 |

402 |

Equity accounted income |

3,446 |

4,129 |

5,345 |

5,177 |

3,910 |

Taxation |

409 |

-573 |

-321 |

-1,022 |

-1,286 |

Other |

-2,512 |

131 |

-1,639 |

-821 |

-850 |

Net profit for the year |

1,372 |

4,562 |

4,948 |

6,984 |

6,368 |

Headline earnings |

3,215 |

4,851 |

5,870 |

6,984 |

6,368 |

HEPS, ZAc |

1,684 |

2,526 |

3,033 |

3,613 |

3,294 |

Thomson Reuters consensus EPS, ZAc |

|

|

2,734 |

2,862 |

2,202 |

DPS declared, ZAc |

650 |

1,000 |

1,200 |

1,500 |

1,500 |

Underlying EBIT |

832 |

1,026 |

2,025 |

3,588 |

3,658 |

Platinum |

|||||

EBIT margin |

16% |

19% |

30% |

40% |

39% |

Nkomati |

120 |

18 |

-404 |

27 |

751 |

EBIT margin |

6% |

1% |

-34% |

2% |

29% |

Goedgevonden |

78 |

408 |

253 |

252 |

206 |

EBIT margin |

9% |

40% |

22% |

23% |

19% |

Other |

-816 |

-394 |

-295 |

-380 |

-423 |

Underlying EBIT |

214 |

1,058 |

1,579 |

3,487 |

4,192 |

Income statement ratios* |

|

|

|

|

|

EBITDA margin |

31% |

34% |

39% |

41% |

38% |

EBIT margin |

3% |

13% |

17% |

30% |

32% |

HEPS growth |

241% |

50% |

20% |

19% |

-9% |

Dividend payout ratio |

39% |

40% |

40% |

42% |

46% |

Input assumptions |

|

|

|

|

|

$/ZAR |

13.60 |

12.85 |

14.18 |

14.40 |

14.41 |

Platinum, $/oz |

988 |

940 |

827 |

875 |

920 |

Iron ore (62%Fe, CIF China), $/t |

69 |

67 |

75 |

88 |

83 |

Manganese ore (44%, CIF China), $/mtu |

5.72 |

6.79 |

6.45 |

5.24 |

5.41 |

Nickel, $/t |

10,134 |

12,474 |

12,504 |

13,584 |

15,496 |

Required breakeven price |

|

|

|

|

|

3PGMs, $/3PGM oz |

811 |

860 |

848 |

932 |

960 |

Nickel, $/t |

9,132 |

12,384 |

17,396 |

14,165 |

9,637 |

Iron ore, $/t |

37 |

46 |

32 |

41 |

50 |

Manganese ore, $/mtu |

3.84 |

4.71 |

5.34 |

4.47 |

4.53 |

Export thermal coal, $/t |

62 |

68 |

72 |

67 |

70 |

Sales volumes |

|

|

|

|

|

PGMs in concentrate - attributable, k oz |

324 |

316 |

309 |

312 |

316 |

Iron ore, kt |

8,638 |

8,937 |

8,726 |

8,700 |

8,700 |

Manganese ore, kt |

1,487 |

1,589 |

1,628 |

1,750 |

1,860 |

Nickel, t |

7,938 |

6,651 |

6,481 |

6,581 |

7,875 |

Attributable Cu eq volumes, kt |

287 |

287 |

274 |

282 |

290 |

Volume growth |

-1.3% |

0.2% |

-4.7% |

2.9% |

2.8% |

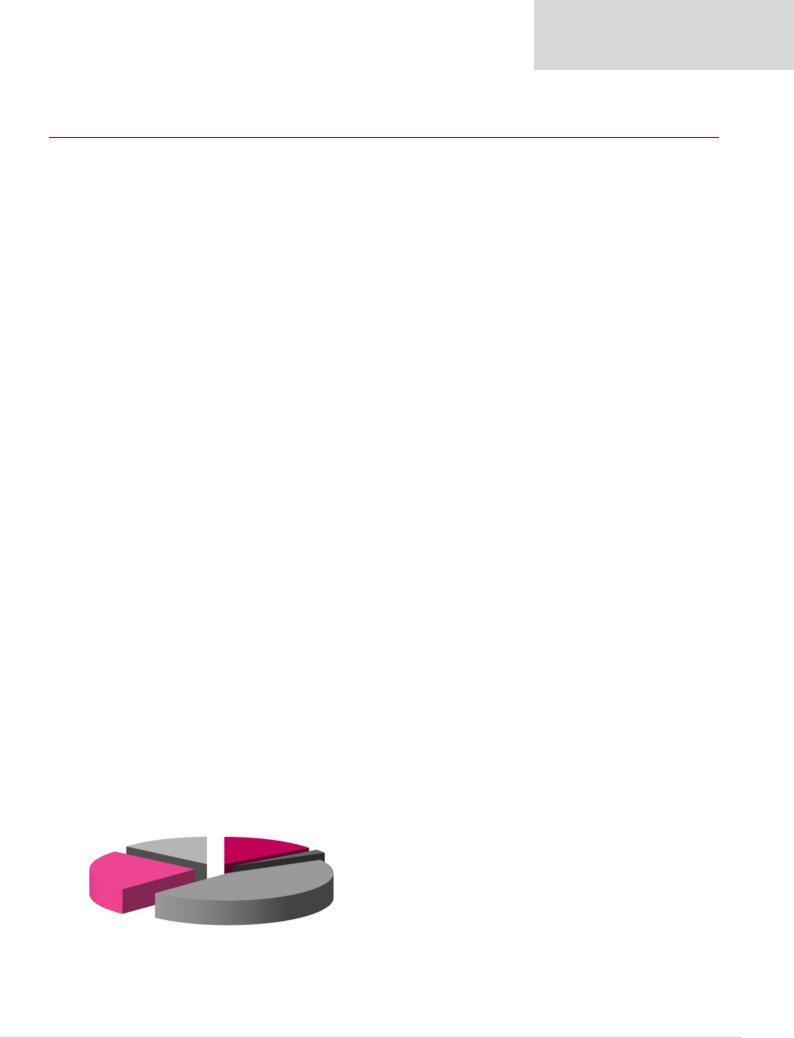

Contribution to FY19E attributable underlying EBITDA

Jun-YE |

|

|

2019E |

2020E |

2021E |

2017 |

2018 |

||||

Balance sheet |

|

|

|

|

|

Net operating assets |

23,738 |

24,822 |

26,231 |

25,998 |

26,082 |

Investments |

1,573 |

1,561 |

2,165 |

2,165 |

2,165 |

Equity |

23,497 |

25,907 |

29,069 |

32,915 |

36,145 |

Minority interest |

543 |

1,471 |

1,674 |

1,838 |

2,008 |

Net debt (cash) |

1,271 |

-995 |

-2,347 |

-6,590 |

-9,906 |

Balance sheet ratios |

|

|

|

|

|

Gearing* |

5.1% |

-4.0% |

-8.8% |

-25.0% |

-37.8% |

Net debt to EBITDA plus equity income |

0.3x |

-0.2x |

-0.3x |

-0.7x |

-1.1x |

RoCE (excluding Harmony) |

19.9% |

23.5% |

32.7% |

37.6% |

33.7% |

RoIC |

15.9% |

22.1% |

31.3% |

35.4% |

30.4% |

RoE |

13.5% |

19.5% |

21.3% |

22.5% |

18.4% |

*net debt/(net debt+equity) |

|

|

|

|

|

Cash flow statement |

|

|

|

|

|

Operating cash flow |

2,312 |

3,914 |

4,801 |

9,341 |

8,345 |

Capex (net of disposals) |

-981 |

-944 |

-1,287 |

-1,445 |

-1,524 |

Other cash flows |

2,030 |

1,179 |

215 |

0 |

0 |

FCF |

3,361 |

4,149 |

3,730 |

7,896 |

6,821 |

Equity shareholders' cash |

3,390 |

3,980 |

3,622 |

7,381 |

6,454 |

Dividends and share buy-backs |

-426 |

-1,714 |

-2,270 |

-3,138 |

-3,138 |

Movement in net debt |

2,964 |

2,266 |

1,352 |

4,243 |

3,316 |

Cash flow ratios |

|

|

|

|

|

Working capital days |

66 |

90 |

96 |

100 |

96 |

Capex/EBITDA |

106.4% |

52.5% |

55.1% |

34.0% |

29.9% |

Cash conversion |

1.1x |

0.8x |

0.6x |

1.1x |

1.0x |

FCF yield |

16.8% |

19.1% |

11.7% |

28.4% |

27.7% |

Equity shareholders' yield |

18.7% |

18.7% |

11.1% |

22.7% |

19.8% |

Valuation |

|

|

|

|

|

SoTP DCF valuation and calculation of target price |

|

|

ZARmn |

ZAR/sh |

|

Iron ore |

|

|

|

13,486 |

64.5 |

Manganese |

|

|

|

9,210 |

44.0 |

Two Rivers (effective interest = 54%) |

|

|

|

4,096 |

19.6 |

Modikwa (41.5%) |

|

|

|

2,061 |

9.8 |

Nkomati |

|

|

|

1,990 |

9.5 |

PCB Coal less debt (effective interest = 20.2%) |

|

|

1,838 |

8.8 |

|

Goedgevonden (effective interest = 26%) |

|

|

|

1,122 |

5.4 |

Copper and exploration |

|

|

|

0 |

0.0 |

Harmony at listed market value |

|

|

|

2,339 |

11.2 |

Corporate and other |

|

|

|

-1,929 |

-9.2 |

Enterprise value |

|

|

|

34,212 |

163.5 |

Net cash and other |

|

|

|

1,795 |

8.6 |

Equity value |

|

|

|

36,007 |

172.1 |

Plus: equity shareholders' cash/share |

|

|

|

|

33.2 |

Less: DPS |

|

|

|

|

-14.2 |

TP, rounded to |

|

|

|

|

190.0 |

Share price on 26/3/2019 |

|

|

|

|

166.0 |

Expected share price return |

|

|

|

|

14.5% |

Plus: expected dividend yield |

|

|

|

|

8.6% |

Total implied one-year return |

|

|

|

|

23.1% |

Share price range, ZAR:

|

|

|

12-month high on 28/3/2019 |

175 |

12-month low on 4/4/2018 |

90 |

|||

|

|

|

Price move since high |

-3.7% |

Price move since low |

|

86.6% |

||

|

Coal |

Platinum |

Calculation of discount rate |

|

|

|

|

|

|

|

15% |

|

|

|

|

|

|

||

|

14% |

|

|

|

|

|

|

|

|

|

|

WACC |

16.8% |

Cost of debt |

|

|

10.0% |

||

|

|

|

|

|

|||||

|

|

Nickel |

Risk-free rate |

9.0% |

Tax rate |

|

|

28% |

|

|

|

-2% |

Equity risk premium |

6.0% |

After-tax cost of debt |

|

7.2% |

||

|

|

|

Beta |

1.30 |

Debt weighting |

|

0.0% |

||

|

|

|

Cost of equity |

16.8% |

Terminal growth rate |

|

2.0% |

||

|

|

|

Valuation ratios |

|

|

|

|

|

|

Manganese |

|

|

Jun-YE |

2017 |

2018 |

|

2019E |

2020E |

2021E |

24% |

|

Iron ore |

P/E multiple |

5.7x |

4.4x |

|

5.6x |

4.7x |

5.1x |

|

|

Dividend yield |

6.8% |

9.0% |

|

7.1% |

8.9% |

8.9% |

|

|

|

45% |

|

||||||

|

|

EV/EBITDA |

4.6x |

3.7x |

|

4.2x |

3.0x |

2.7x |

|

|

|

|

|

||||||

|

|

|

P/B |

0.8x |

0.8x |

|

1.1x |

1.0x |

0.9x |

|

|

|

NAV per share, ZAR |

124 |

136 |

|

150 |

170 |

187 |

* Proportionately consolidated

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

64