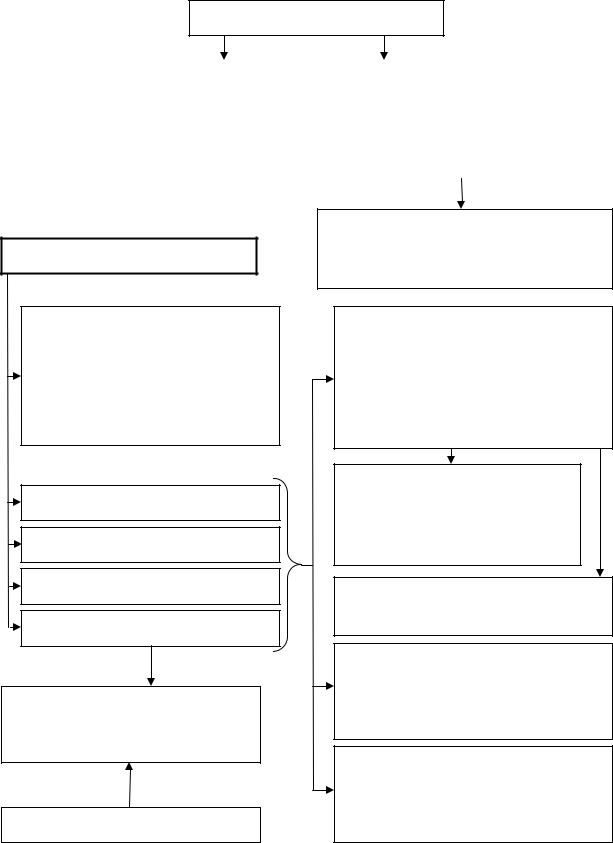

10.3. AML/CFT requirements for financial institutions with foreign operations

Financial institution that has |

|

There has to be the group- |

foreign operations (R. 18, IN) |

|

level AML/CFT program |

|

|

|

|

|

Foreign branches |

|

|

|

|

|

|

|

||

Home country operations |

|

|

|

Foreign majority-owned |

|||

|

|

||

|

|

subsidiaries |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AML/CFT measures applied |

||

|

AML/CFT requirements of |

|

|

to these operations have to be |

||

|

the home country |

|

|

consistent with the home |

||

|

|

|

|

country requirements |

||

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

To the extent the host country |

|

|

|

|

AML/CFT regulations permit |

|

|

|

|

|

|

|

|

|

|

|

Should apply additional |

|

|

|

|

|

|

|

||

measures to manage the |

|

|

If AML/CFT legislature of the |

|

ML/TF risks |

|

|

host country does not permit |

|

|

|

|

the implementation of |

|

|

|

|

||

|

|

|

|

|

Should inform |

|

|

|

|

|

|

|

|

|

If these measures are not sufficient

Home country supervisors

Should consider additional supervisory actions, including

82

Placing additional controls on the group

As appropriate

Requesting the group to close down operations in the host country

10.4. Customer due diligence and record-keeping requirements for designated non-financial businesses and professions

Apply to DNFBPs in the following situations, R. 22

Casinos

Dealers in precious metals

Dealers in precious stones

Real estate agents

CDD measures, R. 10

Record keeping, R. 11

PEPs, R. 12

New technologies, R. 15

Reliance on third parties, R. 17

When customers engage in financial transactions equal or above the 3,000

USD/EUR applicable threshold

When they engage in any cash transaction equal or above the 15,000 USD/EUR applicable threshold

|

|

|

|

|

|

When they are involved in transactions for |

|

|

|

|

|

Buying and selling |

||||||||||||||||||

|

|

|

|

|

|

|

their client concerning the |

|

|

|

|

|

|

|

|

|

|

|

of real estate |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lawyers |

|

|

|

|

|

|

Managing of |

|

|

|

|

Bank ac- |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

counts |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

Notaries |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Money |

|

|

|

|

|

|

|

|

|

|

Savings ac- |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

Independent legal professionals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

counts |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Securities |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

Independent accountants |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Securities ac- |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other assets |

|

|

|

|

|

|

counts |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

Organization of con- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

Legal persons and their arrangements |

||||||||||||||||||||

|

|

|

|

|

|

|

tributions for the |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

(companies, business entities) |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Creation, operation or |

|

|

|

|

|

|

Prepare for or carry out transac- |

||||||||||||||||

|

|

|

|

|

|

|

management of |

|

|

|

|

|

|

|

tions for a client concerning all |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

activities listed in the definition |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

Trust and company service providers |

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

of TCSPs |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

83 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

10.5. Other AML/CFT requirements for designated non-financial businesses and professions

CDD measures, R. 10

Real estate agents should imple- |

|

Casinos should implement |

ment these measures with respect |

|

these measures when their cus- |

to both purchasers and vendors of |

|

tomers engage in a financial |

the property |

|

transaction equal or above the |

|

|

applicable threshold |

|

||

|

|

|

|

Casinos must be able to link CDD |

|

Reporting requirements |

information for a particular custom- |

|

er to his transactions in the casino |

||

|

||

Dealers in precious metals and |

It is not required to report suspi- |

|

dealers in precious stones |

cious transactions if the relevant |

|

should report suspicious cash |

information was obtained in cir- |

|

transactions with a customer |

cumstances where the persons are |

|

equal or above the applicable |

subject to professional secrecy or |

|

designated threshold |

legal professional privilege |

|

Lawyers |

(a) In performing the task of |

|

defending or representing the |

||

Notaries |

client in judicial and other |

|

proceedings |

||

Independent legal professionals |

(b) In the course of ascertaining |

|

|

||

Independent accountants |

the legal position of the client |

|

|

||

|

STRs can be sent to appropriate |

|

Reporting activities should be |

self-regulatory organizations, |

|

provided that they cooperate with |

||

extended to all professional ac- |

the FIU |

|

tivities of accountants |

If these persons seek to dissuade a |

|

|

||

|

client from engaging in illegal ac- |

|

Including auditing |

tivity, this does not amount to tip- |

|

ping-off |

||

|

84 |