2. The law of diminishing marginal returns

The law of diminishing marginal returns states that the extra production obtained from increases in a variable input will eventually decline as more of the variable input is used together with the fixed inputs.

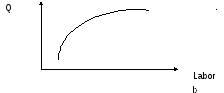

Total product curve and marginal product curve

A total product curve describes how output varies in the short run as more of any one input is used together with fixed amounts of other inputs under current technology. Points on a total product curve give the output that's obtainable, given current technology, from any quantity of the variable input used with the fixed inputs.

The total product of a variable input such as labor services, is the amount of output produced over any given period when that input is used along with other fixed inputs (fig. 6.1).

Figure 6.1. Total product of labor

The marginal product of an input is the increase in output from one more unit of that input when the quantity of all other inputs is unchanged. Marginal product (MPL) is:

MPL=ΔTotalP/ΔLabor,

where ΔTP – the change in the total product of labor;

ΔL – the increase number of workers hired per week.

When the marginal product of labor is zero, total product is at its maximum value per period.

This is because at the point where MPL is zero, hiring another worker doesn't add to production anymore, and hiring still one more worker would begin to reduce output.

When marginal product is negative, additional workers decrease weekly production (figure 6.2).

Figure 6.2. Marginal product of labor

Average Product

The average product of an input is the total output produced over a given period divided by the number of units of that input used.

The average product labor is therefore total product (TP) divided by the number of workers (L):

Average product of labor = TP/L.

The average product measures output per worker, which is an indication of the productivity of workers in a plant (figure 6.3).

Figure 6.3. Average product of labor

Remember: when the marginal product falls below the average product of an input, the average product declines уменьшатся. This means the law of diminishing marginal returns also implies that the average product of a variable input will eventually decline as more of that input is used together with fixed inputs.

3. Variable costs, fixed costs, and total costs

In the short run, costs are divided into two basic categories:

1) Fixed costs (FC) are those that do not vary as a firm varies its output. Managers often refer to their fixed costs as over headed costs. These are costs that must be incurred подвергается in the short run even if the firm doesn't produce anything.

2) Variable costs (VC) are those that change with output. These are the costs variable inputs.

Total cost (TC) is the sum of the value of all inputs used over any given period to produce goods. Total cost is the sum of fixed costs and variable costs:

TC = VC + FC

Average cost (AC) is total cost divided by the number of units of output produced over a given period. It's also called average total cost. Managers often refer average cost as their unit cost:

AC=TC/Q

Average variable cost (AVC) is variable cost divided by the number of units of output produced over a given period:

AVC= VC/Q

Average fixed cost (AFC) is fixed cost divided by the number of units of output produced over a given period:

AFC=FC/Q

It's easy to show that average cost is the sum of average variable cost and average fixed cost. Remember that total cost is the sum of variable cost and fixed cost. It follows that:

TC/Q=VC/Q+FC/Q

The two terms on the other side of the equal sign are AVC and AFC, respectively. It follows that:

AC = AVC + AFC

Marginal cost (MC) is the extra cost of producing one more unit of output. There is no accounting concept that parallels marginal cost. However, all good business managers have an idea of their marginal cost and use their estimates of marginal cost of production to make decisions:

MC=ΔTC/ΔQ,

where ΔTC is the change in total cost associated with any given change output, ΔQ.