vk.com/id446425943

Goldman Sachs

Credit Outlook

Packaging: Karl Blunden

Sector View

We have an Attractive view on HY Packaging. In short, we think pricing power in packaging is underappreciated. We expect packaging business models to outperform the broader market in 2019 as (1) cost inflation headwinds moderate (resin prices declining and truck spot rates leveling off) and (2) lagged pass-throughs (and increasingly shared freight costs) translate to higher EBITDA/FCF generation. While packaging has historically been seen as a defensive and highly cash-generative sector, this view was called into question in 2018 as cost inflation coupled with slow growth drove down public equity multiples, and with them, bond prices. We believe investor sentiment is currently at a low point, and expect stable earnings forecasts to drive material upgrades in investor sentiment toward the space (e.g. the 10% move on BERY’s stable 3Q results).

Data points supporting our expectation for an inflection in pricing success in the

sector have just begun to emerge. Of note, BERY indicated on its 3Q earnings that it will recapture ~50% of cost inflation headwinds and attain high-single digit EBITDA growth in F2019 (with upside to earnings if oil prices decline). Importantly, we think cost recapture could be even better at companies who operate in more consolidated substrates (e.g. metal) than Berry (resins). In addition, we acknowledge that a macro “fear discount” could drive weakness in more levered names (despite our belief that fundamentals will remain sound), but we think idiosyncratic strengths will lead to spread compression at companies such as Ardagh (diversified earnings and refi commitment) and BWAY (synergy capture drives EBITDA growth).

Our top trade idea in the sector is to (1) Buy ARDFIN 7.125% 2023s (on our HY CL) to

benefit from being called by 2020 - offering a double digit total return opportunity under a wide range of market conditions. Outside of Ardagh, we see other opportunities in (1) BWY (OP), as synergy realization, above-average organic growth rates, and focus on debt reduction should help the complex outperform industry peers, and (2) BERY (IL), where for those with a view on M&A, the potential for an LBO skews risk/reward to the upside in the 2026s (which trade ~10 points below their MW price).

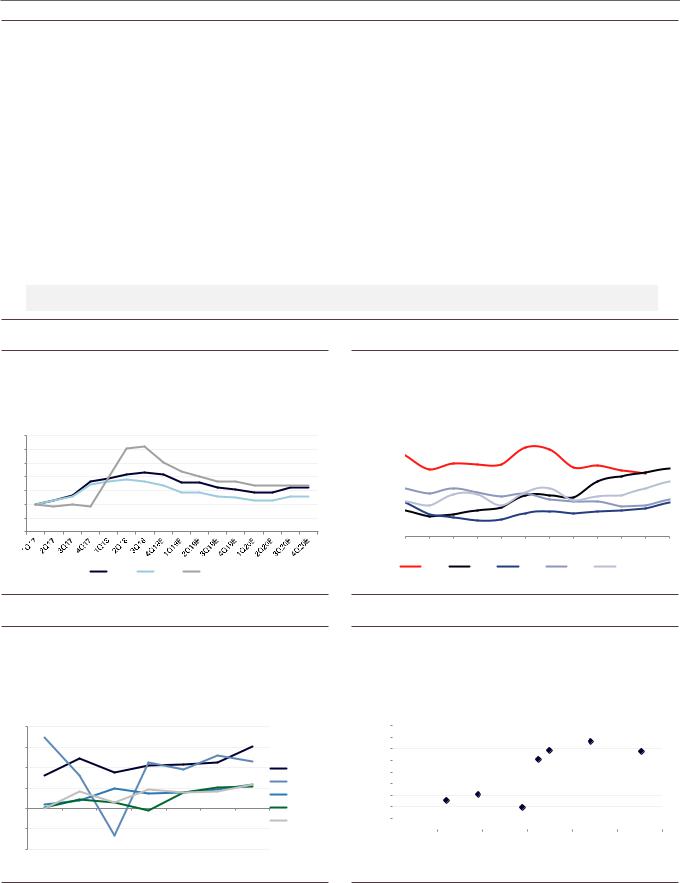

Exhibit 101: Packaging could outperform the market as macro concerns escalate (similar to previous downturn), despite underperforming in 2018

YTW (%)

|

25% |

2008: HY Packaging trades 630bp |

2018 |

1,000 |

||

|

20% |

|

800 |

|

||

(%)YTW |

inside the HY Market |

|

(bp)Spread |

|||

15% |

|

Today: HY packaging trades 135bp |

600 |

|||

|

10% |

|

inside the HY Market |

|

400 |

|

|

|

|

|

|

||

|

5% |

|

|

|

200 |

|

|

0% |

|

|

|

0 |

|

|

-5% |

|

|

|

-200 |

|

|

|

Market discount vs Packaging |

HY Market Index |

HY Packaging Index |

|

|

Exhibit 102: Sector-wide cost inflation has driven Packaging companies to trade at the low end of their historical range

Current Packaging EBITDA multiples relative to 5-year range

Multiple |

15x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

13x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

EBITDA |

11x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

9x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BLL |

SEE |

SON |

CCK |

SLGN BERY |

ARD |

GPK |

OI |

Current Multiple Relative to 5-year Peak

Source: The Yield Book.; FTSE Index |

Source: FactSet, Goldman Sachs Global Investment Research |

4 December 2018 |

46 |

vk.com/id446425943

Goldman Sachs

Credit Outlook

Exhibit 103: The selloff in 2018 (particularly in more levered companies) leaves incremental upside in names where idiosyncratic catalysts will help to offset broader macro concerns (ARGID/ARDFIN and BWY)

Relative value summary

|

ARGID |

BWY |

BERY |

REYNOL |

BLL |

|

Ardagh |

BWAY |

Berry Plastics |

Reynolds |

Ball Corp |

GS Rating |

OP |

OP |

IL |

IL |

U |

|

Holdco refi drives upside in |

Cash generation and synergy |

Most bonds at fair value, but |

Call constraints limit upside |

Equity remuneration and tight |

Catalysts |

select opco notes as well as |

2026s have upside catalyst in |

although asset sales could |

valuation leave us negative on |

|

|

ARDFIN/ARDSECs |

capture drive deleveraging |

LBO scenario |

accelerate debt reduction |

the complex |

|

|

||||

|

|

|

|

|

|

Revenue |

$9,109 |

$3,655 |

$7,696 |

$10,625 |

$11,579 |

EBITDA |

$1,475 |

$694 |

$1,386 |

$1,924 |

$1,894 |

EBITDA Margin |

16% |

19% |

18% |

18% |

16% |

Free Cash Flow |

$167 |

($1) |

$613 |

$391 |

$850 |

Net Leverage (LTM) |

6.4x |

7.5x |

4.0x |

5.5x |

3.2x |

Net Leverage (2019) |

5.8x |

6.3x |

3.0x |

5.0x |

3.0x |

Net Leverage (2020) |

5.4x |

5.6x |

2.4x |

4.5x |

2.5x |

|

|

|

|

|

|

Coupon |

7.250% |

7.250% |

5.125% |

7.000% |

5.250% |

Maturity |

5/15/2024 |

4/15/2025 |

7/15/2023 |

7/15/2024 |

7/1/2025 |

Outstanding (mn) |

1650 |

1350 |

700 |

800 |

1000 |

S&P / Moodys |

B/B3 |

CCC+/Caa2 |

BB-/B2 |

B-/Caa1 |

BB+/Ba1 |

Bid Price |

101.5 |

91.25 |

99.25 |

100 |

101.75 |

YTW (%) |

6.8% |

9.1% |

5.3% |

7.0% |

4.9% |

OAS (bp) |

379 |

621 |

234 |

384 |

205 |

Setup into 2019 |

Levered names have sold off on sector headwinds YTD...but defensive business models and reliable cash generation should drive sector outperformance |

|

amidst fears of macro weakness |

||

|

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg

Exhibit 104: Raw material cost inflation is set to moderate, which should allow the industry’s lagged pass-throughs to be EBITDA contributors in 2019

Raw material prices, indexed to 1Q17

150 |

|

|

140 |

|

Rapid cost inflation negatively impacted |

130 |

|

packaging earnings in 2018... |

|

|

|

120 |

|

|

110 |

|

|

100 |

|

...but input costs are moderating in |

90 |

|

|

|

2019, translating to easier y/y comps |

|

|

|

|

80 |

|

|

HDPE |

LDPE |

Steel (HRC) |

Exhibit 105: Despite freight costs staying high, packaging credits (particularly in consolidated markets) should begin to have positive comps in 2019 as they share cost inflation with customers

Spot Freight Rates

Rate |

|

$2.10 |

|

|

|

|

|

|

|

|

|

|

|

|

$2.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LinehaulSpotTruck |

fuel)-ex($/mile |

$1.90 |

|

|

|

|

|

|

|

|

|

|

|

$1.80 |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$1.70 |

|

|

|

|

|

|

|

|

|

|

|

|

|

$1.60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

$1.50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

$1.40 |

|

|

|

|

|

|

|

|

|

|

|

DAT |

|

$1.30 |

|

|

|

|

|

|

|

|

|

|

|

|

$1.20 |

Feb |

Mar |

Apr |

May |

Jun |

|

Aug |

Sep |

Oct |

Nov |

Dec |

|

|

Jan |

Jul |

|||||||||||

|

|

|

2018 |

|

2017 |

|

2016 |

|

2015 |

|

2014 |

|

|

Source: Chemical data, Bloomberg, Goldman Sachs Global Investment Research

Exhibit 106: Easing cost comparisons and modest growth should help drive FCF generation across our coverage

FCF as % of debt

20% |

|

|

|

|

|

|

15% |

|

|

|

|

|

|

10% |

|

|

|

|

|

BERY |

5% |

|

|

|

|

|

BLL |

|

|

|

|

|

REYNOL |

|

|

|

|

|

|

|

|

0% |

|

|

|

|

|

BWAY |

-5% |

|

|

|

|

|

ARGID |

|

|

|

|

|

|

|

-10% |

|

|

|

|

|

|

FY14 |

FY15 |

FY16 |

FY17 |

FY18E |

FY19E |

FY20E |

Source: DAT data, Goldman Sachs Global Investment Research

Exhibit 107: Despite idiosyncratic strengths at ARGID (diversification and refi commitment) and BWY (synergy capture) that should keep fundamentals sound, we acknowledge that levered names are more susceptible to pricing in of macro fears

YTD change in YTW and net leverage by company

|

360 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

(bp) |

320 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ARDFIN |

|

|

|||

280 |

|

|

|

|

|

|

REYNOL |

BWAY |

|||

|

|

|

|

|

|

|

|||||

YTWin |

|

|

|

|

|

|

|

||||

200 |

|

|

|

|

|

|

|

|

|

|

|

|

240 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ARGID |

|

|

|

change |

160 |

|

|

|

BLL |

|

|

|

|

|

|

|

|

|

|

|

BERY |

|

|

|

|

|

|

|

120 |

|

|

|

|

|

|

|

|

|

|

YTD |

80 |

|

|

|

|

|

CCK |

|

|

|

|

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

0 |

|

|

|

|

|

|

|

|

|

|

|

2.0x |

3.0x |

|

4.0x |

5.0x |

6.0x |

7.0x |

8.0x |

|||

Net leverage

Source: Company data, Goldman Sachs Global Investment Research |

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg |

4 December 2018 |

47 |

vk.com/id446425943

Goldman Sachs

Best idea

Credit Outlook

Trade idea: Buy ARDFIN 7.125% 2023s (on our HY CL) to benefit from being called

by 2020 - offering a double digit total return opportunity. With management’s stated intent to refinance its holdco notes and our expectation that Ardagh posts stable EBITDA growth in 2019, we think the ARDFINs are likely to be taken out early in a transaction facilitated by the issuance of new opco debt (at the secured level if market conditions are weak) and $800-900mn of holdco debt pay down (based on our estimate that Ardagh’s current RP capacity grows to these levels by late 2019). This would provide liquidity to current holders of class-B private shares (management’s stated goal) while also preserving an acceptable LTV for new holdco notes (~$1.4bn would remain in this scenario) as the holdco note size would decrease along with the number of shares in the collateral package. With ARDFINs trading at $94.50 (7-9 points below their 2019/2020 call prices), we see upside from current levels regardless of whether Ardagh initiates a holdco refinancing transaction in 2019 or 2020.

We note that several risks (e.g. broader macro weakness, sector-wide cost headwinds) have the potential to drive variance in Ardagh’s earnings trajectory, but we believe there are multiple paths for Ardagh to complete the holdco refinancing and for investors to invest across the credit capital structure. In a more bearish scenario where slowing company fundamentals magnify RP constraints, we see opportunity in the ARGID

7.25% 2024s or the secured ARGID 4.625% 2023s as these bonds could be targeted in a refi or consent process, respectively (given that these bonds have the tightest RP limitations) to free up additional RP capacity that would reduce the required size of a new holdco note. Ardagh would be able to issue more opco debt (vs our base case above), upstream additional cash that is no longer bound by our estimated $800-900mn of RP capacity (provided opco leverage remains below 5.25x), and pay down holdco debt (which also supports our view that the ARDFIN 2023s are likely to come out regardless of market conditions). See here for more detail on the paths to a holdco refi.

Fundamentally, we think Ardagh’s diversified business and leading market position across the various markets it serves will help mitigate its downside exposure to credit market weakness, and put it in a position to pursue its stated goal of refinancing its holdco notes. In 2019, we expect a resumption of earnings growth and improved cash generation to support gradual deleveraging at the credit.

Risks to our view: Leveraging M&A and credit market weakness.

Exhibit 108: Ardagh fundamentals are strong enough to support a holdco refinancing...

Ardagh FCF, EBITDA, and net leverage through 2020

Exhibit 109: ...which we think will drive the ARDFIN 7.125% 23s and the ARGID 7.25% 2024s to price in the chance of early takeout

OAS (bp)

$2,000 |

|

|

|

|

|

|

|

8.0x |

|

700 |

|

|

|

|

|

|

|

(bp) |

600 |

||

$1,500 |

|

|

|

|

|

|

|

6.0x |

||

|

|

|

|

|

|

|

500 |

|||

$1,000 |

|

|

|

|

|

|

|

4.0x |

400 |

|

|

|

|

|

|

|

|

OAS |

|||

$500 |

|

|

|

|

|

|

|

2.0x |

300 |

|

|

|

|

|

|

|

|

200 |

|||

|

|

|

|

|

|

|

|

|||

$0 |

|

|

|

|

|

|

|

0.0x |

|

100 |

($500) |

|

|

|

|

|

|

|

-2.0x |

|

|

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018E |

2019E |

2020E |

|

|

|

EBITDA |

|

FCF |

|

Net opco leverage |

|

Net holdco leverage |

|

|

|

|

We see incremental tightening potential in the ARGID 7.25% 24s relative to the ARGID 25s as the 25s are worse off in most refi scenarios

ARGID 4.625% 2023 |

|

ARGID 7.25% 2024 |

|

||

ARGID 6% 2025 |

|

ARDFIN 7.125% 2023 |

|

Source: Company data, Goldman Sachs Global Investment Research |

Source: Bloomberg |

4 December 2018 |

48 |

vk.com/id446425943

Goldman Sachs

Credit Outlook

Retail: Jenna Giannelli

Sector View: Neutral, but performance idiosyncratic

Fewer macro top line tailwinds in FY19...

We recently initiated coverage on the High Yield Retail sector with a Neutral coverage view and maintain this view looking into 2019. We have a generally tepid view of the earnings and macro backdrop, and are cautious of putting much weight on favorable macro data (confidence, housing, employment, wages, disposable income) as these variables were largely positive in recent years but did not lead to better retailer performance. We believe the tailwinds from tax cuts, a favorable macro environment and FX will taper in FY19, and that much of the top-line growth (if any, depending on the issuer) will be driven by select outperforming assets (I.e. Madewell, mytheresa, Chewy, Bath & Body Works), company specific initiatives, and for some, square footage expansion.

... and margin, inflationary pressures to persist; tariffs unknown

Offsetting these factors include ongoing traffic and competitive challenges, currency, commodity and freight cost headwinds, as well as store closures. Moreover, tariffs present considerable uncertainty around the 2019 outlook as we wait for further updates on trade policy, as well as our issuers’ ability to offset headwinds with pricing, moved production and cost savings. Finally, concerns over inadequate covenants is a continued focus in our sector, tempering our enthusiasm for some of the more levered and private issuer names in our universe.

‘18 Holiday likely solid but less so than ‘17

We think Holiday ‘18 results could pose the first risks of disappointment, as we are set up to deliver a solid but not as strong season as Holiday ‘17, that we believe benefited from a) comping out of the ‘16 election cycle b) announced tax cuts driving better sentiment at Christmas c) steady / strong oil markets, supporting spend in those regions d) very favorable weather vs. the prior 3 years. Further, heightened department store closures and online penetration reaching all-time highs this season could put incremental pressure on margins.

Retailer constituent health, however, has improved...

Somewhat offsetting this tepid macro view, however, is the improved health of retail constituents. With a number of bankruptcies behind us, the leverage, cash flow and maturity profiles of the sector as a whole are healthier, limiting the sectors’ “tail risk”. For context, the average retailer leverage in our universe stands at 5.0x, high, but still notably less than nearer to 7.0x at the end of 2016. We further estimate that most issuers in our universe will be FCF neutral or positive in FY19.

4 December 2018 |

49 |

vk.com/id446425943

Goldman Sachs

...And performance concentrated

Credit Outlook

Further, year-to-date returns have been largely idiosyncratic rather than thematic, and retailer earnings performance has varied depending on the categories and channels in which they operate. To illustrate, the retail sector has performed nearly in line with the HY index year-to-date and in the last 3 months, but with notable interim volatility (periods of significant outperformance and underperformance). From an issuer standpoint, four issuers have driven nearly all of the sectors’ performance including: Neiman Marcus Group (Underperform), PetSmart (not covered), L Brands (Outperform) and JC Penney (In-Line), underpinning our thesis that performance will continue to be dependent on security and issuer selection as opposed to sector allocation and thus supportive of our Neutral view.

Exhibit 110: Credit Fundamentals: Retail credit health improves, less tail risk but leverage is still high

Retailer Gross Leverage Metrics

Company |

FY16 |

FY17 |

FY18E |

FY19E |

Hanesbrands Inc |

3.6x |

3.8x |

4.0x |

4.0x |

J Crew Group Inc |

11.1x |

7.7x |

8.7x |

8.2x |

J.C. Penney Co |

4.6x |

4.2x |

7.2x |

7.2x |

L Brands Inc |

2.2x |

2.5x |

2.7x |

2.6x |

Neiman Marcus Group |

8.1x |

11.0x |

9.9x |

9.7x |

Party City Holdings |

4.3x |

4.5x |

4.3x |

4.0x |

Rite Aid Corp |

6.7x |

7.0x |

6.3x |

6.7x |

Sally Beauty Holdings |

2.9x |

3.0x |

3.1x |

3.4x |

Tailored Brands |

4.5x |

4.0x |

3.1x |

3.1x |

|

|

|

|

|

Exhibit 111: Industry trends are mixed. Mall traffic declines have moderated, but performance is still largely category and channel dependent

10%

6%

6%

2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2% |

1% |

|

|

1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

-1% |

|

|

|

|

-1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-3% |

|

|

|

|

-1% |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-4% |

|

|

|

|

|

|||

-6% |

|

|

|

|

|

|

|

|

|

|

-3% |

-5% |

|

|

|

|

|

|

||||

-6% |

|

-6% |

|

|

|

|

|

-5% |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

-10% |

|

|

|

-7% |

|

-9% |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

-10% |

|

|

-8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

-11% |

-9% |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

-14% |

|

|

-11% |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Jan-17 |

Feb-17 |

Mar-17 |

Apr-17 |

May-17 |

Jun-17 |

Jul-17 |

Aug-17 |

Sep-17 |

Oct-17 |

Nov-17 |

Dec-17 |

Jan-18 |

Feb-18 |

Mar-18 |

Apr-18 |

May-18 |

Jun-18 |

Jul-18 |

Aug-18 |

Sep-18 |

||

|

||||||||||||||||||||||

|

Average |

5.0x |

5.0x |

5.1x |

5.0x |

|

|

|

|

|

|

|

|

|

|||

Source: Goldman Sachs Global Investment Research, Company reports |

|

|

|

|

Source: Goldman Sachs Global Investment Research, ShopperTrak |

|||

Exhibit 112: Technicals: Retail returns in the L3M and YTD are in line with the market, but performance has been concentrated and volatile

Index |

% YTW |

OAS |

Duration |

MTD % Total |

YTD % |

|

|

|

|

Return |

Total Return |

High Yield Index |

7.2% |

418 |

4.35 |

-0.86% |

0.06% |

High Yield Retailers |

8.8% |

583 |

4.38 |

-0.68% |

0.12% |

BB Index |

5.8% |

275 |

4.77 |

-0.25% |

-1.12% |

B Index |

7.2% |

416 |

4.11 |

-0.75% |

0.90% |

CCC Index |

11.1% |

809 |

3.76 |

-2.84% |

0.45% |

High Yield Consumer Products |

7.5% |

448 |

4.25 |

-0.39% |

0.15% |

High Yield Food & Beverage |

7.2% |

412 |

4.87 |

0.15% |

-2.14% |

High Yield Supermarkets |

8.7% |

569 |

5.68 |

0.35% |

7.90% |

High Yield Restaurants |

6.2% |

313 |

4.97 |

0.27% |

-0.52% |

Exhibit 113: Macro data sets up for a tougher 2019; comping out of tax reform, as well as housing, rates, stock market all-time highs pose threats

|

105 |

|

104 |

|

103 |

Indexed |

102 |

|

|

|

101 |

|

100 |

|

99 |

Est. disposable income without tax reform Disposable Income

Est. disposable income without tax reform Disposable Income

Source: Goldman Sachs Global Investment Research, Bloomberg Source: Goldman Sachs Global Investment Research, Bloomberg

4 December 2018 |

50 |

vk.com/id446425943

Goldman Sachs

Credit Outlook

Exhibit 114: Earnings outlook tepid into FY19, more possible headwinds than tailwinds

|

|

|

Puts & Takes |

|

|

|

|

|

|

|

|

|

|

|

2018 |

2019 |

|

|

|

• |

Footprint rationalization (+ / - implications, depending on issuer) |

…Unchanged ( + / -) |

|

|

|

• Select outsized growth ( + Madewell, MyTheresa, BBW) |

…Unchanged ( + ) |

|

|

|

Top Line |

• |

Online sales ( + ) |

…Unchanged ( + ) |

|

|

• |

FX Tailwinds ( + ) |

…Possible FX Headwinds ( - ) |

|

|

|

|

|

|||

|

|

• |

Tax Bump / Favorable Macro ( + ) |

…Waning Effect ( - ) |

|

|

|

• |

Traffic Challenges ( - ) |

…Unchanged ( - ) |

|

|

|

• |

Inflationary pressures (distribution / freight) ( - ) |

…Unchanged ( - ) |

|

|

|

• |

Tariffs (no impact) |

…Likely headwind ( - ) |

|

|

|

• |

Promotional cadence ( - ) |

…Unchanged ( - ) |

|

|

Margin |

• |

Higher wages ( - ) |

…Unchanged ( - ) |

|

|

|

• |

Online growth / mix ( - ) |

…Unchanged ( - ) |

|

|

|

• |

Business investments (IT, marketing) ( - ) |

…Unchanged ( - ) |

|

|

|

• |

Misc. non-repeatables (Sourcing benefits, acquisition synergies) ( + ) |

…Waning Effect ( - ) |

|

|

|

|

|

|

|

Source: Goldman Sachs Global Investment Research

Trade Idea #1: Swap out of the Sally Beauty 5.625% ’25 ($96.6;YTW 6.2%) and into

the L Brands 5.25% ’28 ($89.5;YTW 6.8%)

Investors can pick up 60bp and take out 7pts by swapping into a credit with similar leverage (FY19E 3.2x at SBH and 2.9x at LB) and free cash flow prospects (>10% FCF to debt in both cases). Although we generally like the beauty category better than apparel, we think SBH is just beginning to face many secular headwinds, whereas a significant portion of LB’s challenges are, we believe, idiosyncratic and largely due to the company’s own actions. LB, despite its headwinds, has a growing banner (BBW), and a strong brand name in Victoria’s Secret; we think with possible strategic changes (branding, imaging, marketing, product) the company can affect a turnaround, and has the balance sheet to do so. With regard to Sally, we think the slowdown in comps that began in 2017 is a result of secular shifts in the sector, including more competition from mass players in the hair care space, shift to online in the beauty category, and preference for premium products. We believe some initiatives underway with regard to product resets / new introductions, changes to the loyalty program, and others, could create a period of disruption into 2019 and keep us less constructive on the longer-term business outlook.

4 December 2018 |

51 |

vk.com/id446425943

Goldman Sachs

Credit Outlook

Exhibit 115: LB vs. SBH Relative Value

|

500 |

|

|

|

|

|

|

|

|

|

450 |

|

|

|

|

|

|

|

|

|

400 |

|

|

|

|

|

|

|

|

OAS Spread |

350 |

|

|

|

|

|

|

|

|

300 |

|

|

|

|

|

|

|

|

|

250 |

|

|

|

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

150 |

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

50 |

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

|

|

|

|

|

Mar-18 |

Apr-18 |

May-18 |

Jun-18 |

Jul-18 |

Aug-18 |

Sep-18 |

Oct-18 |

Nov-18 |

|

|

|

|

LB 5.25 2/1/2028 |

SBH 5.625 12/1/2025 |

|

|

||

Source: Goldman Sachs Global Investment Research, Bloomberg

Trade Idea #2: Swap out of Rite Aid 6.125% ‘23 ($87;YTW 9.9%) and into the J.C.

Penney 1L ‘23 ($83;YTW 10.6%)

An unlikely comparison to some, but we think there are many similarities between RAD and JCP that make these two bonds highly comparable. With similar leverage metrics (>6.0x) and free cash flow generation (modestly negative in FY18E and modestly positive in FY19E for both), the balance sheets are the first point of comparison. Further, both operate in secularly challenged industries where they are smaller names amongst their peers, and struggle with gaining scale and justifying a “need to exist”. Most investors, we believe (ourselves included) value both businesses on a sum-of-the-parts basis (SOTP), but we think it is most appropriate to put weight on this approach if (1) assets are easily severable, (2) there are real, willing buyers available, and (3) the notes are secured. In the case of RAD, assets might be severable, but we struggle to find currently willing buyers, and the notes are unsecured and likely to have secured debt put ahead of them at some point in the future. The JCP notes are secured by real assets (namely real estate), on which we estimate fairly high recovery. Further, we think the JCP structure stands to benefit from more potential near-term catalysts, including (1) favorable guidance / sentiment created by the newly appointed CEO, (2) incremental asset sales to shore up liquidity, and (3) better earnings into 2019 with healthier inventory levels. RAD, on the other hand, we believe faces more downside catalysts from an earnings standpoint, including the potential rolloff of the WBA agreement and uncertainty around the extension of its contract with McKesson that matures in 2020. For these reasons, we prefer the JCP 1st lien notes to the RAD Sr. Notes for similar dollar price, maturity, and yield, and think spreads should widen between the two.

4 December 2018 |

52 |

vk.com/id446425943

Goldman Sachs

Credit Outlook

Exhibit 116: JCP vs. RAD Relative Value

|

900 |

|

|

|

|

|

|

|

|

|

|

|

800 |

|

|

|

|

|

|

|

|

|

|

|

700 |

|

|

|

|

|

|

|

|

|

|

|

600 |

|

|

|

|

|

|

|

|

|

|

OAS Spread |

500 |

|

|

|

|

|

|

|

|

|

|

400 |

|

|

|

|

|

|

|

|

|

|

|

300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

|

Nov-17 |

Dec-17 |

Jan-18 |

Feb-18 |

Mar-18 Apr-18 |

May-18 Jun-18 |

Jul-18 |

Aug-18 |

Sep-18 |

Oct-18 |

Nov-18 |

|

|

|

|

|

JCP 5.875 7/1/2023 |

RAD 6.125 4/1/2023 |

|

|

|

|

|

Source: Goldman Sachs Global Investment Research, Bloomberg

Risks to our view:

nLB (Outperform): EBITDA/gross margin declines beyond expectations, shareholder friendly actions, inability to enact VS or PINK turnarounds

nSBH (Underperform): Greater-than-expected cost reductions, additional tailwinds from product launches

nRAD (Underperform): Takeover/M&A activity, renewed focus on core business, gross margin expansion

nJCP (In-Line): EBITDA recovery, greater-than-expected share gains from Sears closures on the upside; vendor tightening, lack of real estate monetization on the downside

4 December 2018 |

53 |