DB European Building Construction 2019 Outlook_watermark

.pdfvk.com/id446425943

Deutsche |

Another year of significant EBITDA margin consensus cut in 2018 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

Bank |

|

■ |

|

|

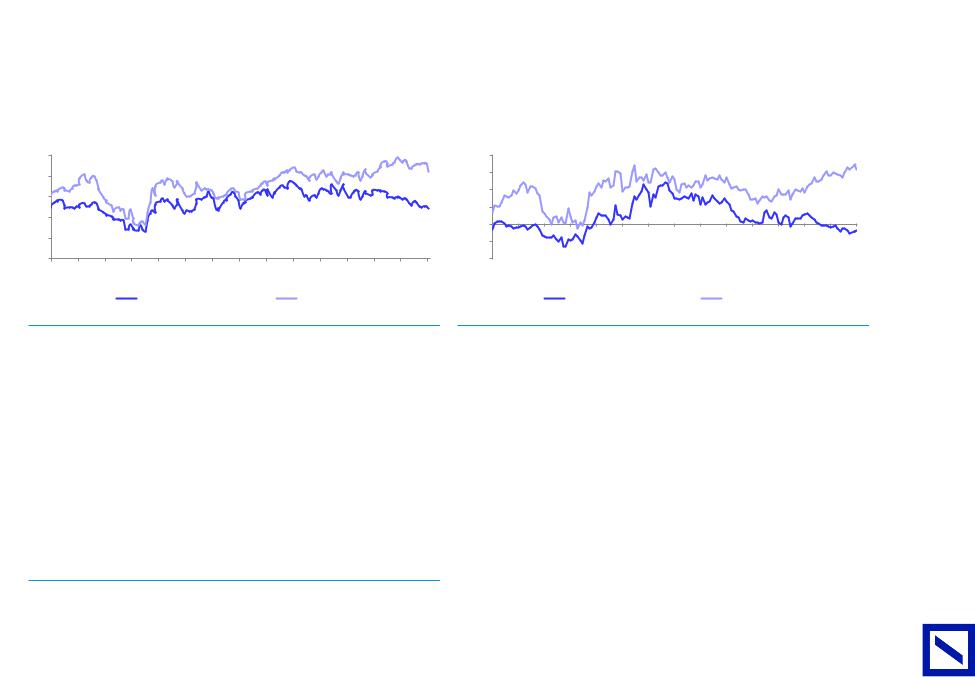

FY 18 EBITDA consensus downgrades for cyclical stocks have mainly been driven by margins rather than top-line cuts. |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

■ |

|

|

We believe in particular that the reinflation of coal / oil in Q2 18 after the DM price increase implementation has been particularly detrimental for |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

AG/London |

|

|

|

|

|

cement stocks as a second round of price increase has been very di cult to implement. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||

Figure 70: Consensus margin evolution by sub-sector |

|

|

|

|

|

|

|

|

|

Figure 71: Newcastle Coal evolution vs. future price at end of 2017 |

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

■ |

|

|

We believe energy price inflation above expectations has caused c50% of Heidelberg EBITDA consensus downgrades in 2018E. |

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

130 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

19.5% |

19.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18.9% |

120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

19.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

18.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

18.0% |

|

|

17.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

90 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

17.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

17.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

70 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

16.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

16.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Jan-17 |

Feb-17 |

Mar-17 |

Apr-17 |

May-17 |

Jun-17 |

Jul-17 |

Aug-17 |

Sep-17 |

Oct-17 |

Nov-17 |

Dec-17 |

Jan-18 |

Feb-18 |

Mar-18 |

Apr-18 |

May-18 |

Jun-18 |

Jul-18 |

Aug-18 |

Sep-18 |

Oct-18 |

Nov-18 |

||||||||||

|

Jan-18 |

Jan-18 |

|

Jan-18 |

Feb-18 |

Feb-18 |

Mar-18 |

Mar-18 |

Apr-18 |

Apr-18 |

May-18 |

May-18 |

Jun-18 |

Jun-18 |

Jul-18 |

Jul-18 |

Jul-18 |

Aug-18 |

Aug-18 |

Sep-18 |

Sep-18 |

Oct-18 |

Oct-18 |

Nov-18 |

|

|

|

|||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

Average - Cyclical stocks |

|

|

|

|

|

Average - Structural stocks |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Newcastle spot price |

|

|

|

|

Newcastle future price as of Nov 17 |

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Source: Deutsche Bank, Bloomberg Finance LP. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank, Factset, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

Figure 72: Oil price evolution vs. forecasts end of 2017 |

|

|

|

|

|

|

|

|

|

Figure 73: Reconciliation Heidelberg EBITDA consensus evolution YTD |

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

85 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,700 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,600 |

|

|

3,569 |

|

|

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

75 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,500 |

|

|

|

|

|

|

|

|

|

|

160 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

70 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,400 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

65 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

90 |

|

|

|

|

|

|

|

|

|

||||

|

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

55 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c10% energy cost |

|

|

|

|

|

|

|

|

51 |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,088 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,100 |

|

|

|

|

|

|

|

|

inflation for FY 18E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

45 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,900 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

17-Jan |

17-Feb |

17-Mar |

17-Apr |

17-May |

17-Jun |

17-Jul |

17-Aug |

17-Sep |

17-Oct |

17-Nov |

17-Dec |

18-Jan |

18-Feb |

18-Mar |

18-Apr |

18-May |

18-Jun |

18-Jul |

18-Aug |

18-Sep |

18-Oct |

18-Nov |

2,800 |

|

|

|

|

|

|

|

|

|

|

|

|

quarry sales |

(mainly |

|

|

|

|

|

2018 |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Start of year |

|

FX |

|

Energy costs |

|

Gains on |

|

Q1 miss |

|

Others |

|

As of Nov |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Crude oil price ($/bbl) |

|

|

|

|

|

DB forecasts as of Jan 18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

weather) |

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Source: Deutsche Bank, Factset, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

31 Page

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

32 Page |

EBITDA margin consensus cuts since start of year |

|

|

|

|

|

|

|

||||||||

■ |

|

Cement companies and Tarkett have seen the highest EBITDA margins downgrade due to a high inflation environment coupled with a limited ability |

||||||||||||||

|

|

|

|

to adjust price over the course of the year. |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||||||

|

Figure 74: Cyclical stocks have had lower pricing power vs. structural growth stocks in 2018 |

|

|

|

|

|||||||||||

|

|

|

|

Cemex |

Heidelberg |

Tarkett |

Buzzi |

Titan |

LafargeHolcim |

Saint Gobain |

Sika |

Geberit |

CRH |

Kingspan |

||

|

0.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-0.3% |

|

|

|

|

-0.5% |

|

|

|

|

|

|

|

|

|

|

-0.3% |

-0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-0.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-0.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-1.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-1.1% |

|

|

|

|

|

|

|

|

-1.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-1.6% |

|

|

|

|

|

|

|

|

|

-2.0% |

|

|

|

|

-1.9% |

-1.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

-2.5% |

|

|

-2.3% |

-2.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Source:Deutsche Bank estimates, Company data |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AG/London Bank Deutsche

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Deutsche |

Costs to follow di erentiated patterns in 2019 |

|

|

|||

|

|

|

||||

|

■ |

Heavyside stocks (exposure to Electricity in Europe and US / International coal) should continue to see a high inflation environment in H1 19 (around |

||||

Bank |

|

c10% energy cost inflation forecasted) before a moderation in H2 19. |

|

|

||

■ |

Lightside products (mostly oil derivatives, limited energy cost exposure) should also see a continuation of cost inflation until at least Q1 19 (four to |

|||||

AG/London |

||||||

|

six months lag between oil price and oil derivatives prices evolution). |

|

|

|||

|

|

|

|

|||

|

■ |

The low levels of the Rhine river in Germany could also cause some supply disruption and switch to more expensive alternative suppliers. |

||||

|

|

|

|

|

||

|

Figure 75: Electricity prices in Europe (2018 = 100) |

Figure 76: Coal & Natural gas price evolution (2018 = 100) |

||||

150 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

150 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

140 |

|

|

|

|

|

|

|

|

|

135 |

|

140 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

130 |

|

|

|

|

|

|

|

|

|

|

|

130 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

120 |

|

|

|

|

|

|

|

|

|

116 |

|

120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

94 |

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

90 |

|

|

|

|

|

|

|

|

|

|

|

90 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

93 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

80 |

|

|

|

|

|

|

|

|

|

||

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

70 |

|

|

|

|

|

|

|

|

|

|

|

70 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

60 |

|

|

|

|

|

|

|

|

|

|

|

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Feb-18 |

Mar-18 |

Apr-18 |

May-18 |

|

Jul-18 |

Aug-18 |

Sep-18 |

Oct-18 |

Nov-18 |

|

|

Jan-18 |

|

|

|

|

|

|

|

|

Jun-18 |

Jun-18 |

Jul-18 |

Jul-18 |

Jul-18 |

|

|

|

|

|

|

|

Jan-18 |

Jun-18 |

||||||||||

Jan-18 |

Jan-18 |

Feb-18 |

Feb-18 |

Mar-18 |

Mar-18 |

Apr-18 |

Apr-18 |

May-18 |

May-18 |

Aug-18 |

Aug-18 |

Sep-18 |

Sep-18 |

Oct-18 |

Oct-18 |

Nov-18 |

|||||||||||||||||

|

France |

|

Italy |

|

Belgium |

|

|

Germany |

|

|

Poland |

|

Nordics |

|

|

UK |

|

Newcastle Coal |

|

|

|

|

Rotterdam Coal |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

Natural Gas (US) |

|

|

|

|

Central Appalachian coal |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Source: Deutsche Bank, Factset, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank, Factset, Bloomberg Finance LP. Nov 2018 index as of 26 Nov closing. |

|

|

|

|||||||||||||||

Figure 77: Oil and oil derivate product prices (2018 = 100)

120 |

|

|

|

|

|

|

|

|

|

|

115 |

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

105 |

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

98 |

|

|

|

|

|

|

|

|

|

|

|

95 |

|

|

|

|

|

|

|

|

|

94 |

90 |

|

|

|

|

|

|

|

|

|

90 |

85 |

|

|

|

|

|

|

|

|

|

86 |

80 |

|

|

|

|

|

|

|

|

|

83 |

75 |

|

|

|

|

|

|

|

|

|

|

70 |

|

|

Apr-18 |

May-18 |

|

|

Aug-18 |

Sep-18 |

Oct-18 |

Nov-18 |

Jan-18 |

Feb-18 |

Mar-18 |

Jun-18 |

Jul-18 |

||||||

|

Brent Crude |

|

|

|

|

|

Naphta |

|

|

|

|

Polyethytlene linear low density |

|

|

MDI W Europe |

|

|

||||

Polystyrene General purpose

Source: Deutsche Bank, Factset, Bloomberg Finance LP. Nov 2018 index as of 26 Nov closing.

33 Page

Figure 78: Miscellaneous commodities' prices (2018 = 100)

115 |

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

|

|

105 |

|

|

|

|

|

|

|

|

|

|

|

102 |

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

98 |

95 |

|

|

|

|

|

|

|

|

|

|

|

94 |

|

|

|

|

|

|

|

|

|

|

|

|

|

90 |

|

|

|

|

|

|

|

|

|

|

|

|

85 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Jan-18 Feb-18 |

Mar-18 |

Apr-18 May-18 Jun-18 |

Jul-18 Aug-18 |

Sep-18 Oct-18 |

|||||||

|

|

|

||||||||||

|

|

|

|

Paper |

|

|

Steel |

|

|

Polyurethane |

PVC |

Cast iron |

|

|

|

|

|

|

|

||||||

Source: Deutsche Bank, Factset, Bloomberg Finance LP

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

34 Page |

Negative cement price vs. cost in H2 18 does not bode well for H1 19. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

■ |

We expect price vs. cost to remain in general negative in H1 19E: energy costs inflation should remain at an elevated level while most prices increases |

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

in DM should be implemented only in April with full impact to be seen only in Q3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

■ |

Among cement stocks, we believe Buzzi (thanks to Germany, Italy and Poland) should be the only one with a positive price vs. cost in H2 18E. |

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

Figure 79: Price vs. cost in negative territories for cement stocks since |

|

Figure 80: Energy cost inflation should remain high at least until Q2 19 |

||||||||||||||||||||||||||||||||||||||||||||||||||

|

H1 17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(example of Heidelberg) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

130 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14% |

|

||

|

3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

125 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12% |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10% |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

115 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8% |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

110 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

105 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6% |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

-1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy cost inflation |

|

|

|

4% |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy cost inflation |

|

|

|

|

|

|||||

|

-2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

95 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

should remain high |

|

|

|

2% |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

should remain high |

|

|

|

|

||||||

|

-3% |

|

|

|

|

|

H2 16 |

|

|

|

H1 17 |

|

|

|

H2 17 |

|

|

|

H1 18 |

|

H2 18E |

90 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0% |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q1 16 |

Q2 16 |

Q3 16 |

Q4 16 |

Q1 17 |

Q2 17 |

Q3 17 |

Q4 17 |

Q1 18 |

Q2 18 |

|

Q3 18 |

Q4 18E |

Q1 19E |

Q2 19E |

Q3 19E |

Q4 19E |

|||||||||||||||||

|

|

|

|

|

|

|

Buzzi |

|

|

|

Cemex |

|

|

|

CRH |

|

|

|

Heidelberg |

|

LafargeHolcim |

|

|

|

|

|

|

|

YoY increase (rhs,%) |

|

|

|

|

|

|

Energy cost Index HEI (lhs) |

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

Source: Deutsche Bank, Company data, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

Source: Deutsche Bank, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AG/London Bank Deutsche

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Deutsche |

LafargeHolcim to benefit from self-help in 2019. |

|

|

||||||

|

|

|

|||||||

Bank |

■ |

Reflecting disappointing results in 2017-18, most ‘cyclical growth’ companies have announced new costs savings program. |

|||||||

■ |

We believe the impact should be visible in 2019 mostly for LafargeHolcim (we estimate a positive impact of CHF250m in 2019 of SG&A savings, eg |

||||||||

|

|||||||||

AG/London |

|

4% of FY 19E EBITDA). This does not take into account potential savings from potential downstream businesses margins improvement. |

|||||||

■ |

Between synergies and business improvement measures, CRH has the most ambitious cost savings program over the 2019-21 period. However the |

||||||||

|

|||||||||

|

|

benefits are expected to be back end-loaded with only E40m of synergies expected in 2019 (c1% of Group EBITDA). |

|||||||

|

|

|

|

||||||

|

Figure 81: LafargeHolcim should benefit from self help the most |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Total cost |

|

Assumed |

% FY 19E |

|

|

|

|

Company |

Timescale |

impact in |

Comments |

|

||||

|

cutting target |

EBITDA |

|

||||||

|

|

|

|

2019E |

|

|

|||

|

|

|

|

|

|

|

|

||

|

|

Buzzi |

N/A |

N/A |

N/A |

N/A |

Synergies in newly German asset could bring E5-10m of fixed costs savings (c1.5% FY 19E EBITDA) |

|

|

|

|

Cemex |

$150m |

2019-20 |

$75m |

2.8% |

Stronger Cemex plan announced in Q2 18 focused on SG&A, process and procurement |

|

|

|

|

CRH |

E450m |

2019-21 |

E40m |

1.1% |

Synergies (E130m) + Business improvement (E325m) however benefits to be back-end loaded |

|

|

|

Heidelberg |

E100m |

2019-20 |

E30m |

1.0% |

SG&A savings target announced after profit warning in Q3 |

|

||

|

LafargeHolcim |

CHF400m |

2018-20 |

CHF250m |

4.2% |

SG&A savings from corp. closures as well as countries / regions |

|

||

|

|

Titan |

N/A |

N/A |

N/A |

N/A |

N/A |

|

|

|

|

Sika |

N/A |

N/A |

N/A |

N/A |

No specific cost cutting besides synergies and margin improvement from recently acquired companies |

|

|

|

|

Geberit |

N/A |

N/A |

N/A |

N/A |

N/A |

|

|

|

|

Tarkett |

N/A |

N/A |

N/A |

N/A |

No specific plan - but on an ongoing basis the company intends to improve productivity by cE40m per year |

|

|

|

Saint Gobain |

E250m |

2019-21 |

E50m |

1.5% |

E250m of additional savings announced on Nov 26 2018 on top of ongoing fixed costs savings program |

|

||

|

Kingspan |

N/A |

N/A |

N/A |

N/A |

No specific cost cutting besides synergies and margin improvement from recently acquired companies |

|

||

|

Source: Deutsche Bank estimates, Company data |

|

|

|

|

|

|||

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

35 Page

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Page |

At spot price, FX to be a tailwind on EURO stocks |

36 |

|

■Reflecting the USD appreciation vs. EUR, we calculate at spot price a positive FX translation impact on 2019E Sales for all EURO reporting stocks.

■We estimate at spot price a negative FX translation impact in 2019 for stocks reporting in CHF or USD. (more so for Cemex, penalized by the c6% Mexican Peso depreciation vs. USD ).

■Key LafargeHolcim EM currencies are holding so far well - Mexico and Argentina are two notable exceptions, however in markets where the local industry has historically been able to compensate currencies depreciation by local price increase.

Figure 82: FX impact on Sales based on geographic footprints |

|

|

|

Figure 83: Key currency rates and expected movements |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FY 18E |

FY 19E |

Exp. YoY movement |

|

2.9% |

|

|

|

|

|

|

|

|

|

|

|

|

EUR --> USD |

1.181 |

1.134 |

4.1% |

|

|

3% |

|

2.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.8% |

|

|

|

|

|

|

|

|

|

|

EUR --> GBP |

0.884 |

0.884 |

-0.1% |

|

|

2% |

|

|

1.3% |

1.3% |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

1.0% |

|

|

|

|

|

|

|

CHF --> USD |

1.022 |

1.001 |

2.1% |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

1% |

|

|

|

|

|

|

0.3% |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

CHF --> EUR |

0.866 |

0.883 |

-1.9% |

|

||

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

CHF --> Nigerian Naira |

369.48 |

364.67 |

1.3% |

|

|

-1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

CHF --> Indian Rupee |

69.84 |

70.90 |

-1.5% |

|

|

-2% |

|

|

|

|

|

|

|

-0.9% |

-1.3% |

-1.5% |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

EUR --> Indonesia Rupee |

16776.9 |

16413.9 |

2.2% |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

-3% |

|

|

|

|

|

|

|

|

|

|

-2.9% |

|

|

USD --> MXN Peso |

19.28 |

20.52 |

-6.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

-4% |

Titan |

CRH |

Tarkett |

Buzzi |

Heidelberg |

Kingspan |

Saint Gobain |

LafargeHolcim |

Sika |

Geberit |

Cemex |

|

|

|

|

|

||

|

|

|

|

|

|

|||||||||||||

Source: Deutsche Bank estimates, Factset |

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank estimates, Factset. Note: FY19E assumed to same as that of 26 Nov closing. |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AG/London Bank Deutsche

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Deutsche |

DB forecasts vs. consensus |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Bank |

■ |

Our 2019E EBITDA forecasts are on average c1% below consensus. |

|

|

|

|

|

|

|

|||

AG/London |

■ |

Our FY 19E EBITDA forecasts for LafargeHolcim are 0.8% above the Street. We believe however that consensus has yet to reflect Holcim Indonesia |

||||||||||

|

■ |

This is especially the case for Geberit (more cautious view on organic sales growth and impact of the recent CHF appreciation vs. EUR) but also on |

||||||||||

|

|

Cemex (Mexican Peso depreciation vs. USD) and Tarkett (more cautious view taken on margins in H1 19). |

|

|

|

|

||||||

|

|

divestment (cCHF110m EBITDA impact) - this would place our forecasts c2.5-3% above consensus for FY 19E. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Figure 84: DB estimates vs. consensus |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

DB estimates |

|

Consensus |

|

DBe vs. consensus |

|

||

|

Company |

|

Key operating metric |

2019E |

2020E |

2019E |

2020E |

|

2019E |

2020E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Buzzi Unicem |

Recurring EBITDA |

617 |

667 |

614 |

655 |

|

0.6% |

1.8% |

|

|

|

|

Cemex |

|

EBITDA |

2,720 |

2,935 |

2,765 |

2,950 |

|

-1.6% |

-0.5% |

|

|

|

CRH |

|

EBITDA |

3,761 |

4,203 |

3,778 |

4,058 |

|

-0.5% |

3.6% |

|

|

|

Geberit |

|

EBITDA |

885 |

914 |

917 |

961 |

|

-3.5% |

-4.9% |

|

|

|

HeidelbergCement |

EBITDA |

3,218 |

3,433 |

3,231 |

3,407 |

|

-0.4% |

0.8% |

|

|

|

|

Kingspan |

|

EBITA |

496 |

535 |

498 |

543 |

|

-0.4% |

-1.5% |

|

|

|

LafargeHolcim |

Recurring EBITDA |

6,391 |

6,793 |

6,338 |

6,698 |

|

0.8% |

1.4% |

|

|

|

|

Saint Gobain |

EBIT |

3,353 |

3,604 |

3,394 |

3,638 |

|

-1.2% |

-0.9% |

|

|

|

|

Sika |

|

EBIT |

1,145 |

1,263 |

1,150 |

1,285 |

|

-0.4% |

-1.7% |

|

|

|

Tarkett |

|

EBITDA |

295 |

317 |

307 |

337 |

|

-3.8% |

-5.7% |

|

|

|

Titan Cement |

EBITDA |

299 |

332 |

295 |

317 |

|

1.3% |

4.9% |

|

|

|

|

Average |

|

|

|

|

|

|

|

-0.8% |

-0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank estimates, Factset. Note: Factset estimates as of 28 Nov.

37 Page

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Page |

Valuation - Sector trades well below mid-cycle |

38 |

|

■After 2018 de-rating, the sector now trades at 13.7x 2019E P/E (vs. 14.9x for mid-cycle level) and 9.0x 2019E EV/EBITDA.

■This hides however a clear skew between ‘cyclical stocks’ (heavyside, Saint Gobain & Tarkett - 11.3x 2019E P/E & 6.8x 2019E EV/EBITDA) and the ‘structural growth stocks’ (Sika, Geberit & Kingspan - 20.4x 2019E P/E & 14.7x 2019E EV/EBITDA).

■Cyclical stocks clealry o er value with 2019E P/E well below mid-cycle levels for most companies. This is especially true for Saint Gobain (2019E P/ E only 19% above the historical trough level seen in 2009).

■Our analysis of Saint Gobain 12m forward P/E vs. European PMI also shows value in the stock. While historically Saint Gobain 12m forward P/E has been very well correlated to the European PMI, we note a clear disconnection between both metrics since mid of 2017 with the current stock's 12m forward P/E more consistent with an European PMI level below 45 (eg a clear recession scenario).

■For structural growth stocks, after YTD strong performance, Kingspan valuation discount vs. other structural growth stocks has faded and is now back to pre-Brexit levels. As such, we believe the stock could be now more vulnerable to any negative news regarding the UK market.

Figure 85: Valuation - European Building & Construction stocks

Company |

Reuters |

Current |

DB |

Upside / |

DB |

Market |

EV/EBITDA (x) |

P/E (x) |

|

FCF Yield |

Dividend Yield |

Net debt / EBITDA (x) |

||||

|

Code |

Price |

Target Price |

downside |

Rating |

Cap (E m) |

2019E |

2020E |

2019E |

2020E |

2019E |

2020E |

2019E |

2020E |

2019E |

2020E |

Cyclical avg. |

|

|

|

17.0% |

|

|

6.8 |

6.0 |

11.3 |

9.5 |

8.6% |

10.5% |

3.4% |

3.8% |

2.0 |

1.6 |

Buzzi Unicem |

BZU.MI |

16.8 |

21.0 |

25.0% |

Buy |

3,453 |

5.1 |

4.1 |

11.8 |

10.0 |

10.1% |

11.2% |

1.2% |

1.6% |

1.2 |

0.6 |

Cemex |

CX.N |

4.9 |

6.0 |

22.0% |

Buy |

6,381 |

6.9 |

6.0 |

10.8 |

7.7 |

13.4% |

17.6% |

na |

na |

3.3 |

2.6 |

CRH |

CRH.I |

24.3 |

28.0 |

15.2% |

Hold |

19,685 |

7.1 |

6.0 |

11.6 |

9.8 |

7.3% |

8.7% |

3.2% |

3.8% |

1.6 |

1.1 |

HeidelbergCement |

HEIG.DE |

59.4 |

72.0 |

21.2% |

Hold |

11,786 |

7.3 |

6.5 |

9.1 |

7.9 |

9.9% |

11.9% |

4.4% |

5.1% |

2.3 |

1.9 |

LafargeHolcim |

LHN.S |

44.8 |

54.0 |

20.5% |

Buy |

23,753 |

7.3 |

6.7 |

11.8 |

10.4 |

7.0% |

8.7% |

4.5% |

4.6% |

2.0 |

1.7 |

Saint Gobain |

SGOB.PA |

32.9 |

43.0 |

30.6% |

Buy |

18,127 |

5.8 |

5.3 |

8.9 |

8.0 |

8.5% |

9.5% |

4.5% |

5.0% |

1.5 |

1.2 |

Tarkett |

TKTT.PA |

21.7 |

20.5 |

-5.4% |

Hold |

1,372 |

7.4 |

6.8 |

13.4 |

11.8 |

5.8% |

6.9% |

3.0% |

3.4% |

2.3 |

1.9 |

Titan Cement |

TTNr.AT |

19.6 |

21.0 |

7.4% |

Hold |

1,582 |

7.7 |

6.5 |

12.9 |

10.6 |

7.1% |

9.2% |

2.8% |

2.8% |

2.1 |

1.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Structural growth avg. |

|

|

|

21.0% |

|

|

14.7 |

13.5 |

20.4 |

18.9 |

4.6% |

5.1% |

2.1% |

2.3% |

0.8 |

0.5 |

Geberit |

GEBN.S |

385.1 |

430.0 |

11.7% |

Hold |

12,324 |

16.8 |

16.1 |

22.3 |

21.4 |

4.3% |

4.4% |

2.9% |

3.0% |

0.5 |

0.5 |

Kingspan |

KSP.I |

37.7 |

45.0 |

19.4% |

Hold |

6,743 |

13.3 |

11.9 |

18.1 |

16.7 |

4.9% |

5.7% |

1.3% |

1.4% |

0.9 |

0.3 |

Sika |

SIKA.S |

121.3 |

160.0 |

31.9% |

Buy |

15,109 |

13.9 |

12.3 |

20.7 |

18.6 |

4.6% |

5.1% |

2.1% |

2.3% |

1.1 |

0.6 |

Sector average |

|

|

|

18.1% |

|

|

9.0 |

8.0 |

13.7 |

12.1 |

7.5% |

9.0% |

3.0% |

3.3% |

1.7 |

1.3 |

Source: Deutsche Bank estimates, Reuters. Note: Valuation and Current price as of closing of 28 Nov 2018.

AG/London Bank Deutsche

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Deutsche |

Cyclical stocks have de-rated since start of year |

|

|

|

||

|

|

|

|

|||

Bank |

■ |

Cyclical stocks have clearly de-rated in 2018 and trade for the first time since mid 2009 below average STOXX 600 P/E. |

||||

■ |