DB European Building Construction 2019 Outlook_watermark

.pdfvk.com/id446425943

Deutsche |

The US: Robust growth in 2019 but housing risks are mounting |

|

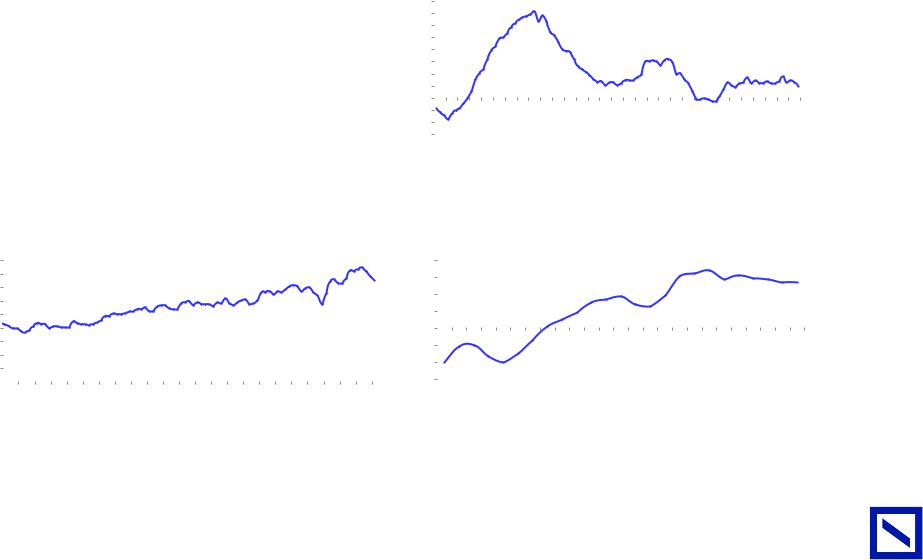

US construction still below mid-cycle level |

||

Bank |

■ |

Mainly driven by the residential segment which is still 20% below mid-cycle level and more than 40% below peak levels, US construction market |

|

||

AG/London |

|

is below the long-term average. |

|

Titan Cement has the highest upside potential to mid-cycle due to its Florida exposure while Buzzi is the closest to mid-cycle (however still below) |

|

|

■ |

When taking into account the population growth, we believe 2018 cement demand is c15% below mid-cycle level. |

|

■ |

|

|

|

due to Texas. |

Figure 11: US cement demand vs. population evolution |

|

|

|

|

|

|

|

Figure 12: US cement demand per capita evolution |

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

140 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

323 |

|

350 |

450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

400 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

94.3 |

250 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

378 |

|

Long-term average: |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

200 |

350 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

328 kg / inh. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

150 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

292 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

299 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

281 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

50 |

250 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

|

|

|

|

233 |

|

|

|

|

|

|

|

|

|

|

|

|

|

228 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1965 |

1967 |

1969 |

1971 |

1973 |

1975 |

1977 |

1979 |

1981 |

1983 |

1985 |

1987 |

1989 |

1991 |

1993 |

1995 |

1997 |

1999 |

2001 |

2003 |

2005 |

2007 |

2009 |

2011 |

2013 |

2015 |

2017 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1965 |

1967 |

1969 |

1971 |

1973 |

1975 |

1977 |

1979 |

1981 |

1983 |

1985 |

1987 |

1989 |

1991 |

1993 |

1995 |

1997 |

1999 |

2001 |

2003 |

2005 |

2007 |

2009 |

2011 |

2013 |

2015 |

2017 |

|||||||||||||||||||||||||||

|

|

|

|

US cement demand (lhs) |

US Population (rhs) |

|

|

|

|

|

US cement demand per cap |

1965-2017 average |

|

|

|

|

|

|

|

|

|||||

Source: Deutsche Bank, US Census, US PCA |

|

Source: Deutsche Bank, US Census, US PCA |

|

|||||||||

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Figure 13: US housing starts (SAAR '000) |

|

Figure 14: Demand evolution per capita on companies' footprint |

|

|

|

2,500 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2018 vs 1965- |

2018 vs. |

Peak vs. 2018 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2018 average |

trough |

||

2,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Long term avg - |

|

Buzzi |

-8% |

32% |

37% |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1,433 |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1,500 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cemex |

-16% |

41% |

63% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1203 |

|

CRH (Heavyside) |

-15% |

21% |

46% |

|

|

500 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heidelberg |

-13% |

27% |

45% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LafargeHolcim |

-14% |

22% |

45% |

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Titan |

-21% |

46% |

94% |

|

1965 |

1967 |

1969 |

1971 |

1973 |

1975 |

1977 |

1979 |

1981 |

1983 |

1985 |

1987 |

1989 |

1991 |

1993 |

1995 |

1997 |

1999 |

2001 |

2003 |

2005 |

2007 |

2009 |

2011 |

2013 |

2015 |

2017 |

|

|

|

||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

Source: Deutsche Bank, US Census |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source:Deutsche Bank estimates, Company data |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 Page

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

12Page |

|

The US growth should show no sign of moderation in 2019 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

■ |

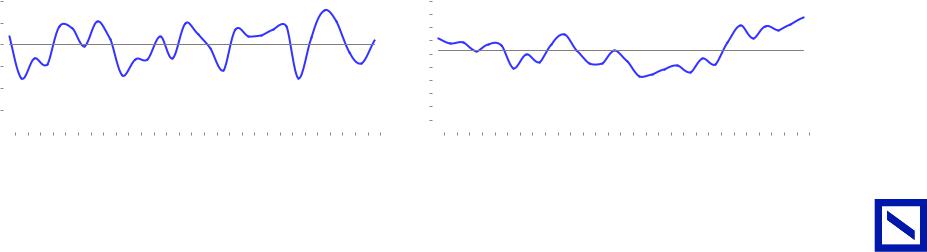

All leading indicators point at a continued cement demand growth in 2019: building permits are up 6% YoY YTD, Dodge Momentum Index on non |

||||||||||||||||||||||||||

|

|

|

|

|

residential buildings is also up c15-20% YoY while 12m trailing highways awards are up 14% in Sept 18. |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

■ |

PCA (the reference for cement consultants in the US) shares this optimism for 2019E, with cement demand growth forecasts of 2.6%. |

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

Figure 15: PCA US cement forecasts for 2019E - 20E |

|

|

|

|

Figure 16: YoY change in 9m trailing US building permits |

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

40% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FALL 2018 |

2017 |

2018E |

2019E |

2020E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

35% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RESIDENTIAL |

6.8% |

3.8% |

3.1% |

1.7% |

|

30% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

25% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NON-RESI |

8.7% |

1.7% |

2.9% |

2.4% |

|

20% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

INFRASTRUCTURE |

-2.0% |

2.8% |

2.2% |

1.2% |

|

15% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5% |

|

||

|

|

TOTAL |

|

2.4% |

2.9% |

2.6% |

1.6% |

|

5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-15% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 |

Oct-12 |

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 |

Apr-14 Jul-14 Oct-14 |

Jan-15 |

Apr-15 |

Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 |

Jan-17 |

Apr-17 Jul-17 |

Oct-17 |

Jan-18 |

Apr-18 |

Jul-18 Oct-18 |

||||

|

|

Source: Deutsche Bank, US PCA |

|

|

|

|

|

|

Source: Deutsche Bank, Factset |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

Figure 17: Dodge Momentum Index (Commercial + Institutional |

|

|

|

Figure 18: YoY change in 12m trailing highway awards |

|

|

|

|

|

|

|

|

||||||||||||||

|

|

Building) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

180 |

|

|

|

|

|

|

|

|

|

20% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

160 |

|

|

|

|

|

|

|

|

|

15% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

140 |

|

|

|

|

|

|

150.5 |

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

14% |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

100 |

|

|

|

|

|

|

|

|

|

5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

80 |

|

|

|

|

|

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

60 |

|

|

|

|

|

|

|

|

|

-5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

-10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

0 |

|

|

|

|

|

|

|

|

|

-15% |

|

Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 |

Feb-17 |

Mar-17 Apr-17 May-17 Jun-17 |

Jul-17 Aug-17 |

Sep-17 |

Oct-17 |

Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 |

Apr-18 |

May-18 |

Jun-18 |

Jul-18 |

Aug-18 |

Sep-18 |

|||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

JUN-11 OCT-11 FEB-12 JUN-12 OCT-12 FEB-13 JUN-13 OCT-13 |

FEB-14 JUN-14 OCT-14 FEB-15 |

|

OCT-16 FEB-17 JUN-17 OCT-17 FEB-18 |

JUN-18 OCT-18 |

|

||||||||||||||||||||

|

|

|

FEB-11 |

JUN-15 OCT-15 FEB-16 JUN-16 |

|

|

||||||||||||||||||||||

AG/LondonBankDeutsche |

|

Source: Deutsche Bank, Dodge Data & Analytics |

|

|

|

|

|

|

Source: Deutsche Bank, US DoT, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Deutsche |

2019 Growth in the US should remain dictated by the footprint |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

Bank |

|

■ |

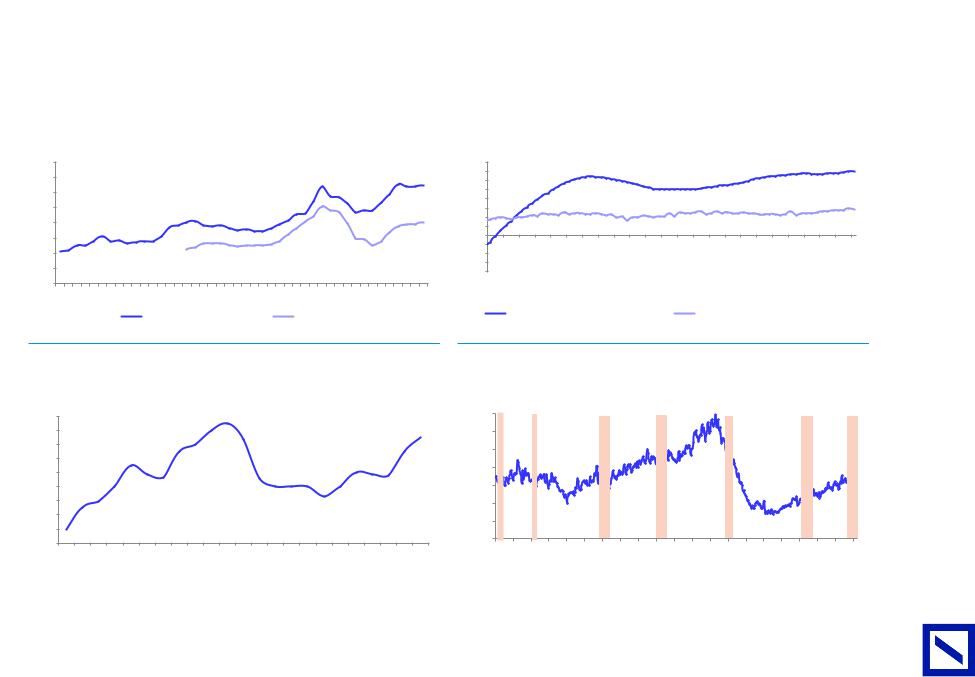

With US regions at di erent stages of the recovery, we believe cement demand growth will remain dictated by the footprint. |

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

■ |

We see above average demand growth on Cemex and Titan (driven by the residential but also strong infrastructure). |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

AG/London |

|

■ |

State by state building permits and highways awards analysis suggest CRH and LafargeHolcim could see demand growth below country average. |

||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12% |

|

10.7% |

|

|

|

|

|

|

|

|

|

|

30% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Figure 19: YoY % YTD US building permits on companies’ US footprints |

|

Figure 20: YoY change in trailing 12m highway awards dollars |

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

9.9% |

|

|

|

|

|

|

|

|

25% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22% |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

20% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

8% |

|

|

|

|

6.5% |

|

|

|

|

|

|

|

15% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

5.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

6% |

|

|

|

|

|

|

|

|

|

|

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

4.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5% |

|

|||

|

4% |

|

|

|

|

|

|

|

|

2.7% |

|

|

|

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

2.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

2% |

|

|

|

|

|

|

|

|

|

|

|

|

-5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0% |

|

CementTitan |

Cemex |

USAverage |

Heidelberg |

CRH |

UnicemBuzzi |

LafargeHolcim |

|

|

-15% |

|

16-Sep |

16-Oct 16-Nov 16-Dec |

Jan-17 AllFeb-17otherMar-17 |

marketsApr-17 May-17 |

17-Jul 17-Aug |

17-Sep 17-Oct 17-Nov |

17-Dec |

|

VulcanFeb-18 |

marketsApr-18 |

18-Jun |

18-Jul |

18-Aug |

18-Sep |

||||||||||

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

-20% |

|

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Jun-17 |

|

|

|

Jan-18 |

Mar-18 |

May-18 |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Source: Deutsche Bank estimates, Company data |

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank, US DoT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

Figure 21: ABI Index by region and regional exposure by company |

|

|

|

Figure 22: Overlap with key Vulcan states by company |

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

ABI Index |

Buzzi |

|

Cemex |

CRH |

Heidelberg |

LafargeHolcim |

|

Titan |

|

|

|

|

LTM |

|

VMC |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

North East |

|

46.6 |

6% |

0% |

15% |

26% |

12% |

|

15% |

|

|

|

|

|

awards |

revenues |

Buzzi |

Cemex |

CRH |

Heidelberg |

|

LafargeHolcim |

|

Titan |

|

||||||||||

|

|

West |

|

51.3 |

1% |

29% |

28% |

21% |

14% |

|

0% |

|

|

California |

66% |

|

17% |

0% |

|

22% |

0% |

|

15% |

|

0% |

|

|

|

0% |

|

|

||||||

|

|

South |

|

54.1 |

53% |

66% |

30% |

35% |

38% |

|

85% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

Texas |

23% |

|

17% |

35% |

|

17% |

6% |

|

14% |

|

15% |

|

|

0% |

|

|

|||||||||||||||

|

|

Midwest |

|

59.7 |

39% |

5% |

27% |

18% |

36% |

|

0% |

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

Tennessee |

43% |

|

10% |

6% |

|

6% |

2% |

|

0% |

|

1% |

|

|

|

0% |

|

|

||||||||||||||

|

|

Average |

|

52.9 |

55.8 |

53.6 |

53.7 |

52.6 |

54.8 |

|

53.0 |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Virginia |

172% |

|

10% |

0% |

|

0% |

1% |

|

4% |

|

3% |

|

|

|

20% |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Georgia |

-45% |

|

10% |

0% |

|

6% |

0% |

|

3% |

|

3% |

|

|

|

0% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

64% |

41% |

|

51% |

9% |

|

37% |

|

23% |

|

|

20% |

|

||||||

|

Source: Deutsche Bank, AIA |

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank estimates, US DoT, Company data |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13 Page

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

14Page |

|

2017-18 weather has been exceptionally unfavourable in the US |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

■ |

|

Weather impact on volumes in the US has been a recurring theme in 2017 and 2018. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

■ |

|

Our analysis also confirms Q1 18 has been impacted by more freezing days than Q1 17 – however this was more due to exceptionally mild weather |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

conditions in Q1 17 rather than particulary cold weather in Q1 18. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

|

|

|

|

■ |

|

This points as comps for Q1 19 in the US not as easy as investors might believe. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

■ |

|

Our analysis on each company’s US footprint shows however that 2017 and 2018 have seen exceptionally wet weather on all companies’ US footprints |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

(mainly in Q3). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

|

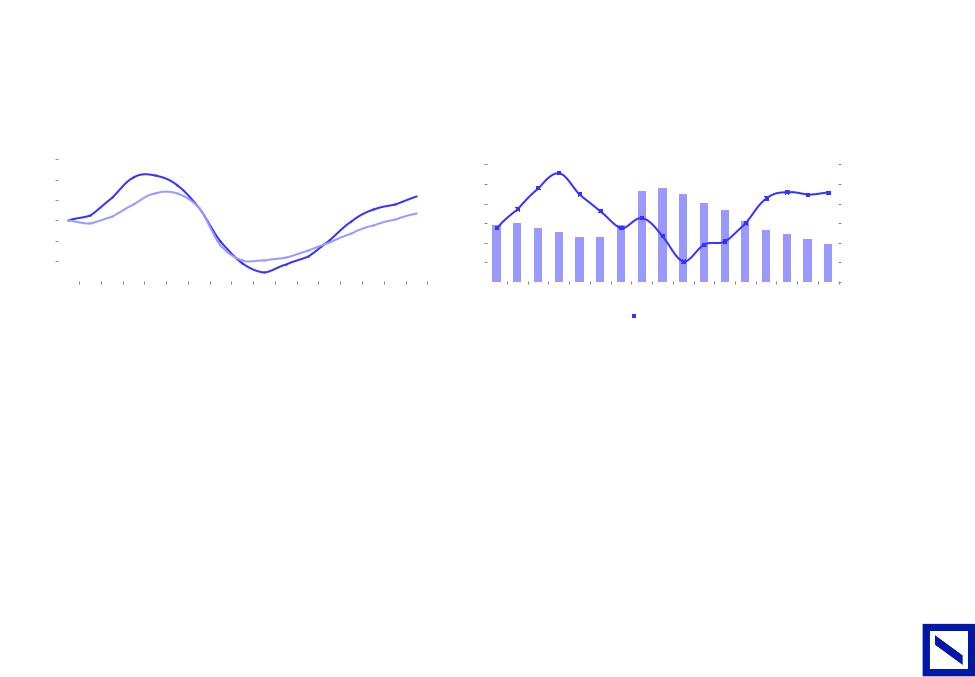

Figure 23: 2017-17 have been exceptionally wet weather years on companies' US footprints |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# of freezing days |

|

|

|

|

|

|

# of days with preci > 15 |

|

|

|

# of days with preci > 25 |

|

|

|

|

# of days with preci > 35 |

|

|

|

||||||||||||||||||||||||||||||||||||||

|

|

Company |

|

|

|

|

2018 |

|

|

2017 |

|

Avg 30y |

|

|

2018 |

|

|

2017 |

|

|

Avg 30y |

|

|

|

2018 |

|

|

2017 |

|

|

Avg 30y |

|

2018 |

|

|

2017 |

|

Avg 30y |

|

||||||||||||||||||||||||||||||||

|

|

Buzzi |

|

|

|

|

|

|

|

|

22 |

|

|

|

|

15 |

|

|

|

|

21 |

|

|

|

67 |

|

|

|

63 |

|

|

56 |

|

|

|

|

|

42 |

|

|

|

40 |

|

|

|

33 |

|

|

|

|

28 |

|

|

|

|

27 |

|

|

|

|

20 |

|

|

|

|||||||

|

|

Cemex |

|

|

|

|

|

|

|

8 |

|

|

|

|

5 |

|

|

|

|

7 |

|

|

|

67 |

|

|

|

64 |

|

|

55 |

|

|

|

|

|

41 |

|

|

|

40 |

|

|

|

30 |

|

|

|

|

24 |

|

|

|

|

25 |

|

|

|

|

17 |

|

|

|

||||||||

|

|

CRH |

|

|

|

|

|

|

|

|

32 |

|

|

|

|

27 |

|

|

|

|

31 |

|

|

|

62 |

|

|

|

61 |

|

|

49 |

|

|

|

|

|

37 |

|

|

|

38 |

|

|

|

27 |

|

|

|

|

23 |

|

|

|

|

24 |

|

|

|

|

16 |

|

|

|

|||||||

|

|

Heidelberg |

|

|

|

|

|

21 |

|

|

|

|

17 |

|

|

|

|

21 |

|

|

|

63 |

|

|

|

61 |

|

|

52 |

|

|

|

|

|

40 |

|

|

|

38 |

|

|

|

30 |

|

|

|

|

26 |

|

|

|

|

25 |

|

|

|

|

17 |

|

|

|

||||||||||

|

|

LafargeHolcim |

|

|

|

30 |

|

|

|

|

22 |

|

|

|

|

29 |

|

|

|

68 |

|

|

|

66 |

|

|

54 |

|

|

|

|

|

42 |

|

|

|

41 |

|

|

|

31 |

|

|

|

|

27 |

|

|

|

|

28 |

|

|

|

|

18 |

|

|

|

||||||||||||

|

|

Titan |

|

|

|

|

|

|

|

|

12 |

|

|

|

|

8 |

|

|

|

|

11 |

|

|

|

107 |

|

|

|

85 |

|

|

73 |

|

|

|

|

|

63 |

|

|

|

51 |

|

|

|

38 |

|

|

|

|

35 |

|

|

|

|

31 |

|

|

|

|

20 |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

Source: Deutsche Bank, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

Figure 24: Average # of days with Temp below 0 degree on companies' |

|

Figure 25: Average # of days with precipitations > 25mm on companies' |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

US footprint |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

US footprint |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

45 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Deutsche |

|

|

|

1989 |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

2000 |

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

|

5 |

|

1989 |

1990 |

1991 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

2000 |

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

|

|

|||

0 |

|

|

0 |

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

AG/London Bank |

|

Source: Deutsche Bank, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Deutsche Bank, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Building European |

2018 December 3 Materials Building |

Construction & |

|

vk.com/id446425943

Deutsche |

|

■ |

Based on the last 30 years monthly analysis, we estimate that precipitations in Q3 have caused 3-6% cement demand loss on companies’ US footprints |

|||||||||||

|

3-6% volume upside on US footprints in case of weather normalization |

|

|

|

|

|||||||||

Bank |

|

|

vs. a more normalized weather pattern. |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|||

AG/London |

|

■ |

We believe Titan has been the most impacted with exceptionally wet weather in Florida and the Mid-Atlantic region in 2018. |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Figure 26: Cement volumes lost in 2018 vs. ‘normalized’ weather conditions |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

# of freezing days |

|

|

|

# of days with precip. > 25mm |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

Total 2018 weather impact |

|

|

|

|

|

|

|

|

Impact cement demand |

|

|

|

|

Impact cement demand |

vs. 30y average on cement |

|

|

|

|

Company |

2018 |

30y avg |

freezing days |

|

|

2018 |

30y avg |

precipitations |

volumes |

|

|

|

|

|

Buzzi |

|

22 |

21 |

0.3% |

|

|

42 |

33 |

2.4% |

2.7% |

|

|

|

|

Cemex |

|

8 |

7 |

0.2% |

|

|

41 |

30 |

3.0% |

3.3% |

|

|

|

|

CRH |

|

32 |

31 |

0.2% |

|

|

37 |

27 |

2.5% |

2.7% |

|

|

|

|

Heidelberg |

21 |

21 |

0.0% |

|

|

40 |

30 |

2.7% |

2.7% |

|

|

|

|

|

LafargeHolcim |

30 |

29 |

0.2% |

|

|

42 |

31 |

2.9% |

3.1% |

|

|

|

|

|

Titan |

|

12 |

11 |

0.1% |

|

|

63 |

38 |

6.8% |

7.0% |

|

|

|

Source: Deutsche Bank estimates, Company data, Bloomberg Finance LP |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|||||||||

|

|

Figure 27: Impact of freezing day on cement demand growth |

Figure 28: Impact of precipitations on cement demand growth: example |

|||||||||||

|

|

|

|

|

|

|

|

|

of Texas in Q3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40% |

|

|

|

|

|

|

|

|

|

|

20% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(%) |

|

|

|

|

30% |

|

|

|

|

|

(%) |

|

|

|

|

15% |

|

2011 |

2004 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

demand |

|

|

|

|

|

|

|

|

y = 0.9764x + 0.0265 |

demand |

|

|

|

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

R² = 0.4714 |

|

|

2006 |

|

|

|

2010 |

|

|

||||

|

|

|

|

20% |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2015 |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2013 |

5% |

2007 |

2014 |

|

|

|

|

|

|

|

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

adj.YoYcement |

|

|

|

|

|

|

|

|

|

|

adj.YoYcement |

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

-20% |

|

|

|

|

|

||

|

-40% |

-30% |

-20% |

-10% |

0% |

10% |

20% |

30% |

40% |

50% |

|

-40% |

-30% |

-20% |

-10% |

-5% 0% |

|

|

10% |

20% |

30% |

|

|

|

|

|

-10% |

|

|

|

|

|

|

y = 0.4944x - 0.001 |

|

2017 |

2016 |

|

|

|

|

||

|

|

|

|

|

|

|

YoY freezing days impact (%) |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

R² = 0.4928 |

|

2012 |

-10% |

2008 |

|

|

||

|

|

|

|

|

-20% |

|

|

|

|

|

|

|

|

|

|

|

YoY precipitations > 25mm |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-15% |

2005 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

impact (%) |

|

|

||

|

|

|

|

|

-30% |

|

|

|

|

|