Accounting For Dummies, 4th edition

.pdf90 |

Part II: Figuring Out Financial Statements |

A business hires a law firm that does a lot of legal work during the year, but the company doesn’t pay the bill until the following year.

A business matches retirement contributions made by its employees but doesn’t pay its share until the following year.

A business has unpaid bills for telephone service, gas, electricity, and water that it used during the year.

Accountants use three different types of liability accounts to record a business’s unpaid expenses:

Accounts payable: This account is used for items that the business buys on credit and for which it receives an invoice (a bill). For example, your business receives an invoice from its lawyers for legal work done. As soon as you receive the invoice, you record in the accounts payable liability account the amount that you owe. Later, when you pay the invoice, you subtract that amount from the accounts payable account, and your cash goes down by the same amount.

Accrued expenses payable: A business has to make estimates for several unpaid costs at the end of the year because it hasn’t yet received invoices for them. Examples of accrued expenses include the following:

•Unused vacation and sick days that employees carry over to the following year, which the business has to pay for in the coming year

•Unpaid bonuses to salespeople

•The cost of future repairs and part replacements on products that customers have bought and haven’t yet returned for repair

•The daily accumulation of interest on borrowed money that won’t be paid until the end of the loan period

Without invoices to refer to, you have to examine your business operations carefully to determine which liabilities of this sort to record.

Income tax payable: This account is used for income taxes that a business still owes to the IRS at the end of the year. The income tax expense for the year is the total amount based on the taxable income for the entire year. Your business may not pay 100 percent of its income tax expense during the year; it may owe a small fraction to the IRS at year’s end. You record the unpaid amount in the income tax payable account.

Note: A business may be organized legally as a pass-through tax entity for income tax purposes, which means that it doesn’t pay income tax itself but instead passes its taxable income on to its owners. Chapter 8 explains these types of business entities. The example I offer here is for a business that is an ordinary corporation that pays income tax.

Chapter 4: Reporting Revenue, Expenses, and the Bottom Line |

91 |

Summing Up the Financial

Effects of Profit

Business managers should understand not only how to make profit, but also the financial effects of making profit. Profit does not simply mean an increase in cash. Sales revenue and expenses affect several assets other than cash and operating liabilities. I realize that I make this point several times in this chapter, so forgive me if I seem to be harping. I simply want to drive home the importance of understanding this fact.

Making profit involves additional transactions that are closely allied with sales and expenses. These tightly connected transactions include the following:

Collecting cash from customers for credit sales made to them, which takes place after recording the sales revenue

Purchasing (or manufacturing) products that are put in inventory and held there until the products are sold sometime later, at which time the cost of products sold is charged to expense in order to match up with the revenue from the sale

Paying certain costs in advance of when they are charged to expense

Paying for products bought on credit and for other items that are not charged to expense until sometime after the purchase

Paying for expenses that have been recorded sometime earlier

Making payments to the government for income tax expense that has already been recorded

These allied transactions are the “before and after” of recording sales and expense transactions. The allied transactions are not reported as such in a financial statement. However, the allied transactions change assets and liabilities, and they definitely affect cash flow. I explain how the changes in assets and liabilities caused by the allied transactions affect cash flow in Chapter 6.

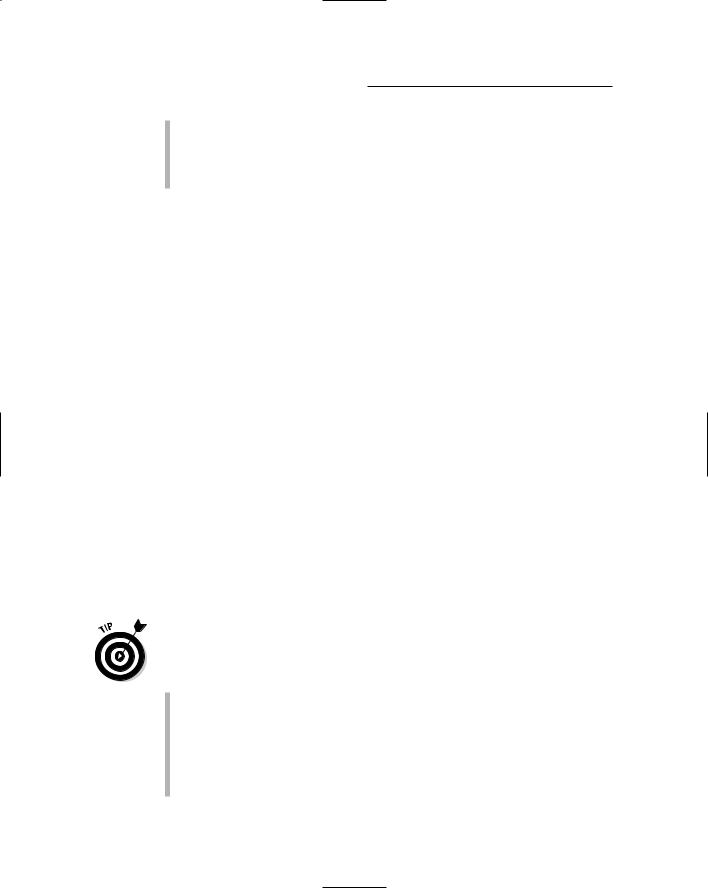

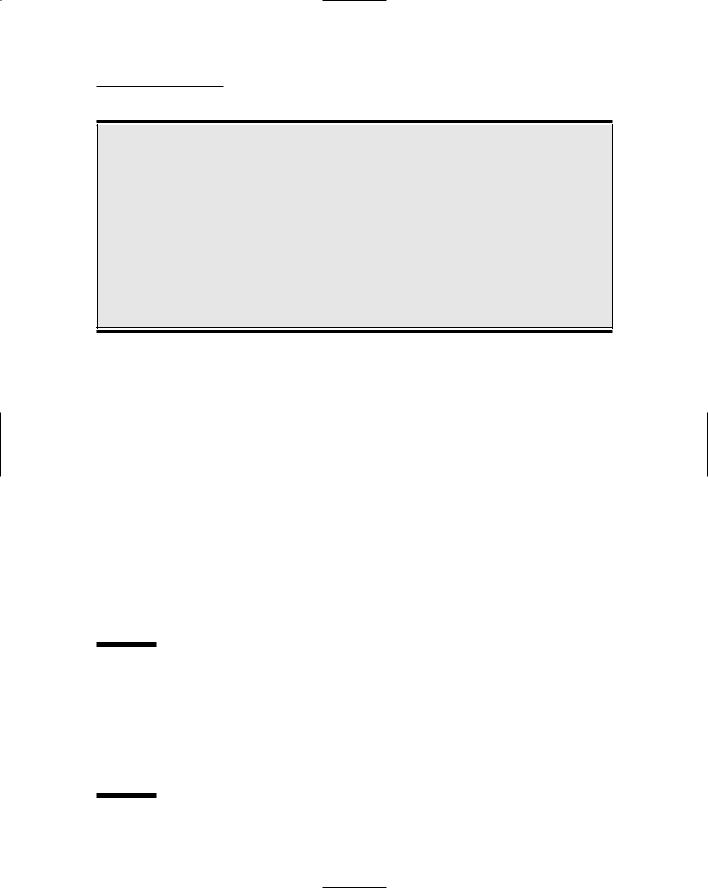

Figure 4-2 is a summary of the changes in assets and liabilities during the year that are caused by a company’s profit-making activities — including the sales and expense transactions (summarized in the income statement) and the allied transactions (which are not reported in a financial statement). This sort of summary is not usually prepared for business managers, nor is such a summary presented in external financial reports. But it is a useful way to sum up the financial consequences of making profit.

92 |

Part II: Figuring Out Financial Statements |

Figure 4-2:

Summary of changes in assets and liabilities from sales, expenses, and their allied transactions during the year.

Typical Business Inc.

Summary of Changes in Assets and Liabilities

from Sales and Expenses and Allied Transactions

Through Year Ended December 31, 2009

Assets

Cash |

$1,515,000 |

|

|

|

Receivables from credit sales |

$450,000 |

|

|

|

Cost of unsold products in inventory |

$725,000 |

|

|

|

Amount of expenses paid in advance |

$75,000 |

|

|

|

Cost of fixed assets, net of depreciation |

($775,000) |

|

|

|

Change in total assets |

|

$1,990,000 |

|

|

Liabilities |

|

|

|

|

Payables for products and things bought on credit |

$125,000 |

|

|

|

Unpaid expenses |

$150,000 |

|

|

|

Income tax payable |

$25,000 |

|

|

|

Change in liabilities |

|

|

$300,000 |

|

Net income for year |

$1,690,000 |

|

||

Note in Figure 4-2 that I use descriptive names for the assets and liabilities, instead of the formal account titles that you see in actual financial statements. You can refer to the formal account titles earlier in the chapter (see the section “Getting Particular about Assets and Liabilities”). When explaining the balance sheet in Chapter 5, I stick to the formal titles of the accounts.

Other transactions also change the assets, liabilities, and owners’ equity of a business, such as borrowing money and buying new fixed assets. These nonrevenue and non-expense transactions are reported in the statement of cash flows, which I explain in Chapter 6.

Reporting Extraordinary

Gains and Losses

I have a small confession to make: The income statement example shown in Figure 4-1 is a sanitized version as compared with actual income statements in external financial reports. If you took the trouble to read 100 income statements, you’d be surprised at the wide range of things you’d find in these statements. But I do know one thing for certain you would discover.

Chapter 4: Reporting Revenue, Expenses, and the Bottom Line |

93 |

Many businesses report unusual, extraordinary gains and losses in addition to their usual revenue, income, and expenses. In these situations, the income statement is divided into two sections:

The first section presents the ordinary, continuing sales, income, and expense operations of the business for the year.

The second section presents any unusual, extraordinary, and nonrecurring gains and losses that the business recorded in the year.

The road to profit is anything but smooth and straight. Every business experiences an occasional discontinuity — a serious disruption that comes out of the blue, doesn’t happen regularly or often, and can dramatically affect its bottom-line profit. In other words, a discontinuity is something that disturbs the basic continuity of its operations or the regular flow of profit-making activities.

Here are some examples of discontinuities:

Downsizing and restructuring the business: Layoffs require severance pay or trigger early retirement costs; major segments of the business may be disposed of, causing large losses.

Abandoning product lines: When you decide to discontinue selling a line of products, you lose at least some of the money that you paid for obtaining or manufacturing the products, either because you sell the products for less than you paid or because you just dump the products you can’t sell.

Settling lawsuits and other legal actions: Damages and fines that you pay — as well as awards that you receive in a favorable ruling — are obviously nonrecurring extraordinary losses or gains (unless you’re in the habit of being taken to court every year).

Writing down (also called writing off) damaged and impaired assets:

If products become damaged and unsellable, or fixed assets need to be replaced unexpectedly, you need to remove these items from the assets accounts. Even when certain assets are in good physical condition, if they lose their ability to generate future sales or other benefits to the business, accounting rules say that the assets have to be taken off the books or at least written down to lower book values.

Changing accounting methods: A business may decide to use a different method for recording revenue and expenses than it did in the past, in some cases because the accounting rules (set by the authoritative accounting governing bodies — see Chapter 2) have changed. Often,

the new method requires a business to record a one-time cumulative effect caused by the switch in accounting method. These special items can be huge.

94 |

Part II: Figuring Out Financial Statements |

Correcting errors from previous financial reports: If you or your accountant discovers that a past financial report had an accounting error, you make a catch-up correction entry, which means that you record a loss or gain that had nothing to do with your performance this year.

According to financial reporting standards (GAAP), which I explain in Chapter 2, a business must make these one-time losses and gains very visible in its income statement. So in addition to the main part of the income statement that reports normal profit activities, a business with unusual, extraordinary losses or gains must add a second layer to the income statement to disclose these out-of-the-ordinary happenings.

If a business has no unusual gains or losses in the year, its income statement ends with one bottom line, usually called net income (which is the situation shown in Figure 4-1). When an income statement includes a second layer, that line becomes net income from continuing operations before unusual gains and losses. Below this line, each significant, nonrecurring gain or loss appears.

Say that a business suffered a relatively minor loss from quitting a product line and a very large loss from adopting a new accounting standard. The second layer of the business’s income statement would look something like the following:

Net income from continuing operations |

$267,000,000 |

Discontinued operations, net of income taxes |

($20,000,000) |

Earnings before cumulative effect of changes |

$247,000,000 |

in accounting principles |

|

Cumulative effect of changes in accounting principles, |

($456,000,000) |

net of income taxes |

|

Net earnings (loss) |

($209,000,000) |

The gains and losses reported in the second layer of an external income statement are generally complex and may be quite difficult to follow. So where does that leave you? In assessing the implications of extraordinary gains and losses, use the following questions as guidelines:

Were the annual profits reported in prior years overstated?

Why wasn’t the loss or gain recorded on a more piecemeal and gradual year-by-year basis instead of as a one-time charge?

Was the loss or gain really a surprising and sudden event that could not have been anticipated?

Will such a loss or gain occur again in the future?

Chapter 4: Reporting Revenue, Expenses, and the Bottom Line |

95 |

Every company that stays in business for more than a couple of years experiences a discontinuity of one sort or another. But beware of a business that takes advantage of discontinuities in the following ways:

Discontinuities become continuities: This business makes an extraordinary loss or gain a regular feature on its income statement. Every year or so, the business loses a major lawsuit, abandons product lines, or restructures itself. It reports “nonrecurring” gains or losses from the same source on a recurring basis.

A discontinuity is used as an opportunity to record all sorts of writedowns and losses: When recording an unusual loss (such as settling a lawsuit), the business opts to record other losses at the same time, and everything but the kitchen sink (and sometimes that, too) gets written off. This so-called big-bath strategy says that you may as well take a big bath now in order to avoid taking little showers in the future.

A business may just have bad (or good) luck regarding extraordinary events that its managers could not have predicted. If a business is facing a major, unavoidable expense this year, cleaning out all its expenses in the same year so it can start off fresh next year can be a clever, legitimate accounting tactic. But where do you draw the line between these accounting manipulations and fraud? All I can advise you to do is stay alert to these potential problems.

Closing Comments

The income statement occupies center stage; the bright spotlight is on this financial statement because it reports profit or loss for the period. But remember that a business reports three primary financial statements — the other two being the balance sheet and the statement of cash flows, which I discuss in the next two chapters. The three statements are like a three-ring circus. The income statement may draw the most attention, but you have to watch what’s going on in all three places. As important as profit is to the financial success of a business, the income statement is not an island unto itself.

Also, keep in mind that financial statements are supplemented with footnotes and contain other commentary from the business’s executives. If the financial statements have been audited, the CPA firm includes a short report stating whether the financial statements have been prepared in conformity with GAAP. Chapter 15 explains audits and the auditor’s report.

I don’t like closing this chapter on a sour note, but I must point out that an income statement you read and rely on — as a business manager, investor, or lender — may not be true and accurate. In most cases (I’ll even say in the large majority of cases), businesses prepare their financial statements in

96 |

Part II: Figuring Out Financial Statements |

good faith, and their profit accounting is honest. They may bend the rules a little, but basically their accounting methods are within the boundaries of GAAP even though the business puts a favorable spin on its profit number.

But some businesses resort to accounting fraud and deliberately distort their profit numbers. In this case, an income statement reports false and misleading sales revenue and/or expenses in order to make the bottom-line profit appear to be better than the facts would support. If the fraud is discovered at a later time, the business puts out revised financial statements. Basically, the business in this situation rewrites its profit history. I wish I could say that this doesn’t happen very often, but the number of high-profile accounting fraud cases in recent years has been truly alarming. The CPA auditors of these companies did not catch the accounting fraud, even though this is one purpose of an audit. Investors who relied on the fraudulent income statements ended up suffering large losses.

Anytime I read a financial report, I keep in mind the risk that the financial statements may be “stage managed” to some extent — to make year-to-year reported profit look a little smoother and less erratic, and to make the financial condition of the business appear a little better. Regretfully, financial statements don’t always tell it as it is. Rather, the chief executive and chief accountant of the business fiddle with the financial statements to some extent. I say much more about this tweaking of a business’s financial statements in later chapters.

Chapter 5

Reporting Assets, Liabilities,

and Owners’ Equity

In This Chapter

Identifying three basic types of business transactions

Classifying assets and liabilities

Connecting revenue and expenses with their assets and liabilities

Examining where businesses go for capital

Understanding balance sheet values

This chapter explores one of the three primary financial statements reported by businesses — the balance sheet, which is also called the

statement of financial condition and the statement of financial position. This financial statement is a summary at a point in time of the assets of a business on the one hand, and the liabilities and owners’ equity sources of the business on the other hand. It’s a two-sided financial statement, which can be condensed in the accounting equation:

Assets = Liabilites + Owners’ equity

The balance sheet may seem to stand alone — like an island to itself — because it’s presented on a separate page in a financial report. But keep in mind that the assets and liabilities reported in a balance sheet are the results of the activities, or transactions, of the business. Transactions are economic exchanges between the business and the parties it deals with:

customers, employees, vendors, government agencies, and sources of capital. Transactions are the stepping stones from the start-of-the year to the end- of-the-year financial condition.

98 |

Part II: Figuring Out Financial Statements |

Understanding That Transactions

Drive the Balance Sheet

A balance sheet is a snapshot of the financial condition of a business at an instant in time — the most important moment in time being at the end of the last day of the income statement period. If you read Chapter 4, you’ll notice that I continue using the same business example in this chapter. The fiscal, or accounting, year of the business ends on December 31. So its balance sheet is prepared at the close of business at midnight December 31. (A company should end its fiscal year at the close of its natural business year or at the close of a calendar quarter — September 30, for example.) This freeze-frame nature of a balance sheet may make it appear that a balance sheet is static. Nothing is further from the truth. A business does not shut down to prepare its balance sheet. The financial condition of a business is in constant motion because the activities of the business go on nonstop.

The activities, or transactions, of a business fall into three basic types:

Operating activities: This category refers to making sales and incurring expenses, and also includes the allied transactions that are part and parcel of making sales and incurring expenses. For example, a business records sales revenue when sales are made on credit, and then, later, records cash collections from customers. Another example: A business purchases products that are placed in its inventory (its stock of products awaiting sale), at which time it records an entry for the purchase. The expense (the cost of goods sold) is not recorded until the products are actually sold to customers. Keep in mind that the term operating activities includes the allied transactions that precede or are subsequent to the recording of sales and expense transactions.

Investing activities: This term refers to making investments in assets and (eventually) disposing of the assets when the business no longer needs them. The primary examples of investing activities for businesses that sell products and services are capital expenditures, which are the amounts spent to modernize, expand, and replace the long-term operating assets of a business.

Financing activities: These activities include securing money from debt and equity sources of capital, returning capital to these sources, and making distributions from profit to owners. Note that distributing profit to owners is treated as a financing transaction, not as a separate category.

Wondering where to find these transactions in a financial report? See the sidebar “How transactions are reported in financial statements.”

Chapter 5: Reporting Assets, Liabilities, and Owners’ Equity |

99 |

How transactions are reported in financial statements

Sales revenue and expenses, as well as any gains or losses that are recorded in the period, are reported in the income statement. However, the total flows during the period of the allied transactions connected with sales and expenses are not reported. For example, the total of cash collections from customers from credit sales made to them is not reported. The net changes

in the assets and liabilities directly involved in operating activities are reported in the statement of cash flows (see Chapter 6). Financing and investing transactions are also found in the statement of cash flows. (Reporting the cash flows from investing and financing activities is one of the main purposes of the statement of cash flows.)

Figure 5-1 shows a summary of changes in assets, liabilities, and owners’ equity during the year for the business example I introduce in Chapter 4. Notice the middle three columns in Figure 5-1, for each of the three basic types of activities of a business. One column is for changes caused by its revenue and expenses and their allied transactions during the year, which collectively are called operating activities. The second column is for changes caused by its investing activities during the year. The third column is for the changes caused by its financing activities.

Typical Business, Inc.

Statement of Changes in Assets, Liabilities, and Owners’ Equity for Year Ended December 31, 2009

(Dollar amounts in thousands)

Figure 5-1:

Summary of changes in assets, liabilities, and owners’ equity during the year.

|

Beginning |

Operating |

|

Investing |

|

|

Financing |

|

|

Ending |

|

|

Balances |

Activities |

|

Activities |

|

|

Activities |

|

|

Balances |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash |

$2,275 |

|

$1,515 |

($1,275) |

($350) |

$2,165 |

|||||

Accounts receivable |

$2,150 |

|

$450 |

|

|

|

|

|

$2,600 |

||

Inventory |

$2,725 |

|

$725 |

|

|

|

|

|

$3,450 |

||

Prepaid expenses |

$525 |

|

$75 |

|

|

|

|

|

$600 |

||

Fixed assets, net of depreciation |

$5,535 |

|

($775) |

$1,275 |

|

|

|

|

$6,035 |

||

Assets |

$13,210 |

|

$1,990 |

|

|

($350) |

$14,850 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

Accounts payable |

$640 |

|

$125 |

|

|

|

|

|

$765 |

||

Accrued expenses payable |

$750 |

|

$150 |

|

|

|

|

|

$900 |

||

Income tax payable |

$90 |

|

$25 |

|

|

|

|

|

$115 |

||

Interest-bearing debt |

$6,000 |

|

|

|

|

$250 |

$6,250 |

||||

O.E.-invested capital |

$3,100 |

|

|

|

|

$150 |

$3,250 |

||||

O.E.-retained earnings |

$2,630 |

|

$1,690 |

|

|

|

($750) |

|

$3,570 |

||

Liabilities & owners’ equity |

$13,210 |

|

$1,990 |

|

|

($350) |

$14,850 |

||||

|

|

|

|

|

|

|

|

|

|

|

|