Ksg Agro On the road to space/Not ready to be public

Lowest cost Ukrainian agriproducer: only USD 228 applied to ha of sunflower in 2010 vs. USD 386 on average for listed peers; USD 115/ha of wheat vs. USD 355/ha on average for listed peers

One of the highest margins thanks to its low-cost operations and heavy bias toward sunflowers in its crop rotation: 44%-64% EBITDA margin in 2009-10, net of biological revaluation

Located in sunflower-favourable Dnipropetrovsk region, resulting in a high risk, high return operation

Scattered and overambitious growth strategy with announced projects requiring CapEx of 12x-30x of 2010 EBITDA

Risks: ability to keep costs low, management accountability, high concentration in one region and on one crop, poor disclosure

Watch list:

2011 annual report: end of May

Landbank acquisition: up to 20 ths ha expected during summer

2012 harvest results: July-October 2012

Company description

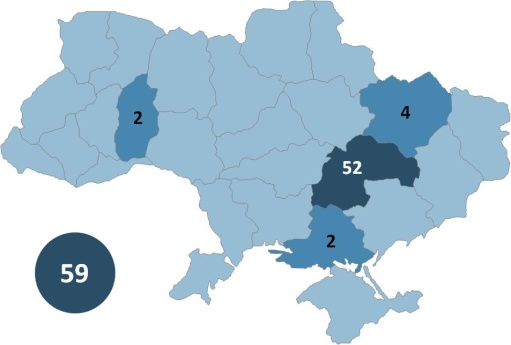

Low-cost mid-sized farming company located in sunflower-favorable Dnipropetrovsk region. Landbank has grown from 33 ths ha at IPO in May 2010 to 59.3 ths ha as of early 2012, with further growth plans still the most ambitious among listed names. Owns 16 kt grain storage facility. Acquired 50% stake in a pork farm in the same region in October 2011. Announced plans in January 2012 to construct a 60-90 kt pellet production plant.

Selected financials, USD mln and ratios |

|||||

|

2010 |

2011E |

yoy |

2012E |

yoy |

Net revenue |

15.6 |

18.1 |

16% |

31.2 |

72% |

Gross margin, % |

67% |

68% |

1pp |

58% |

-10pp |

EBITDA |

10.1 |

11.9 |

18% |

17.3 |

46% |

EBITDA margin, % |

64% |

65% |

1pp |

55% |

-10pp |

Net income |

7.9 |

8.5 |

9% |

12.5 |

46% |

Net margin, % |

50% |

47% |

-3pp |

40% |

-7pp |

|

|

|

|

|

|

PP&E, net |

5.0 |

20.3 |

4.0x |

36.2 |

78% |

Shareholder equity |

11.7 |

45.3 |

3.9x |

57.9 |

28% |

LT debt |

2.4 |

0.0 |

-100% |

0.0 |

n/m |

ST debt |

5.4 |

5.3 |

-2% |

5.4 |

2% |

Total liabilities & equity |

26.3 |

53.7 |

2.0x |

66.9 |

24% |

|

|

|

|

|

|

Operating Cash Flow |

10.0 |

-3.6 |

n/m |

10.1 |

n/m |

CapEx |

0.8 |

17.3 |

21x |

19.5 |

13% |

|

|

|

|

|

|

Working Capital |

8.6 |

13.6 |

59% |

19.7 |

44% |

|

|

|

|

|

|

Harvest value, USD/ha |

583 |

549 |

-6% |

544 |

-1% |

Gross profit, USD/ha |

388 |

307 |

-21% |

252 |

-18% |

|

|

|

|

|

|

ROA |

30% |

21% |

-9pp |

21% |

-1pp |

ROE |

68% |

30% |

-38pp |

24% |

-6pp |

ROIC |

35% |

36% |

1pp |

20% |

-15pp |

Source: Company Data, Concorde Capital estimates |

|||||

Market data |

|

Bloomberg |

|

Reuters |

|

Recommendation |

|

Price, PLN |

|

12M target, PLN |

|

Upside |

|

No of shares, mln |

|

Market Cap, PLN mln |

|

52-week performance |

|

52-week range, PLN |

|

ADT, 12M, PLN mln |

|

Free float, % |

|

Free float, PLN mln |

|

Source: Bloomberg |

|

KSG PW |

Current: |

PLN 21.7 |

HOLD |

Target: |

PLN 25.0 |

Ownership structure |

|

Sergey Mazin |

xx.x% |

Free float |

xx.x% |

Source: Company data, Concorde Capital estimates |

|

Share price performance (1) |

|

(1) Hereafter, share prices as of XXX XX, XXXX Source: Bloomberg |

Multiples and per-share data |

|||

|

2008 |

2009E |

2010E |

EV/Capacity |

xx |

xx |

xx |

EV/Output |

xx |

xx |

xx |

|

|

|

|

EV/Sales |

xx |

xx |

xx |

EV/EBITDA |

xx |

xx |

xx |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Bloomberg, Company data, Concorde Capital estimates

Company`s

landbank, ths ha

Source: Company data, Concorde Capital

|

|||