65. Short-Term Investments, Long-Term Investments (Debt, Equity). Краткосрочные инвестиции. Долгосрочные инвестиции (долг, капитал).

The accounting methods used to record investments are directly related to how much is owned and how long management intends to hold the investments.

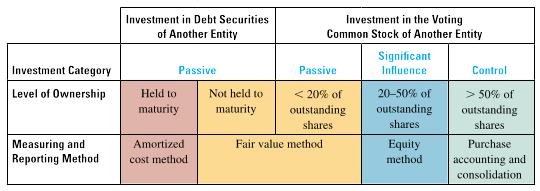

Passive investments are made to earn a return on funds that may be needed for future short-term or long-term purposes. This category includes both investments in debt (bonds and notes) and equity securities (stock). Debt securities are always considered passive investments. If the company intends to hold the securities until they reach maturity, the investments are measured and reported at amortized cost. If they are to be sold before maturity, they are reported using the fair value method. NB! Under IFRS amortized cost of bonds are not extracted from its value, rather capitalized into equity!

For investments in equity securities, the investment is presumed passive if the investing company owns less than 20 percent of the outstanding voting shares of the other company. The fair value method is used to measure and report the investments.

Significant influence is the ability to have an important impact on the operating, investing, and financing policies of another company. Significant influence is presumed if the investing company owns from 20 to 50 percent of the outstanding voting shares of the other company. The equity method is used to measure and report this category of investments.

C ontrol

is the ability to determine the operating and financing policies of

another company through ownership of voting stock. Control is

presumed when the investing company owns more than 50 percent of the

outstanding voting stock of the other company. Purchase accounting

and consolidation are applied to combine the companies. These

investment categories and the appropriate measuring and reporting

methods can be summarized as follows:

ontrol

is the ability to determine the operating and financing policies of

another company through ownership of voting stock. Control is

presumed when the investing company owns more than 50 percent of the

outstanding voting stock of the other company. Purchase accounting

and consolidation are applied to combine the companies. These

investment categories and the appropriate measuring and reporting

methods can be summarized as follows:

Bond Purchases. On the date of purchase, a bond may be acquired at the maturity amount (at par), for less than the maturity amount (at a discount), or for more than the maturity amount (at a premium). The total cost of the bond, including all incidental acquisition costs such as transfer fees and broker commissions, is debited to the Held-to-Maturity Investments account. Depending on management’s intent, passive investments at fair value may be classified as trading securities or securities available for sale.

Trading securities are actively traded with the objective of generating profits on short-term changes in the price of the securities. This approach is similar to the one taken by many mutual funds. The portfolio manager actively seeks opportunities to buy and sell securities. Trading securities are classified as current assets on the balance sheet.

Most companies do not actively trade the securities of other companies. Instead, they invest to earn a return on funds they may need for future operating purposes. Other than debt securities to be held to maturity, these debt and equity investments are called securities available for sale. They are classified as current or noncurrent assets on the balance sheet depending on whether management intends to sell the securities during the next year.

Under the equity method, the investor’s 20 to 50 percent ownership of a company presumes significant influence over the affiliate’s process of earning income. As a consequence, the investor reports its portion of the affiliate’s net income as its income and increases the investment account by the same amount.