Учебник Английский язык

.pdfaction |

action |

admission |

conference |

contingency |

confidence |

damage |

information |

flow |

liability |

legal |

limitation |

loss |

plan |

press |

plan |

press |

release |

speed |

response |

b) Complete these sentences with the word partnerships above.

1.How quickly management react to a crisis is known as the …

2.In a breaking crisis, a manager may speak to the media at a(n) …

3.Alternatively, they may have a written statement which is given to the media in the form of a ….

4.During the crisis, management may choose to keep customers, employees and shareholders up to date with a regular ….

5.A strategy for dealing with a crisis is a(n) …

6.A backup strategy is a(n) …

7.The risk of being taken to court is the threat of …

8.An acceptance of responsibility in a crisis is a(n) …

9.Following a crisis, a company may suffer a decline in loyalty from its customers, or a(n) … in its product or service.

10.Minimising the negative effects of a crisis is known as …

4. Answer these questions.

Which of the above would you expect to happen or be needed a) before a crisis? b) during a crisis? c) after a crisis? Which of the above, in your opinion, should exist all the time?

Effective Risk Management

1. Which item in each of the categories below carries the most and the least risk? Explain why.

Travel |

Lifestyle |

Money |

Shopping |

car |

drinking alcohol |

property |

online |

plane |

poor diet |

stocks and share |

mail order |

train |

smoking |

savings account |

private sales |

ship |

jogging |

cash |

auction |

2.Are you a risk-taker? What risks have you taken?

3.What risks do businesses face? Note down three types.

4.Read the passage below. In most of the lines 1-10 there is one extra word which does not fit. Find them and write in the space provided. Some lines, however, are correct.

In its everyday sense, risk often has negative connotations and is associated |

1 ……………. |

with danger, the loss, or accidents. |

2 ……………. |

In business, however, the concept is slightly more complex one. Risk is not |

3 ……………. |

Only about threats, but also about opportunities. This is summarised as in the |

4 ……………. |

popular saying who ‘nothing ventured, nothing gained’. Indeed, in order to |

5 ……………. |

grow, to become more profitable or competitive, businesses usually have to |

6 ……………. |

change direction, which it involves a certain amount of risk. Having said that, |

7 ……………. |

in business doing nothing is potentially more risky than moving forward and |

8 ……………. |

innovating. A company that plays it safe all the time and runs the risk of |

9 ……………. |

offering products which go unnoticed or which no longer meet up the needs of |

10 …………... |

their customers. |

|

VOCABULARY

1. The verbs in the box are used to describe risk. Check their meanings and put them under the appropriate heading.

calculate |

eliminate |

encounter |

estimate |

face |

foresee |

minimise |

prioritise |

reduce |

spread |

Predict |

Meet |

Access |

Manage |

|

2. Match these halves of sentences from newspaper extracts.

1 |

Internet businesses |

a) risks involved when sending staff to work |

in |

dangerous locations. |

|

|

|

|

2 We can reduce risk.... |

b) in order to advise insurance companies. |

|

3 Trying to minimise risk … |

c) involved in setting up a new business |

|

4 |

It is impossible to ... |

d) involved in setting up a new business |

5 |

It is difficult to foresee the risks ... e) eliminate all risk when entering a new |

|

6 Actuaries calculate risk |

market |

|

7 |

It’s important to consider the... |

f) is an important part of business strategy |

g)by spreading our lending to more businesses

h)face increasing risks of running out of money.

3.The following adjectives can be used with the word risk. Which describe a high level of risk? Which describe a low level?

faint |

great |

huge |

minuscule |

negligible |

remote |

serious |

significant |

slight |

substantial |

terrible |

tremendous |

4. In pairs, talk about the risks facing one of the following:

1 your company / institution

2 your city / town

3 your country.

READING

1.In today’s fast-changing world, how far ahead can companies realistically plan for the future?

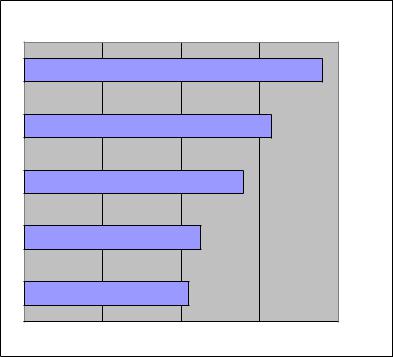

2.The following risks are of concern to senior executives. Where do you think they fit into the table below?

Changes in customer demand

Loss of productivity due to staff absence / staff turnover

Increased competition

Losing key staff to competitors

Changes in demographics

The risks that concern senior executives

…………………………….. 1

…………………………….. 2

…………………………….. 3

Losing key staff to competitors

Changes in demographic

0% |

20% |

40% |

60% |

80% |

The dangers of not looking ahead

By Andrew Bolger

Risk management has undoubtedly moved up the corporate agenda in recent years with fears of war and terrorism being added to the usual list of business worries.

Shivan Subramaniam, the Chairman and Chief Executive of FM Global, a commercial and industrial property insurer, says: ‘Corporations are operating in a turbulent world where businesses are seeking growth through globalisation, outsourcing, consolidation, just-in-time delivery and cross-border supply, further increasing their potential exposure to risk.’

‘Add regulatory, legal and labour considerations, and you begin to understand the complex nature of business risk in the 21st century. While acts of terrorism receive the most coverage, it’s the more traditional events such as fires, floods, explosions, power failures or natural disasters that have the biggest impact.’ FM Global believes the majority of all loss can be prevented or minimised and this should be the first part of any disaster recovery plan. It also argues that

prevention is better than cure and says there is a lot companies can do to stop such events from becoming a disaster in the first place.

However, research shows that more than one-third of the world’s leading companies are not sufficiently prepared to protect their main revenue sources and have room for improvement.

Ken Davey, a managing director with FM Global, says: ‘To best protect cash flow, competitive position and profit, companies need to assess the potential hazards that can impact top revenue sources and make sure there is business continuity planning.’

Lord Levene, chairman of the Lloyd’s insurance market, said recently that companies must be prepared for business interruptions, which accounted for 25 per cent of the $40bn lost as a result of the September 11 terrorist attacks. It was estimated that 90 per cent of medium to large companies that could not resume near-normal operations within five days of an emergency would go out of business.

‘Looking ahead 10 years I firmly believe that the most successful, least crisis-prone businesses will be those whose boards have shown firm resolve and taken decisive action,’ Lord Levene said. ‘Effective, integrated strategies for dealing with tomorrow’s risks require a change in culture at board level now.’

A new research report from Marsh, the world's biggest insurance broker, found that half of European companies did not know how to manage the most significant risks to their business.

Most of Europe’s senior executives surveyed admitted that they did not have procedures in place to manage properly operational and strategic risks, which were responsible for most company failures in the twenty-first century. The survey found that the three most significant risks, and those that businesses felt least able to manage, were:

•Increased competition

•Adverse changes in customer demand

•Reduced productivity because of staff absenteeism and turnover.

‘While business leaders are aware that these risks are the most threatening to their future survival and growth they are scratching their heads when it comes to protecting their businesses against them,’ says Neil Irwin, European development director of Marsh’s corporate client practice. ‘Management no processes could easily help companies identify and address these risks. Instead, too many companies take a low-level approach to risk management preferring to focus on easy-to-solve risks, such as asset protection and health and safety.’

Mr Irwin says: ‘Risk is dynamic, it changes with the environment. Unless businesses accept this and review risk regularly, they could eventually find themselves in a state of crisis, struggling to survive rather than focused on growth. Business leaders have an obligation to their employees, shareholders and other stakeholders to properly protect themselves against risk. Businesses that do attempt to manage these risks will boost their bottom lines.’

From the Financial Times

3.What types of risk are mentioned in the first three paragraphs?

4.Why are companies paying more attention to risk management?

5.Match the follow word partnerships as they appear in the article

1 business |

a) hazards |

2 recovery |

b) interruptions |

3 decisive |

c) sources |

4 potential |

d) operations |

5 integrated |

e) plan |

6 revenue |

f) strategies |

7 near-normal |

g) action |

6. Match the word partnerships to the most appropriate verb below. For example: develop integrated strategies

take protect assess develop implement resume prepare for

7. Make your predictions.

Which types of risk do you think will

a)more significant in the next 50 years?

b)become less significant in the next 50 years?

Part 5 |

RECRUITMENT |

Brainstorm ideas how to find right person for a job. Complete a mind-map.

Right person for a job

VOCABULARY

1. Read the information below. Complete your sentences with the words in bold.

The process of finding people for particular jobs is recruitment, or hiring. Someone who has been recruited is a recruit, or in American English, a hire. The company employs or hires them, they join the company. A company may recruit employees directly or use outside recruiters, recruitment agencies or employment agencies. Outside specialists called headhunters may be called on to headhunt people for very important jobs, persuading them to leave the organizations they already work for. This process is called headhunting. Managers found in this way are headhunted. Executives may be persuaded to move company by the promise of a golden hello: a large sum of money or some other financial enticement offered by the company they move to.

2. a) Match the verbs 1 to 6 to the nouns a) to f) to make word partnerships.

1. to train |

a) a vacancy / post |

2. to shortlist |

b) an interview panel |

3. to advertise |

c) the candidates |

4. to assemble |

d) references |

5. to make |

e) new staff |

6. to check |

f) a job offer |

Now decide on a possible order for the events above from the employer’s point of view.

b) Read the talk of consultant about the recruitment process to check your answers.

Well, what usually happens is that an employer will advertise a vacancy or new post – sometimes both inside and outside the company. Then, after they have received all the applications, they shortlist the candidates, choosing those who appear to meet their criteria. Next, they will assemble an interview panel and call the candidates to an interview. Some employers choose to check references at this stage to avoid delays later, while others wait until after the interview when they

have chosen one of the candidates. Provided the panel are happy, the employer will make a job offer and the successful candidate starts work. Often they attend induction sessions or are given a mentor who helps to train new staff.

3. Complete the text using words or phrases from the box.

curriculum vitae (CV) / resume |

probationary period |

||

interview |

|

|

|

application form |

psychometric test |

covering letter |

|

These days many applicants submit their ..…..1 speculatively to companies they would like to work for. In other words, they do not apply for an advertised job but hope the employer will be interested enough to keep their CV on file and contact them when they have a vacancy. When replying to an advertisement, candidates often fill in a / an …….2 and write a / an …….3. The employer will then invite the best candidates to attend a / an …….4. Sometimes candidates will take a / an …….5 before the interview to assess their mental ability and reasoning skills. These days it is normal for successful candidates to have to work a / an ……6 in a company. This is usually three or six months; after that they are offered a permanent post.

4. a) Which of these words would you use to describe yourself in a work or study situation? Add any other useful words.

• |

motivated |

• confident |

• reliable |

• proud |

• |

dedicated |

• loyal |

• determined |

• charismatic |

• |

honest |

• adaptable |

• resourceful |

• meticulous |

b) Compare your answers with a partner. Which of the qualities in a) do you think are the most important to be successful in a job?

5. Choose the correct alternatives to complete the text below.

Employees who leave a company are not always replaced. Sometimes the company examines the (1) ......... for the post, and decides that it no longer needs to be filled. On other occasions the company will replace the person who resigns with an internal candidate who can be (2) ......... (or moved sideways) to the job. Or it will advertise the position in newspapers or trade journals, or engage an employment (3) ......... to do so. For junior management positions, employers occasionally recruit by giving presentations and holding interviews in universities, colleges and business schools. For senior positions, companies sometimes use the

services of a firm of (4) |

.......... who already have the details of promising |

||

managers. |

|

|

|

|

People looking for work or wanting to change their job generally read the |

||

(5) |

......... advertised in newspapers. To reply to an advertisement is to (6) |

......... for |

|

a job; you become an (7) ......... |

or a candidate. You write a/an (8) .......... |

or fill in |

|

the company's application form, and send it, along with your (9) ......... (GB) or resume (US). You are often asked to give the names of two people who are prepared to write a (10) ......... for you. If you have the right qualifications and abilities, you might be (11) .......... i.e. selected to attend a/an (12) ......... .

It is not uncommon for the (13)......... department or the managers responsible for a particular post to spend eighty or more working hours on the recruitment of a single member of staff. However, this time is well-spent if the company appoints

the right person for the job. |

|

|

|

1. |

a. job description |

b. job satisfaction |

c. job security |

2. |

a. advanced |

b. employed |

c. promoted |

3. |

a. agency |

b. centre |

c. company |

4. |

a. headhunters |

b. headquarters |

c. headshrinkers |

5. |

a. openings |

b. opportunities |

c. vacancies |

6. |

a. apply |

b. applicate |

c. candidate |

7. |

a. appliance |

b. applicant |

c. application |

8. |

a. appliance |

b. application |

c. demand |

9. |

a. job history |

b. curriculum vitae (CV) |

c. life history |

10. a. reference |

b. report |

c. testimony |

|

11. a. appointed |

b. employed |

c. short-listed |

|

12. a. examination |

b. interview |

c. trial |

|

13. a. personal |

b. personnel |

c. resources |

|

How to select the best candidate and avoid the worst

READING

1. Read the text below and decide if the following statements are true (T) or false (F).

1)Traditionally, candidates for executive positions have been evaluated on their technical skills.

2)The principal aim of testing is to find out how candidates have performed in the past.

3)Today, choosing the wrong person for a position can have more serious consequences than 10 years ago.

4)Most interviewers select candidates for their professional abilities.

5)Candidates are now better prepared for interviews than they were in the past.

FIT FOR HIRING? IT’S MIND OVER MATTER

By Judith H. Dobrzynski

NEW YORK – Members of America’s professional and managerial classes have always left college confident of at least one thing: they had taken their last test. From here on, they could rely on charm, cunning and/or a record of accomplishment to propel them up the corporate ladder.

But that’s not necessarily true any longer. A growing number of companies, from General Motors Corp to American Express Co., are no longer satisfied with traditional job interviews. Instead, they are requiring applicants for many whitecollar jobs – from top executives down – to submit a series of paper and pencil tests, role-playing exercises, simulated decision-making exercises and brainteasers. Others put candidates through a long series of interviews by psychologists or trained interviewers.

The tests are not about mathematics or grammar, nor about any of the basic technical skills for which many production, sales or clerical workers have long been tested. Rather, employers want to evaluate candidates on intangible qualities: Is she creative or entrepreneurial? Can he lead and coach? Is he flexible and capable of learning? Does she have passion and a sense of urgency? How will he function under pressure? Most important, will the potential recruit fit the corporate culture?

These tests, which can take from an hour to two days, are all part of a broader trend. ‘Companies are getting much more careful about hiring,’ said Paul R. Ray Jr., chairman of the Association of Executive Search Consultants.

Ten years ago, candidates could win a top job with the right look and the right answers to the question such as ‘Why do you want this job?’ Now, many are having to face questions and exercises intended to learn how to get things done.

They may, for example, have to describe in great detail not one career accomplishment but many – so that patterns of behavior emerge. They may face questions such as ‘Who is the best manager you ever worked for and why?’ or ‘What is your best friend like?’ The answers, psychologists say, reveal much about a candidate’s management style and about himself or herself.

The reason for the interrogations is clear: many hires work out badly. About 35 percent of recently hired senior executives are judged failures, according to the Center for Creative Leadership in Greensboro, North Carolina, which surveyed nearly 500 chief executives.

The cost of bringing the wrong person on board is sometimes huge. Searching and training can cost from $5000 for a lower level manager to $250,000 for a top executive. Years of corporate downsizing, a trend that has slashed layers of management, has also increased the potential damage that one bad executive can do. With the pace of change accelerating in markets and technology, companies what to know how an executive will perform, not just how he or she had performed.

‘Years ago, employers looked for experience – has a candidate done this before?’ said Harold P. Weinstein, executive vice-president of Caliper, a personnel testing and consulting firm in Princeton, New Jersey. ‘But having experience in a job doesn’t guaranty that you can do it in a different environment.’