Построение периодического тренда

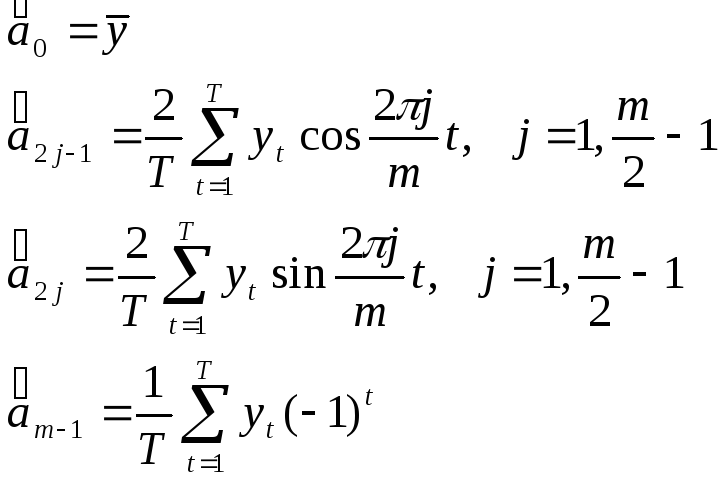

После того, как мы определили длину периода (m=14) можно произвести оценку коэффициентов периодического тренда с помощью МНК, используя следующие формулы:

или сделать это, используя статистические пакеты (например ППП «Statgraphics»). Результаты расчетов можно посмотреть в Приложении №7 . В итоге получаем:

|

j = |

1 |

2 |

3 |

4 |

5 |

6 |

|

A2j-1 = |

-5,4915 |

-3,4956 |

-0,0397 |

0,4497 |

0,0386 |

0,1922 |

|

A2j = |

1,8310 |

3,6666 |

-1,3575 |

1,3088 |

0,7354 |

0,7131 |

|

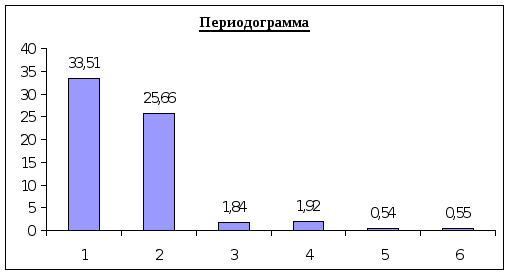

Rj = |

33,5094 |

25,6631 |

1,8443 |

1,9153 |

0,5422 |

0,5454 |

|

m/j = |

14 |

7 |

4,6667 |

3,5 |

2,8 |

2,3333 |

Дисперсионный анализ

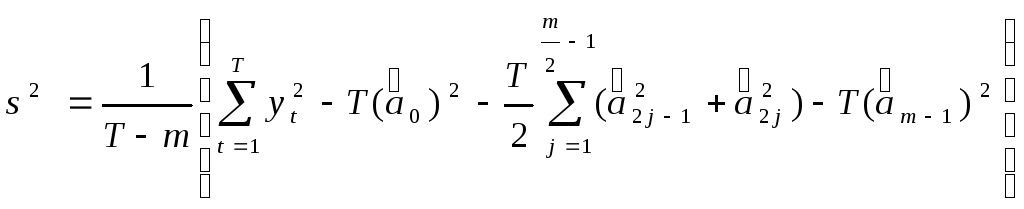

Оценим параметры построенного периодического тренда. Следует заметить, что параметры a0 и am-1 проверяются по критерию Стьюдента с (T-m) степенями свободы:

![]()

![]()

![]()

![]()

Коэффициенты a2j-1 и a2j проверяются на значимость парами (для каждого j) по критерию 2:

![]()

Расчеты приведены в Приложении № 8. В итоге получаем следующий вид периодического тренда:

![]()

З начимыми

оказались лишь гармоники 1 и 2

начимыми

оказались лишь гармоники 1 и 2

Теперь стоит проверить гипотезу о том, что тренд не содержит периодической составляющей. Для этого определяем расчетное значение F-статистики.

![]()

FP=1,393 Fтабл(0,05;13;28)=2,09

Так как FP < Fтабл , то гипотеза об отсутствии в тренде периодической составляющей принимается. Следовательно, при построении прогноза использовать построенную периодическую модель не следует строить прогноз будем только по трендовой модели.

Построение прогноза

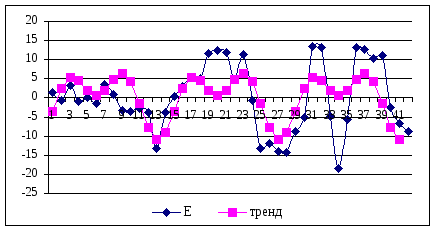

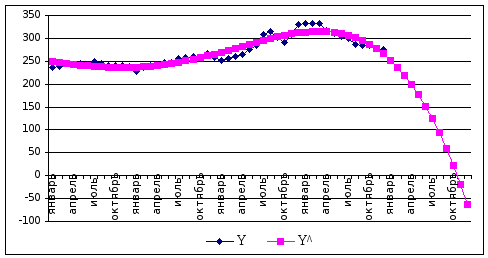

Перестроим лучший тренд по исходным 48-ми данным (см Приложение №9). В результате получим:

![]()

Теперь сделаем прогноз по этой модели на следующий 1977 год, т.е. на 12 периодов вперед (в реальности прогноз по трендовой модели на столь длинный период времени делать не следует). Расчет точечных прогнозных значений и доверительных интервалов смотрите в Приложении №9

Как видно из графика, построенная модель тренда достаточно хорошо описывает исходную статистику (R2 =89,13%). Однако прогноз полученный по этой модели явно искаженный. Это еще раз подтверждает сделанное выше замечание (по поводу величины прогнозного периода). Поэтому прогнозы по трендовой модели стоит строить не более, чем на три периода вперед. Также следует заметить, что в остатках имеется положительная автокорреляция (см. статистику Дарбина-Уотсона в Приложении №9), т.е. есть возможность построения авторегрессионной модели, что поможет более точно построить прогнозные значения.

Приложения

Приложение №1

Вариант №14

|

Период |

Год |

Месяц |

Y |

|

1 |

1973 |

январь |

236 |

|

2 |

февраль |

238 |

|

|

3 |

март |

245 |

|

|

4 |

апрель |

243 |

|

|

5 |

май |

245 |

|

|

6 |

июнь |

244 |

|

|

7 |

июль |

249 |

|

|

8 |

август |

246 |

|

|

9 |

сентябрь |

241 |

|

|

10 |

октябрь |

240 |

|

|

11 |

ноябрь |

240 |

|

|

12 |

декабрь |

238 |

|

|

13 |

1974 |

январь |

228 |

|

14 |

февраль |

237 |

|

|

15 |

март |

241 |

|

|

16 |

апрель |

244 |

|

|

17 |

май |

247 |

|

|

18 |

июнь |

248 |

|

|

19 |

июль |

256 |

|

|

20 |

август |

259 |

|

|

21 |

сентябрь |

261 |

|

|

22 |

октябрь |

257 |

|

|

23 |

ноябрь |

267 |

|

|

24 |

декабрь |

259 |

|

|

25 |

1975 |

январь |

251 |

|

26 |

февраль |

257 |

|

|

27 |

март |

260 |

|

|

28 |

апрель |

265 |

|

|

29 |

май |

276 |

|

|

30 |

июнь |

285 |

|

|

31 |

июль |

309 |

|

|

32 |

август |

314 |

|

|

33 |

сентябрь |

301 |

|

|

34 |

октябрь |

292 |

|

|

35 |

ноябрь |

309 |

|

|

36 |

декабрь |

331 |

|

|

37 |

1976 |

январь |

333 |

|

38 |

февраль |

332 |

|

|

39 |

март |

333 |

|

|

40 |

апрель |

318 |

|

|

41 |

май |

311 |

|

|

42 |

июнь |

304 |

|

|

43 |

июль |

299 |

|

|

44 |

август |

286 |

|

|

45 |

сентябрь |

285 |

|

|

46 |

октябрь |

284 |

|

|

47 |

ноябрь |

279 |

|

|

48 |

декабрь |

275 |

Приложение №2

STAT. T-test for Independent Samples (lab_2.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

252,0000* |

305,0588* |

-9,98358* |

46* |

,000000* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

31* |

17* |

16,31972* |

19,80363* |

1,472530* |

,350582* |

tтабл (0,05;46)=2,013

Fтабл(0,05;16;30)=1,99

Приложение №3

Regression Analysis - Linear model: Y = a + b*X

-----------------------------------------------------------------------------

Dependent variable: Y42

Independent variable: t

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 218,35 4,85021 45,0185 0,0000

Slope 2,34697 0,196514 11,9431 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 33988,9 1 33988,9 142,64 0,0000

Residual 9531,61 40 238,29

-----------------------------------------------------------------------------

Total (Corr.) 43520,5 41

Correlation Coefficient = 0,883734

R-squared = 78,0986 percent

Standard Error of Est. = 15,4366

Regression Analysis - Exponential model: Y = exp(a + b*X)

-----------------------------------------------------------------------------

Dependent variable: Y42

Independent variable: t

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 5,40466 0,0167025 323,585 0,0000

Slope 0,00848959 0,000676726 12,5451 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 0,444727 1 0,444727 157,38 0,0000

Residual 0,113033 40 0,00282583

-----------------------------------------------------------------------------

Total (Corr.) 0,55776 41

Correlation Coefficient = 0,892941

R-squared = 79,7344 percent

Standard Error of Est. = 0,0531585

Regression Analysis - Reciprocal-Y model: Y = 1/(a + b*X)

-----------------------------------------------------------------------------

Dependent variable: Y42

Independent variable: t

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 0,00443475 0,0000583415 76,0137 0,0000

Slope -0,0000309286 0,00000236379 -13,0843 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 0,00000590257 10,00000590257 171,20 0,0000

Residual 0,00000137911 40 3,44778E-8

-----------------------------------------------------------------------------

Total (Corr.) 0,00000728169 41

Correlation Coefficient = -0,900336

R-squared = 81,0605 percent

Standard Error of Est. = 0,000185682

Regression Analysis - Square root-X model: Y = a + b*sqrt(X)

-----------------------------------------------------------------------------

Dependent variable: Y42

Independent variable: t

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 191,089 9,19687 20,7776 0,0000

Slope 17,6924 1,98345 8,92005 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 28961,1 1 28961,1 79,57 0,0000

Residual 14559,3 40 363,983

-----------------------------------------------------------------------------

Total (Corr.) 43520,5 41

Correlation Coefficient = 0,815757

R-squared = 66,546 percent

Standard Error of Est. = 19,0783

Regression Analysis - Square root-Y model: Y = (a + b*X)^2

-----------------------------------------------------------------------------

Dependent variable: Y42

Independent variable: t

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 14,8511 0,142078 104,528 0,0000

Slope 0,0705143 0,00575652 12,2495 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 30,6813 1 30,6813 150,05 0,0000

Residual 8,17901 40 0,204475

-----------------------------------------------------------------------------

Total (Corr.) 38,8603 41

Correlation Coefficient = 0,888554

R-squared = 78,9528 percent

Standard Error of Est. = 0,452189

Polynomial Regression Analysis

-----------------------------------------------------------------------------

Dependent variable: Y42

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

CONSTANT 228,782 8,28757 27,6054 0,0000

t 6,45191 2,60344 2,47823 0,0179

t^2 -0,806261 0,242163 -3,32941 0,0020

t^3 0,0352464 0,00841485 4,18859 0,0002

t^4 -0,000442188 0,0000971212 -4,55295 0,0001

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 40356,6 4 10089,1 117,99 0,0000

Residual 3163,91 37 85,511

-----------------------------------------------------------------------------

Total (Corr.) 43520,5 41

R-squared = 92,7301 percent

R-squared (adjusted for d.f.) = 91,9441 percent

Standard Error of Est. = 9,24722

Mean absolute error = 7,07397

Durbin-Watson statistic = 0,747583

Приложение №4

|

t |

Y |

|

a+b*t |

exp(a+b*t) |

1/(a+b*t) |

полином 4 |

a+b*sqrt(t) |

|

1 |

236 |

|

220,70 |

224,34 |

227,08 |

234,46 |

208,78 |

|

2 |

238 |

|

223,04 |

226,25 |

228,68 |

238,74 |

216,11 |

|

3 |

245 |

|

225,39 |

228,18 |

230,31 |

241,80 |

221,73 |

|

4 |

243 |

|

227,74 |

230,12 |

231,96 |

243,83 |

226,47 |

|

5 |

245 |

|

230,08 |

232,09 |

233,64 |

245,01 |

230,65 |

|

6 |

244 |

|

232,43 |

234,06 |

235,34 |

245,51 |

234,43 |

|

7 |

249 |

|

234,78 |

236,06 |

237,07 |

245,47 |

237,90 |

|

8 |

246 |

|

237,13 |

238,07 |

238,82 |

245,03 |

241,13 |

|

9 |

241 |

|

239,47 |

240,10 |

240,59 |

244,34 |

244,17 |

|

10 |

240 |

|

241,82 |

242,15 |

242,40 |

243,50 |

247,04 |

|

11 |

240 |

|

244,17 |

244,21 |

244,23 |

242,63 |

249,77 |

|

12 |

238 |

|

246,51 |

246,30 |

246,09 |

241,84 |

252,38 |

|

13 |

228 |

|

248,86 |

248,40 |

247,97 |

241,21 |

254,88 |

|

14 |

237 |

|

251,21 |

250,51 |

249,89 |

240,81 |

257,29 |

|

15 |

241 |

|

253,55 |

252,65 |

251,84 |

240,72 |

259,61 |

|

16 |

244 |

|

255,90 |

254,80 |

253,81 |

241,00 |

261,86 |

|

17 |

247 |

|

258,25 |

256,98 |

255,82 |

241,69 |

264,04 |

|

18 |

248 |

|

260,60 |

259,17 |

257,86 |

242,83 |

266,15 |

|

19 |

256 |

|

262,94 |

261,38 |

259,94 |

244,44 |

268,21 |

|

20 |

259 |

|

265,29 |

263,61 |

262,04 |

246,54 |

270,21 |

|

21 |

261 |

|

267,64 |

265,85 |

264,18 |

249,13 |

272,17 |

|

22 |

257 |

|

269,98 |

268,12 |

266,36 |

252,21 |

274,07 |

|

23 |

267 |

|

272,33 |

270,40 |

268,57 |

255,76 |

275,94 |

|

24 |

259 |

|

274,68 |

272,71 |

270,82 |

259,76 |

277,76 |

|

25 |

251 |

|

277,02 |

275,04 |

273,11 |

264,16 |

279,55 |

|

26 |

257 |

|

279,37 |

277,38 |

275,44 |

268,92 |

281,30 |

|

27 |

260 |

|

281,72 |

279,75 |

277,80 |

273,98 |

283,02 |

|

28 |

265 |

|

284,07 |

282,13 |

280,21 |

279,26 |

284,71 |

|

29 |

276 |

|

286,41 |

284,54 |

282,66 |

284,70 |

286,37 |

|

30 |

285 |

|

288,76 |

286,96 |

285,15 |

290,18 |

287,99 |

|

31 |

309 |

|

291,11 |

289,41 |

287,69 |

295,63 |

289,60 |

|

32 |

314 |

|

293,45 |

291,88 |

290,27 |

300,92 |

291,17 |

|

33 |

301 |

|

295,80 |

294,36 |

292,90 |

305,93 |

292,72 |

|

34 |

292 |

|

298,15 |

296,87 |

295,58 |

310,52 |

294,25 |

|

35 |

309 |

|

300,49 |

299,40 |

298,31 |

314,56 |

295,76 |

|

36 |

331 |

|

302,84 |

301,96 |

301,09 |

317,89 |

297,24 |

|

37 |

333 |

|

305,19 |

304,53 |

303,92 |

320,34 |

298,71 |

|

38 |

332 |

|

307,53 |

307,13 |

306,80 |

321,73 |

300,15 |

|

39 |

333 |

|

309,88 |

309,75 |

309,74 |

321,89 |

301,58 |

|

40 |

318 |

|

312,23 |

312,39 |

312,73 |

320,61 |

302,99 |

|

41 |

311 |

|

314,58 |

315,05 |

315,79 |

317,69 |

304,38 |

|

42 |

304 |

|

316,92 |

317,74 |

318,90 |

312,90 |

305,75 |

|

43 |

299 |

|

319,27 |

320,45 |

322,08 |

306,02 |

307,11 |

|

44 |

286 |

|

321,62 |

323,18 |

325,32 |

296,81 |

308,45 |

|

45 |

285 |

|

323,96 |

325,93 |

328,63 |

285,02 |

309,77 |

|

46 |

284 |

|

326,31 |

328,71 |

332,00 |

270,39 |

311,08 |

|

47 |

279 |

|

328,66 |

331,51 |

335,45 |

252,64 |

312,38 |

|

48 |

275 |

|

331,00 |

334,34 |

338,96 |

231,50 |

313,67 |

|

|

|

Кт = |

0,148 |

0,156 |

0,167 |

0,078 |

0,096 |

Приложение №5

Periodogram for RESID

Cumulative Integrated

Frequency Period Ordinate Sum Periodogram

--------------------------------------------------------------------------------

0,0 0,0 0,0 0,0

0,0238095 42,0 4,22049 4,22049 0,00133395

0,047619 21,0 578,705 582,926 0,184243

0,0714286 14,0 703,654 1286,58 0,406643

0,0952381 10,5 140,974 1427,55 0,4512

0,119048 8,4 328,142 1755,7 0,554914

0,142857 7,0 538,896 2294,59 0,72524

0,166667 6,0 204,965 2499,56 0,790023

0,190476 5,25 126,583 2626,14 0,830031

0,214286 4,66667 38,7352 2664,88 0,842274

0,238095 4,2 225,646 2890,52 0,913593

0,261905 3,81818 70,3745 2960,9 0,935836

0,285714 3,5 40,22 3001,12 0,948548

0,309524 3,23077 27,9011 3029,02 0,957366

0,333333 3,0 30,4306 3059,45 0,966984

0,357143 2,8 11,3861 3070,83 0,970583

0,380952 2,625 7,06397 3077,9 0,972816

0,404762 2,47059 22,7291 3100,63 0,98

0,428571 2,33333 11,4533 3112,08 0,98362

0,452381 2,21053 27,059 3139,14 0,992172

0,47619 2,1 7,40308 3146,54 0,994512

0,5 2,0 17,3635 3163,91 1,0

The StatAdvisor

---------------

This table shows the periodogram ordinates for RESID. It is often

used to identify cycles of fixed frequency in the data. The

periodogram is constructed by fitting a series of sine functions at

each of 22 frequencies. The ordinates are equal to the squared

amplitudes of the sine functions. The periodogram can be thought of

as an analysis of variance by frequency, since the sum of the

ordinates equals the total corrected sum of squares in an ANOVA table.

You can plot the periodogram ordinates by selecting Periodogram from

the list of Graphical Options.

Приложение №6

|

Период |

|

|

k |

Ck |

|

cos |

j |

Uj |

|

1 |

1,54 |

|

0 |

87,89 |

1,000 |

## |

0 |

45,700 |

|

2 |

-0,74 |

|

1 |

53,90 |

0,972 |

## |

1 |

54,131 |

|

3 |

3,20 |

|

2 |

9,62 |

0,895 |

## |

2 |

63,822 |

|

4 |

-0,83 |

|

3 |

-13,71 |

0,784 |

## |

3 |

62,546 |

|

5 |

-0,01 |

|

4 |

-17,70 |

0,650 |

## |

4 |

56,2904 |

|

6 |

-1,51 |

|

5 |

-18,82 |

0,508 |

## |

5 |

47,474 |

|

7 |

3,53 |

|

6 |

-18,03 |

0,370 |

## |

6 |

40,397 |

|

8 |

0,97 |

|

7 |

-11,37 |

0,250 |

## |

7 |

36,935 |

|

9 |

-3,34 |

|

8 |

-11,66 |

0,157 |

## |

8 |

33,367 |

|

10 |

-3,50 |

|

9 |

-22,39 |

0,091 |

## |

9 |

30,386 |

|

11 |

-2,63 |

|

10 |

-32,40 |

0,047 |

## |

10 |

29,229 |

|

12 |

-3,84 |

|

11 |

-24,57 |

0,020 |

## |

11 |

28,979 |

|

13 |

-13,21 |

|

12 |

-4,51 |

0,006 |

## |

12 |

28,957 |

|

14 |

-3,81 |

|

13 |

4,98 |

0,001 |

## |

13 |

28,813 |

|

15 |

0,28 |

|

14 |

10,90 |

0,000 |

## |

14 |

28,701 |

|

16 |

3,00 |

|

|

|

|

|

|

|

|

17 |

5,31 |

|

|

|

|

|

|

|

|

18 |

5,17 |

|

|

|

|

|

|

|

|

19 |

11,56 |

|

|

|

|

|

|

|

|

20 |

12,46 |

|

|

|

|

|

|

|

|

21 |

11,87 |

|

|

|

|

|

|

|

|

22 |

4,79 |

|

|

|

|

|

|

|

|

23 |

11,24 |

|

|

|

|

|

|

|

|

24 |

-0,76 |

|

|

|

|

|

|

|

|

25 |

-13,16 |

|

|

|

|

|

|

|

|

26 |

-11,92 |

|

|

|

|

|

|

|

|

27 |

-13,98 |

|

|

|

|

|

|

|

|

28 |

-14,26 |

|

|

|

|

|

|

|

|

29 |

-8,70 |

|

|

|

|

|

|

|

|

30 |

-5,18 |

|

|

|

|

|

|

|

|

31 |

13,37 |

|

|

|

|

|

|

|

|

32 |

13,08 |

|

|

|

|

|

|

|

|

33 |

-4,93 |

|

|

|

|

|

|

|

|

34 |

-18,52 |

|

|

|

|

|

|

|

|

35 |

-5,56 |

|

|

|

|

|

|

|

|

36 |

13,11 |

|

|

|

|

|

|

|

|

37 |

12,66 |

|

|

|

|

|

|

|

|

38 |

10,27 |

|

|

|

|

|

|

|

|

39 |

11,11 |

|

|

|

|

|

|

|

|

40 |

-2,61 |

|

|

|

|

|

|

|

|

41 |

-6,69 |

|

|

|

|

|

|

|

|

42 |

-8,90 |

|

|

|

|

|

|

|

Приложение №7

Multiple Regression Analysis

-----------------------------------------------------------------------------

Dependent variable: RESID

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

CONSTANT -0,00081512 1,23793 -0,000658452 0,9995

a1 -5,49196 1,75087 -3,1367 0,0040

a2 1,83036 1,75045 1,04565 0,3047

a3 -3,49596 1,75087 -1,9967 0,0557

a4 3,66606 1,75045 2,09435 0,0454

a5 -0,0392238 1,75087 -0,0224024 0,9823

a6 -1,35751 1,75045 -0,775522 0,4445

a7 0,450862 1,75087 0,257507 0,7987

a8 1,30846 1,75045 0,747498 0,4610

a9 0,0403022 1,75087 0,0230184 0,9818

a10 0,735162 1,75045 0,419984 0,6777

a11 0,192437 1,75087 0,109909 0,9133

a12 0,712703 1,75045 0,407154 0,6870

a13 -0,644543 1,23793 -0,52066 0,6067

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 1361,71 13 104,747 1,63 0,1363

Residual 1802,2 28 64,3642

-----------------------------------------------------------------------------

Total (Corr.) 3163,91 41

R-squared = 43,0388 percent

R-squared (adjusted for d.f.) = 16,5926 percent

Standard Error of Est. = 8,02273

Mean absolute error = 5,32326

Durbin-Watson statistic = 0,891393

Приложение №8

|

t |

|

|

|

|

|

tрасч |

tтабл |

P-value |

|

1 |

1,54 |

|

|

a0 |

-0,001 |

0,00 |

2,05 |

1,00 |

|

2 |

-0,74 |

|

|

a13 |

-0,64 |

-0,52 |

2,05 |

0,61 |

|

3 |

3,20 |

|

j |

|

Rj^2 |

Хи:2 |

Хи:2 табл |

P-value |

|

4 |

-0,83 |

|

1 |

a1+a2 |

33,51 |

10,93 |

5,99 |

0,00 |

|

5 |

-0,01 |

|

2 |

a3+a4 |

25,66 |

8,37 |

5,99 |

0,02 |

|

6 |

-1,51 |

|

3 |

a5+a6 |

1,84 |

0,60 |

5,99 |

0,74 |

|

7 |

3,53 |

|

4 |

a7+a8 |

1,92 |

0,62 |

5,99 |

0,73 |

|

8 |

0,97 |

|

5 |

a9+a10 |

0,54 |

0,18 |

5,99 |

0,92 |

|

9 |

-3,34 |

|

6 |

a11+a12 |

0,55 |

0,18 |

5,99 |

0,91 |

|

10 |

-3,50 |

|

|

|

|

|

|

|

|

11 |

-2,63 |

|

|

s^2 = |

64,3617 |

|

|

|

|

12 |

-3,84 |

|

|

|

|

|

|

|

|

13 |

-13,21 |

|

|

|

|

|

|

|

|

14 |

-3,81 |

|

j |

|

Rj^2 |

Хи:2 |

Хи:2 табл |

P-value |

|

15 |

0,28 |

|

1 |

a1+a2 |

33,51 |

10,26 |

5,99 |

0,01 |

|

16 |

3,00 |

|

2 |

a3+a4 |

25,66 |

7,85 |

5,99 |

0,02 |

|

17 |

5,31 |

|

|

|

|

|

|

|

|

18 |

5,17 |

|

|

s^2 = |

68,6173 |

|

|

|

|

19 |

11,56 |

|

|

|

|

|

|

|

|

20 |

12,46 |

|

|

|

|

|

|

|

|

21 |

11,87 |

|

|

|

Вывод: гармоники j=1,2 значимы |

|

||

|

22 |

4,79 |

|

|

|

|

|

|

|

|

23 |

11,24 |

|

|

|

|

|

|

|

|

24 |

-0,76 |

|

|

|

|

|

|

|

|

25 |

-13,16 |

|

Fр = |

1,39303 |

|

F(0,05;13;28) = |

2,08893 |

|

|

26 |

-11,92 |

|

|

|

|

|

|

|

|

27 |

-13,98 |

|

|

|

|

|

|

|

|

28 |

-14,26 |

|

|

|

|

|

|

|

|

29 |

-8,70 |

|

|

|

|

|

|

|

|

30 |

-5,18 |

|

|

|

|

|

|

|

|

31 |

13,37 |

|

|

|

|

|

|

|

|

32 |

13,08 |

|

|

|

|

|

|

|

|

33 |

-4,93 |

|

|

|

|

|

|

|

|

34 |

-18,52 |

|

|

|

|

|

|

|

|

35 |

-5,56 |

|

|

|

|

|

|

|

|

36 |

13,11 |

|

|

|

|

|

|

|

|

37 |

12,66 |

|

|

|

|

|

|

|

|

38 |

10,27 |

|

|

|

|

|

|

|

|

39 |

11,11 |

|

|

|

|

|

|

|

|

40 |

-2,61 |

|

|

|

|

|

|

|

|

41 |

-6,69 |

|

|

|

|

|

|

|

|

42 |

-8,90 |

|

|

|

|

|

|

|

Приложение №9

Multiple Regression Analysis

-----------------------------------------------------------------------------

Dependent variable: Y48

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

CONSTANT 235,622 8,15259 28,9015 0,0000

t 3,41011 2,25467 1,51247 0,1377

t2 -0,48587 0,184415 -2,63465 0,0117

t3 0,023581 0,00562733 4,19044 0,0001

t4 -0,000306782 0,0000569923 -5,38286 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 40945,6 4 10236,4 104,10 0,0000

Residual 4228,29 43 98,3323

-----------------------------------------------------------------------------

Total (Corr.) 45173,9 47

R-squared = 90,64 percent

R-squared (adjusted for d.f.) = 89,7693 percent

Standard Error of Est. = 9,91627

Mean absolute error = 7,4022

Durbin-Watson statistic = 0,65469

Multiple Regression Analysis

-----------------------------------------------------------------------------

Dependent variable: Y48

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

CONSTANT 252,514 5,36506 47,0663 0,0000

t -2,36238 0,566854 -4,16752 0,0001

t3 0,00894824 0,0009649 9,27375 0,0000

t4 -0,000162524 0,0000168487 -9,64607 0,0000

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 40263,1 3 13421,0 120,25 0,0000

Residual 4910,85 44 111,61

-----------------------------------------------------------------------------

Total (Corr.) 45173,9 47

R-squared = 89,129 percent

R-squared (adjusted for d.f.) = 88,3878 percent

Standard Error of Est. = 10,5646

Mean absolute error = 8,14179

Durbin-Watson statistic = 0,5614

Regression Results for Y48

------------------------------------------------------------------------------------------------------

Fitted Stnd. Error Lower 95,0% CL Upper 95,0% CL Lower 95,0% CL Upper 95,0% CL

Row Value for Forecast for Forecast for Forecast for Mean for Mean

------------------------------------------------------------------------------------------------------

49 252,592 12,9741 226,444 278,739 237,414 267,77

50 237,152 13,9543 209,029 265,275 218,778 255,525

51 219,52 15,2127 188,861 250,179 197,46 241,58

52 199,553 16,7727 165,75 233,357 173,298 225,808

53 177,105 18,6517 139,515 214,695 146,126 208,084

54 152,023 20,8625 109,977 194,069 115,767 188,279

55 124,153 23,4153 76,9624 171,344 82,0386 166,267

56 93,336 26,3194 40,2927 146,379 44,7534 141,919

57 59,4093 29,5842 -0,213884 119,033 3,71734 115,101

58 22,2061 33,22 -44,7446 89,1568 -41,2688 85,681

59 -18,4442 37,2382 -93,4931 56,6046 -90,4095 53,521

60 -62,7162 41,6514 -146,659 21,2268 -143,914 18,4817

------------------------------------------------------------------------------------------------------