vk.com/id446425943

African Rainbow Minerals – BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 90: African Rainbow Minerals, ZARmn (unless otherwise stated)

|

|

|

|

African Rainbow Minerals |

ARIJ.J |

Target price, ZAR: |

150 |

Market capitalisation, ZARmn: |

29,947 |

Last price, ZAR: |

136 |

Enterprise value, ZARmn: |

31,146 |

Potential 12-month return: |

20.5% |

Jun-YE |

2017 |

2018 |

2019E |

2020E |

2021E |

Income statement |

|

|

|

|

|

Revenue |

8,158 |

8,346 |

9,745 |

10,188 |

10,771 |

Underlying EBITDA |

922 |

1,799 |

2,653 |

2,664 |

2,894 |

Underlying EBIT |

214 |

1,058 |

1,802 |

1,789 |

1,858 |

Net interest |

-185 |

-183 |

135 |

326 |

425 |

Equity accounted income |

3,446 |

4,129 |

4,159 |

2,471 |

2,108 |

Taxation |

409 |

-573 |

-543 |

-592 |

-639 |

Other |

-2,512 |

131 |

-451 |

-478 |

-409 |

Net profit for the year |

1,372 |

4,562 |

5,103 |

3,516 |

3,342 |

Headline earnings |

3,215 |

4,851 |

5,103 |

3,516 |

3,342 |

HEPS, ZAc |

1,684 |

2,526 |

2,670 |

1,840 |

1,749 |

Thomson Reuters consensus EPS, ZAc |

|

|

2,406 |

1,987 |

2,129 |

DPS declared, ZAc |

650 |

1,000 |

1,400 |

1,350 |

1,290 |

Underlying EBIT |

832 |

1,026 |

1,563 |

1,666 |

1,422 |

Platinum |

|||||

EBIT margin |

16% |

18% |

24% |

24% |

20% |

Nkomati |

120 |

18 |

-42 |

-31 |

400 |

EBIT margin |

6% |

1% |

-2% |

-2% |

17% |

Goedgevonden |

78 |

408 |

579 |

466 |

365 |

EBIT margin |

9% |

40% |

40% |

33% |

27% |

Other |

-816 |

-394 |

-298 |

-312 |

-329 |

Underlying EBIT |

214 |

1,058 |

1,802 |

1,789 |

1,858 |

Income statement ratios* |

|

|

|

|

|

EBITDA margin |

31% |

34% |

37% |

30% |

28% |

EBIT margin |

3% |

13% |

18% |

18% |

17% |

HEPS growth |

241% |

50% |

6% |

-31% |

-5% |

Dividend payout ratio |

39% |

40% |

52% |

73% |

74% |

Input assumptions |

|

|

|

|

|

$/ZAR |

13.60 |

12.85 |

14.25 |

14.25 |

14.09 |

Platinum, $/oz |

988 |

940 |

820 |

970 |

1,134 |

Iron ore (62%Fe, CIF China), $/t |

69 |

67 |

65 |

61 |

62 |

Manganese ore (44%, CIF China), $/mtu |

5.72 |

6.79 |

6.32 |

5.24 |

5.41 |

Nickel, $/t |

10,134 |

12,474 |

11,593 |

13,176 |

14,541 |

Required breakeven price |

|

|

|

|

|

3PGMs, $/3PGM oz |

811 |

860 |

872 |

932 |

986 |

Nickel, $/t |

9,132 |

12,384 |

12,444 |

13,749 |

11,308 |

Iron ore, $/t |

37 |

46 |

44 |

50 |

53 |

Manganese ore, $/mtu |

3.84 |

4.71 |

5.05 |

4.32 |

4.47 |

Export thermal coal, $/t |

62 |

65 |

65 |

66 |

67 |

Sales volumes |

|

|

|

|

|

PGMs in concentrate - attributable, k oz |

324 |

316 |

316 |

316 |

316 |

Iron ore, kt |

8,638 |

8,937 |

8,700 |

8,700 |

8,700 |

Manganese ore, kt |

1,487 |

1,589 |

1,550 |

1,550 |

1,860 |

Nickel, t |

7,938 |

6,651 |

6,825 |

6,825 |

7,875 |

Attributable Cu eq volumes, kt |

296 |

297 |

284 |

284 |

297 |

Volume growth |

-1.2% |

0.3% |

-4.4% |

0.0% |

4.5% |

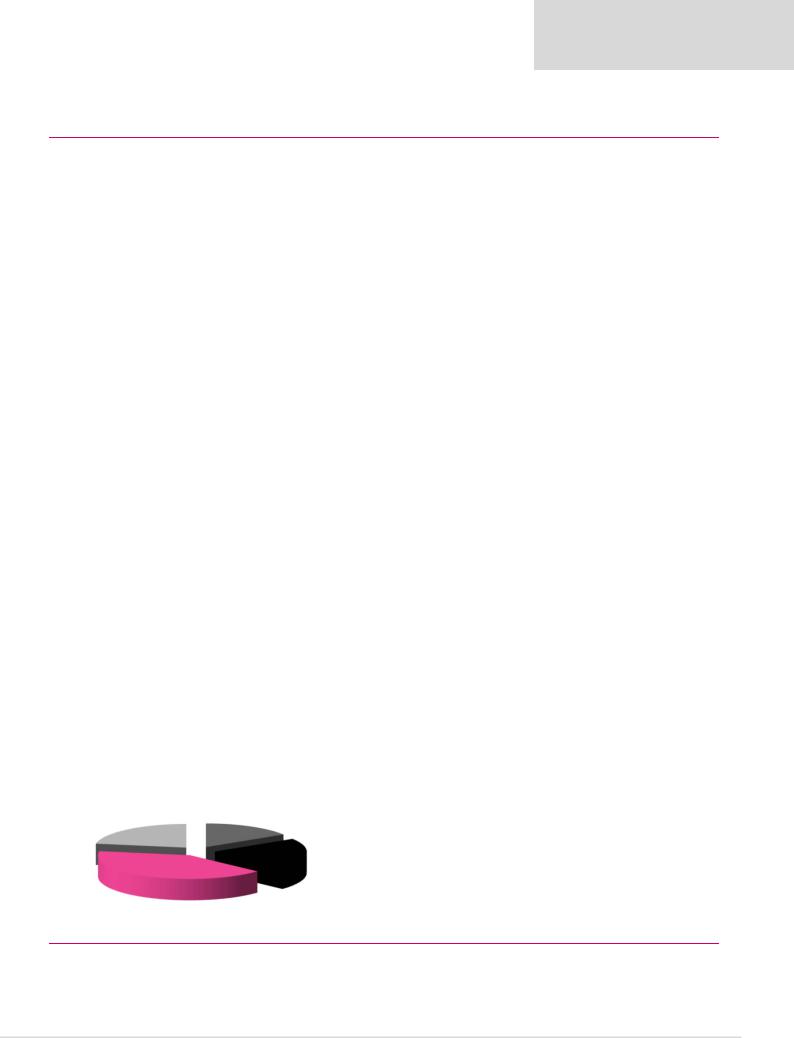

Contribution to FY19E attributable underlying EBITDA

|

Platinum |

Coal |

13% |

22% |

Nickel |

|

|

|

1% |

Iron ore Manganese 31%

33%

Jun-YE |

|

|

|

2019E |

2020E |

2021E |

|

2017 |

2018 |

|

|

||||

Balance sheet |

|

|

|

|

|

|

|

Net operating assets |

23,738 |

24,822 |

|

24,708 |

23,805 |

23,224 |

|

Investments |

1,573 |

1,561 |

|

1,772 |

1,772 |

1,772 |

|

Equity |

23,497 |

25,907 |

|

28,009 |

28,627 |

29,257 |

|

Minority interest |

543 |

1,471 |

|

1,561 |

1,657 |

1,739 |

|

Net debt (cash) |

1,271 |

-995 |

|

-3,090 |

-4,707 |

-6,000 |

|

Balance sheet ratios |

|

|

|

|

|

|

|

Gearing* |

5.1% |

-4.0% |

|

-12.4% |

-19.7% |

-25.8% |

|

Net debt to EBITDA plus equity income |

0.3x |

-0.2x |

|

-0.5x |

-0.9x |

-1.2x |

|

RoCE (excluding Harmony) |

19.9% |

23.5% |

|

28.3% |

19.9% |

18.8% |

|

RoIC |

15.9% |

22.1% |

|

27.4% |

18.5% |

16.9% |

|

RoE |

13.5% |

19.5% |

|

18.9% |

12.4% |

11.5% |

|

*net debt/(net debt+equity) |

|

|

|

|

|

|

|

Cash flow statement |

|

|

|

|

|

|

|

Operating cash flow |

2,312 |

3,914 |

|

6,833 |

5,893 |

5,171 |

|

Capex (net of disposals) |

-981 |

-944 |

|

-1,282 |

-1,251 |

-1,163 |

|

Other cash flows |

2,030 |

1,179 |

|

0 |

0 |

0 |

|

FCF |

3,361 |

4,149 |

|

5,551 |

4,643 |

4,007 |

|

Equity shareholders' cash |

3,390 |

3,980 |

|

5,096 |

4,515 |

4,005 |

|

Dividends and share buy-backs |

-426 |

-1,714 |

|

-3,001 |

|

-2,898 |

-2,712 |

Movement in net debt |

2,964 |

2,266 |

|

2,095 |

1,617 |

1,294 |

|

Cash flow ratios |

|

|

|

|

|

|

|

Working capital days |

66 |

88 |

|

69 |

67 |

67 |

|

Capex/EBITDA |

106.4% |

52.5% |

|

48.3% |

47.0% |

40.2% |

|

Cash conversion |

1.1x |

0.8x |

|

1.0x |

1.3x |

1.2x |

|

FCF yield |

16.8% |

19.1% |

|

22.7% |

20.3% |

18.5% |

|

Equity shareholders' yield |

18.7% |

18.7% |

|

19.6% |

17.4% |

15.4% |

|

Valuation |

|

|

|

|

|

|

|

SoTP DCF valuation and calculation of target price |

|

ZARmn |

ZAR/sh |

|

|||

Iron ore |

|

|

|

|

7,406 |

35.8 |

|

Manganese |

|

|

|

|

9,987 |

48.2 |

|

Two Rivers (effective interest = 54%) |

|

|

|

|

2,576 |

12.4 |

|

Modikwa (41.5%) |

|

|

|

|

916 |

4.4 |

|

Nkomati |

|

|

|

|

1,700 |

8.2 |

|

PCB Coal less debt (effective interest = 20.2%) |

|

|

|

1,949 |

9.4 |

|

|

Goedgevonden (effective interest = 26%) |

|

|

|

|

2,228 |

10.8 |

|

Copper and exploration |

|

|

|

|

0 |

0.0 |

|

Harmony at listed market value |

|

|

|

|

2,089 |

10.1 |

|

Corporate and other |

|

|

|

|

-1,522 |

-7.4 |

|

Enterprise value |

|

|

|

|

27,329 |

132.0 |

|

Net cash and other |

|

|

|

|

1,795 |

8.7 |

|

Equity value |

|

|

|

|

29,124 |

140.7 |

|

Plus: equity shareholders' cash/share |

|

|

|

|

|

25.1 |

|

Less: DPS |

|

|

|

|

|

-13.7 |

|

TP, rounded to |

|

|

|

|

|

150.0 |

|

Share price on 7/1/2019 |

|

|

|

|

|

135.8 |

|

Expected share price return |

|

|

|

|

|

10.4% |

|

Plus: expected dividend yield |

|

|

|

|

|

10.1% |

|

Total implied one-year return |

|

|

|

|

|

20.5% |

|

Share price range, ZAR: |

|

|

|

|

|

|

|

12-month high on 31/12/2018 |

144 |

12-month low on 4/4/2018 |

90 |

|

|||

Price move since high |

-5.9% |

Price move since low |

|

50.5% |

|

||

Calculation of discount rate |

|

|

|

|

|

|

|

WACC |

16.2% |

Cost of debt |

|

|

10.0% |

|

|

Risk-free rate |

9.0% |

Tax rate |

|

|

28% |

|

|

Equity risk premium |

5.5% |

After-tax cost of debt |

|

7.2% |

|

||

Beta |

1.30 |

Debt weighting |

|

0% |

|

||

Cost of equity |

16.2% |

Terminal growth rate |

|

2.0% |

|

||

Valuation ratios |

|

|

|

|

|

|

|

Jun-YE |

2017 |

2018 |

|

2019E |

2020E |

2021E |

|

P/E multiple |

5.7x |

4.4x |

|

5.1x |

7.4x |

7.8x |

|

Dividend yield |

6.8% |

9.0% |

|

10.3% |

9.9% |

9.5% |

|

EV/EBITDA |

4.6x |

3.7x |

|

3.6x |

4.5x |

4.3x |

|

P/B |

0.8x |

0.8x |

|

0.9x |

0.9x |

0.9x |

|

NAV per share, ZAR |

124 |

136 |

|

147 |

150 |

153 |

|

* Proportionately consolidated

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

55

vk.com/id446425943

Alrosa – BUY

Renaissance Capital

14 January 2019

Metals & Mining

Figure 91: Alrosa, RUBmn (unless otherwise stated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Alrosa |

|

ALRS.MM |

|

|

|

|

|

Target price, RUB: |

|

|

109.0 |

|

||

Market capitalisation, RUBmn: |

|

736,555 |

|

|

|

|

|

Share price, RUB: |

|

|

101.6 |

|

||

Enterprise value, RUBmn: |

|

837,502 |

|

|

|

|

|

Potential 12-month return: |

|

20.1% |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dec-YE |

2016 |

2017 |

2018E |

2019E |

2020E |

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

||

Income statement |

|

|

|

|

|

|

Balance sheet ratios |

|

|

|

|

|

|

|

Revenue |

317,090 |

275,381 |

302,368 |

336,787 |

355,901 |

|

Gearing (net debt/(net debt+equity) |

24.5% |

24.4% |

|

18.7% |

16.4% |

13.8% |

|

Adjusted EBITDA |

176,418 |

126,890 |

162,410 |

172,162 |

181,928 |

|

Net debt/(EBITDA+dividends from associat |

0.5x |

0.7x |

|

0.3x |

0.3x |

0.2x |

|

Adjusted EBIT |

151,750 |

103,098 |

139,183 |

146,384 |

155,918 |

|

RoCE |

40.0% |

27.4% |

|

39.2% |

42.9% |

44.2% |

|

EBIT |

142,965 |

99,083 |

140,265 |

146,384 |

155,918 |

|

RoIC (after tax) |

35.8% |

17.6% |

|

30.0% |

33.5% |

34.6% |

|

Net interest |

24,124 |

-1,320 |

-12,662 |

-8,870 |

-11,013 |

|

RoE |

65.3% |

30.0% |

|

42.2% |

48.0% |

48.6% |

|

Taxation |

-36,268 |

-22,174 |

-27,740 -30,253 -31,879 |

|

Cash flow statement |

|

|

|

|

|

|

|

||

Equity accounted income |

2,650 |

3,027 |

3,681 |

3,665 |

3,795 |

|

|

|

|

|

|

|

|

|

Net profit for the year |

133,471 |

78,616 |

103,544 |

110,925 |

116,821 |

|

Operating cash flow |

143,138 |

100,464 |

|

146,925 |

130,108 |

145,843 |

|

Minority interest in profit |

-2,079 |

-1,541 |

-2,086 |

-2,219 |

-2,336 |

|

Capex |

-31,752 |

-26,944 |

|

-31,600 |

-26,400 |

-28,000 |

|

Attributable net profit |

131,392 |

77,075 |

101,457 |

108,707 |

114,484 |

|

Other FCF |

0 |

0 |

|

30,801 |

0 |

0 |

|

|

|

|

|

|

|

|

FCF |

111,386 |

73,520 |

|

146,126 |

103,708 |

117,843 |

|

EPS, RUB |

17.85 |

10.47 |

14.12 |

15.08 |

15.88 |

|

Equity shareholders' cash |

134,076 |

63,014 |

|

129,410 |

94,970 |

107,371 |

|

|

Dividends and share buy backs |

-14,775 |

-65,706 |

|

-94,823 |

-90,247 |

-99,429 |

|

||||||

Thomson Reuters consensus EPS, RUB |

|

|

14.72 |

15.89 |

16.05 |

|

Surplus (deficit) cash |

119,301 |

-2,692 |

|

34,588 |

4,723 |

7,942 |

|

DPS declared, RUB |

2.09 |

8.93 |

16.40 |

12.95 |

15.53 |

|

Cash flow ratios |

|

|

|

|

|

|

|

Adjusted EBIT |

|

-0.41345 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Working capital days |

104 |

145 |

|

112 |

115 |

115 |

|

|

Diamonds |

205,235 |

132,879 |

171,624 |

187,647 |

199,173 |

|

Cash conversion |

1.0x |

0.8x |

|

1.3x |

0.9x |

0.9x |

|

Transportation |

933 |

1,298 |

1,869 |

856 |

904 |

|

FCF yield |

17.3% |

10.1% |

|

19.9% |

13.3% |

15.3% |

|

Social infrastructure |

-5,559 |

-3,537 |

-3,409 |

-4,977 |

-5,259 |

|

Equity shareholders' yield |

23.9% |

9.8% |

|

18.9% |

13.0% |

14.7% |

|

Other (SG&A, other expenses) |

-48,859 |

-27,542 |

-30,901 |

-37,142 |

-38,899 |

|

Capex/Adjusted EBITDA |

18.0% |

21.2% |

|

19.5% |

15.3% |

15.4% |

|

Income statement ratios |

|

|

|

|

|

|

Valuation |

|

|

|

|

|

|

|

EBITDA margin |

56% |

46% |

54% |

51% |

51% |

|

SoTP DCF valuation and calculation of target price |

|

|

|

RUBmn |

RUB/sh |

||

EBIT margin |

45% |

36% |

46% |

43% |

44% |

|

Diamonds |

|

|

|

|

993,344 |

137.8 |

|

EPS growth |

328% |

-41% |

35% |

7% |

5% |

|

Transportation |

|

|

|

|

6,604 |

0.9 |

|

Payout ratio |

12% |

85% |

116% |

86% |

98% |

|

Other |

|

|

|

|

-127,648 |

-17.7 |

|

Input assumptions |

|

|

|

|

|

|

Total enterprise value |

|

|

|

|

872,300 |

121.0 |

|

|

|

|

|

|

|

Net debt as at 31 December 2017 |

|

|

|

|

-86,047 |

-11.9 |

|

|

Rough diamond index, $/c |

197 |

198 |

202 |

202 |

208 |

|

Cash used in share buy-backs |

|

|

|

|

14,077 |

2.0 |

|

Alrosa average gem realisations, $/ct |

150.1 |

135.4 |

160.3 |

157.1 |

162.3 |

|

Other investments |

|

|

|

|

0 |

0.0 |

|

Gem realisations vs. index prices |

76% |

68% |

80% |

78% |

78% |

|

Minority interest |

|

|

|

|

-14,900 |

-2.1 |

|

Alrosa average industrial realisations, $/ct |

8.5 |

7.6 |

9.7 |

10.4 |

10.8 |

|

Equity value as at 8/1/2019 |

|

|

|

|

785,430 |

109.0 |

|

Alrosa average realisations, $/ct |

110.8 |

101.0 |

118.3 |

113.1 |

116.9 |

|

|

|

|

|

|

|

|

|

Rounded to |

|

|

|

|

|

109.0 |

|

|||||||

RUB/$ |

67 |

58 |

63 |

67 |

68 |

|

Share price on 7/1/2019 |

|

|

|

|

|

101.6 |

|

All in cash costs, net of by-products |

|

|

|

|

|

|

Expected share price return |

|

|

|

|

|

7.3% |

|

|

|

|

|

|

|

Plus: expected dividend yield |

|

|

|

|

|

12.8% |

|

|

Estimated required breakeven price, $/c |

128 |

148 |

131 |

138 |

142 |

|

Total implied one-year return |

|

|

|

|

|

20.1% |

|

Production volumes, kct |

|

|

|

|

|

|

Share price range, RUB: |

|

|

|

|

|

|

|

Diamonds |

|

|

|

|

|

|

12-month high on 1/10/2018 |

107.9 |

12-month low on 12/1/2018 |

75.1 |

|

|||

Aikhal division |

12,228 |

13,010 |

11,300 |

8,962 |

8,539 |

|

Price move since high |

-5.9% |

Price move since low |

|

35.2% |

|

||

Mirny division |

7,808 |

7,231 |

4,415 |

3,692 |

3,691 |

|

|

|

|

|

|

|

|

|

Udachny division |

3,167 |

3,821 |

5,288 |

8325 |

8343 |

|

Calculation of discount rate |

|

|

|

|

|

|

|

Nyurba division |

6,793 |

7,713 |

7,351 |

7,321 |

7,382 |

|

|

|

|

|

|

|

|

|

Severalmaz |

2,217 |

2,642 |

3,320 |

3,823 |

4,198 |

|

WACC |

14.0% |

Cost of debt |

|

|

8.5% |

|

|

Almazy Anabara & Nizhne-Lenskoye |

5,145 |

5,197 |

4,977 |

4,973 |

4,999 |

|

Risk-free rate |

7.0% |

Tax rate |

|

|

20% |

|

|

Other production |

0 |

0 |

-5 |

0 |

0 |

|

Equity risk premium |

6.0% |

After-tax cost of debt |

|

6.8% |

|

||

Total |

37,358 |

39,614 |

36,646 |

37,096 |

37,152 |

|

Beta |

1.30 |

Debt weighting |

|

10% |

|

||

Sales volumes , kct |

|

|

|

|

|

|

Cost of equity |

14.8% |

Terminal growth rate |

|

4.0% |

|

||

|

|

|

|

|

|

Valuation ratios |

|

|

|

|

|

|

|

|

Gem-quality |

28,900 |

30,100 |

26,700 |

27,856 |

28,068 |

|

|

|

|

|

|

|

|

|

Industrial |

11,100 |

11,100 |

10,300 |

11,938 |

12,029 |

|

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

|

Total |

40,000 |

41,200 |

37,000 |

39,794 |

40,097 |

|

P/E multiple |

4.3x |

8.3x |

|

6.7x |

6.7x |

6.4x |

|

Balance sheet |

|

|

|

|

|

|

Dividend yield |

2.7% |

10.3% |

|

17.5% |

12.7% |

15.3% |

|

|

|

|

|

|

|

EV/(EBITDA+Equity income) |

3.6x |

5.6x |

|

4.4x |

4.4x |

4.1x |

||

Net operating assets |

340,325 |

352,534 |

273,784 |

284,653 |

279,478 |

|

P/B |

2.2x |

2.4x |

|

3.1x |

3.1x |

3.0x |

|

Equity |

257,202 |

266,825 |

223,576 |

238,945 |

241,479 |

|

NAV per share, USc |

52.1 |

62.1 |

|

48.9 |

49.5 |

49.3 |

|

Minority interest |

-232 |

-338 |

-1,250 |

-1,029 |

-795 |

|

NAV per share, RUB |

34.9 |

36.2 |

|

30.7 |

33.1 |

33.5 |

|

Net debt |

83,355 |

86,047 |

51,459 |

46,736 |

38,794 |

|

|

|

|

|

|

|

|

|

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

56

vk.com/id446425943

Anglo American – HOLD

Renaissance Capital

14 January 2019

Metals & Mining

Figure 92: Anglo American, $mn (unless otherwise noted)

|

|

|

|

Anglo American |

AGLJ.J |

Target price, ZAR: |

320 |

Market capitalisation, $mn: |

31,660 |

Share price, ZAR: |

312 |

Enterprise value, $mn: |

45,876 |

Potential 12-month return: |

8.6% |

Dec-YE |

|

|

2016 |

2017 |

2018E |

2019E |

2020E |

Income statement |

|

|

|

|

|

|

|

Revenue |

|

|

23,142 |

28,650 |

28,990 |

27,691 |

27,880 |

Underlying EBITDA |

|

|

6,104 |

8,823 |

9,210 |

9,308 |

8,349 |

Underlying EBIT |

|

|

3,822 |

6,247 |

6,454 |

6,421 |

5,399 |

Net interest |

|

|

-567 |

-635 |

-474 |

-318 |

-262 |

Taxation |

|

|

-821 |

-1,770 |

-2,016 |

-1,931 |

-1,627 |

Minority interest in profit |

|

|

-329 |

-891 |

-899 |

-936 |

-844 |

Net profit for the year |

|

|

1,594 |

3,166 |

2,870 |

3,236 |

2,666 |

Underlying earnings |

|

|

2,210 |

3,272 |

3,145 |

3,236 |

2,666 |

Underlying EPS, USc |

|

|

172 |

257 |

247 |

255 |

210 |

Thomson Reuters consensus EPS, USc |

|

|

|

246 |

250 |

228 |

|

DPS declared, USc |

|

|

0 |

102 |

99 |

127 |

199 |

Underlying EBIT |

|

|

185 |

512 |

826 |

1,051 |

1,289 |

Platinum |

|

|

|||||

EBIT margin |

|

|

4% |

10% |

15% |

22% |

26% |

Diamonds |

|

|

1,019 |

873 |

759 |

779 |

792 |

EBIT margin |

|

|

17% |

15% |

13% |

13% |

13% |

Copper |

|

|

261 |

923 |

1,253 |

1,074 |

1,004 |

EBIT margin |

|

|

9% |

22% |

27% |

25% |

23% |

Nickel |

|

|

-15 |

0 |

92 |

37 |

113 |

EBIT margin |

|

|

-4% |

0% |

16% |

7% |

18% |

Iron ore and manganese |

|

|

1,275 |

1,978 |

1,207 |

1,515 |

1,280 |

EBIT margin |

|

|

46% |

57% |

36% |

48% |

42% |

Coal |

|

|

1,112 |

2,274 |

2,599 |

2,271 |

1,230 |

EBIT margin |

|

|

21% |

32% |

35% |

33% |

20% |

Other |

|

|

-15 |

-313 |

-282 |

-307 |

-309 |

Underlying EBIT |

|

|

3,822 |

6,247 |

6,454 |

6,421 |

5,399 |

Income statement ratios |

|

|

|

|

|

|

|

EBITDA margin |

|

|

26% |

31% |

32% |

34% |

30% |

EBIT margin |

|

|

17% |

22% |

22% |

23% |

19% |

EPS Growth |

|

|

169% |

49% |

-4% |

3% |

-18% |

Dividend payout ratio |

|

|

0% |

40% |

40% |

50% |

95% |

Input assumptions |

|

|

|

|

|

|

|

$/ZAR |

|

|

14.70 |

13.31 |

13.24 |

14.31 |

14.14 |

Platinum, $/oz |

|

|

988 |

950 |

880 |

870 |

1,070 |

Copper, USc/lb |

|

|

221 |

280 |

296 |

272 |

289 |

Hard coking coal, $/t |

|

|

114 |

210 |

202 |

190 |

163 |

Iron ore fines (62%Fe, CIF China), $/t |

|

|

58 |

71 |

66 |

62 |

62 |

Required breakeven price |

|

|

|

|

|

|

|

Breakeven price - 3PGM, $/oz |

|

|

754 |

774 |

803 |

759 |

701 |

Breakeven price - copper, USc/lb |

|

|

198 |

216 |

206 |

208 |

228 |

Breakeven price - coking coal, $/t |

|

|

85 |

129 |

122 |

122 |

123 |

Breakeven price - Export thermal coal, $/t |

|

46 |

59 |

60 |

62 |

71 |

|

Sales volumes |

|

|

|

|

|

|

|

Platinum, koz |

|

|

2,416 |

2,505 |

2,430 |

2,000 |

2,000 |

Diamonds (consolidated sales), mn ct |

|

|

30.0 |

33.1 |

32.4 |

30.3 |

30.3 |

Total iron ore, mnt |

|

|

59 |

61 |

46 |

60 |

65 |

Total copper segment, kt |

|

|

577 |

579 |

660 |

663 |

653 |

Metallurgical coal, mnt |

|

|

20.7 |

19.8 |

21.4 |

22.0 |

22.0 |

Attributable Cu eq volumes, kt |

|

|

2,962 |

2,910 |

2,700 |

2,768 |

2,834 |

Volume growth |

|

|

0.1% |

-1.7% |

-7.2% |

2.5% |

2.4% |

Contribution to FY18E attributable underlying EBITDA |

|

|

|

||||

|

|

|

|

Platinum (80% of |

|

|

|

|

|

|

|

AMS) |

|

|

|

Coal |

|

|

|

11% |

|

Diamonds (85% of |

|

|

|

|

|

|

De Beers) |

|

|

38% |

|

|

|

|

|

13% |

|

|

|

|

|

|

|

Copper |

|

Samancor |

|

|

|

|

Nickel |

16% |

|

Manganese |

|

|

|

|

|

|

|

Minas Rio Kumba Iron Ore |

2% |

|

|

||||

8% |

|

|

|||||

|

-4% |

|

(51%) |

|

|

|

|

|

|

|

|

8% |

|

|

|

Dec-YE |

|

|

|

2018E |

2019E |

2020E |

2016 |

2017 |

|

||||

Balance sheet |

|

|

|

|

|

|

Net operating assets |

32,315 |

33,172 |

|

31,972 |

31,909 |

32,872 |

Financial instruments |

497 |

211 |

|

169 |

195 |

205 |

Equity |

19,016 |

22,972 |

|

23,343 |

25,062 |

25,727 |

Minority interest |

5,309 |

5,910 |

|

5,719 |

5,953 |

6,164 |

Net debt |

8,487 |

4,501 |

|

3,080 |

1,089 |

1,186 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing* |

30.9% |

16.4% |

|

11.7% |

4.2% |

4.4% |

Net debt to EBITDA |

1.4x |

0.5x |

|

0.3x |

0.1x |

0.1x |

RoCE |

10.8% |

17.8% |

|

18.8% |

19.3% |

15.6% |

RoIC (after tax) |

6.0% |

15.1% |

|

10.3% |

14.6% |

10.5% |

RoE |

12.4% |

15.6% |

|

13.6% |

13.4% |

10.5% |

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

4,573 |

8,101 |

|

6,137 |

8,301 |

6,489 |

Capex (net of disposals) |

-2,388 |

-2,150 |

|

-2,240 |

-3,950 |

-3,868 |

Other cash flows |

2,045 |

-688 |

|

-182 |

0 |

0 |

FCF |

4,230 |

5,263 |

|

3,715 |

4,351 |

2,621 |

Equity shareholders' cash |

4,423 |

4,607 |

|

2,732 |

3,507 |

1,904 |

Dividends and share buy-backs |

0 |

-621 |

|

-1,311 |

-1,516 |

-2,000 |

Surplus (deficit) cash |

4,423 |

3,986 |

|

1,421 |

1,990 |

-96 |

Cash flow ratios |

|

|

|

|

|

|

Working capital days |

52 |

33 |

|

32 |

20 |

23 |

Capex/EBITDA |

43.4% |

28.0% |

|

28.7% |

49.5% |

53.2% |

FCF yield |

15.9% |

16.9% |

|

9.9% |

12.2% |

7.3% |

Equity shareholders' yield |

34.7% |

22.1% |

|

9.5% |

12.3% |

6.7% |

Cash conversion |

2.0x |

1.4x |

|

0.9x |

1.1x |

0.7x |

Valuation |

|

|

|

|

|

|

SoTP DCF fair value and calculation of target price |

|

$mn |

ZAR/sh |

|||

Platinum |

|

|

|

|

8,248 |

91.5 |

Diamonds |

|

|

|

|

6,962 |

77.3 |

Coal |

|

|

|

|

6,745 |

74.9 |

Copper |

|

|

|

|

5,957 |

66.1 |

Nickel |

|

|

|

|

981 |

10.9 |

Kumba Iron Ore |

|

|

|

|

3,269 |

36.3 |

Samancor manganese |

|

|

|

|

3,535 |

39.2 |

Anglo Ferrous Brazil |

|

|

|

|

1,336 |

14.8 |

Corporate & other |

|

|

|

|

-3,966 |

-44.0 |

Total enterprise value excluding minority interests |

|

|

|

33,068 |

367.0 |

|

Attributable net debt as at 31 December 2017 |

|

|

|

-4,536 |

-50.3 |

|

Investments as at 31 December 2017 |

|

|

|

|

211 |

2.3 |

Equity value as at 8/1/2019 |

|

|

|

|

28,743 |

319.0 |

Rounded to |

|

|

|

|

|

320.0 |

Share price on 7/1/2019 |

|

|

|

|

|

311.6 |

Expected share price return |

|

|

|

|

|

2.7% |

Plus: expected dividend yield |

|

|

|

|

|

5.9% |

Total implied one-year return |

|

|

|

|

|

8.6% |

Share price range, ZAR: |

|

|

|

|

|

|

12-month high on 4/10/2018 |

336 |

12-month low on 4/4/2018 |

262 |

|||

Price move since high |

-7.2% |

Price move since low |

|

19.2% |

||

Calculation of discount rate |

|

|

|

|

|

|

WACC |

9.5% |

Cost of debt |

|

|

5.0% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

30% |

|

Equity risk premium |

5.0% |

After-tax cost of debt |

|

3.5% |

||

Beta |

1.30 |

Debt weighting |

|

15% |

||

Cost of equity |

10.5% |

Terminal growth rate |

|

3.0% |

||

Valuation ratios |

|

|

|

|

|

|

Dec-YE |

2016 |

2017 |

|

2018E |

2019E |

2020E |

P/E multiple |

5.8x |

6.4x |

|

9.1x |

8.8x |

10.7x |

Dividend yield |

0.0% |

6.2% |

|

4.4% |

5.7% |

8.8% |

EV/EBITDA |

4.8x |

4.1x |

|

4.8x |

4.5x |

4.9x |

P/B |

0.7x |

0.9x |

|

1.2x |

1.1x |

1.1x |

NAV per share, $ |

14.8 |

18.0 |

|

18.4 |

19.7 |

20.3 |

NAV per share, ZAR |

217 |

240 |

|

243 |

282 |

286 |

* Gearing defined as net debt/(net debt +equity)

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

57

vk.com/id446425943

Assore – HOLD

Renaissance Capital

14 January 2019

Metals & Mining

Figure 93: Assore, ZARmn (unless otherwise stated)

|

|

|

|

Assore |

ASRJ.J |

Target price, ZAR: |

300 |

Market capitalisation, ZARmn: |

40,815 |

Last price, ZAR: |

294 |

Enterprise value, ZARmn: |

33,863 |

Potential 12-month return: |

10.3% |

Jun-YE |

2017 |

2018 |

2019E |

2020E |

2021E |

Income statement |

|

|

|

|

|

Revenue |

5,945 |

6,306 |

5,751 |

6,226 |

6,510 |

Underlying EBITDA |

2,237 |

1,846 |

1,680 |

1,685 |

1,791 |

Underlying EBIT |

2,120 |

1,683 |

1,493 |

1,484 |

1,580 |

Investment and other income |

372 |

649 |

738 |

843 |

1,058 |

Interest paid |

-20 |

-19 |

-12 |

0 |

0 |

Taxation |

-583 |

-646 |

-621 |

-652 |

-739 |

Equity income |

3,249 |

3,508 |

3,590 |

2,132 |

1,962 |

Minority interest in profit |

-117 |

-56 |

17 |

18 |

18 |

Net profit for the year |

5,021 |

5,119 |

5,204 |

3,826 |

3,880 |

Headline earnings |

5,209 |

5,109 |

5,204 |

3,826 |

3,880 |

HEPS, ZAc |

5,410 |

4,953 |

5,045 |

3,709 |

3,761 |

Thomson Reuters consensus EPS, ZAc |

|

|

5,328 |

3,903 |

4,186 |

DPS declared, ZAc |

1,400 |

2,200 |

2,610 |

2,190 |

2,500 |

Underlying EBIT |

1,200 |

704 |

473 |

588 |

636 |

Other mining and trading business |

|||||

EBIT margin |

20% |

11% |

8% |

9% |

10% |

Commissions on sales and technical fees |

920 |

979 |

1,020 |

895 |

943 |

Total consolidated |

2,120 |

1,683 |

1,493 |

1,484 |

1,580 |

Equity accounted: Assmang |

2,881 |

2,115 |

2,239 |

1,185 |

1,033 |

Iron ore |

|||||

EBIT margin |

36% |

29% |

30% |

18% |

16% |

Manganese |

1,681 |

2,553 |

2,809 |

1,837 |

1,764 |

EBIT margin |

33% |

40% |

40% |

29% |

26% |

Chrome |

-5 |

-29 |

0 |

0 |

0 |

Underlying EBIT* |

6,677 |

6,322 |

6,541 |

4,505 |

4,377 |

Income statement ratios |

|

|

|

|

|

EBITDA margin * |

41% |

37% |

38% |

30% |

29% |

EBIT margin * |

35% |

31% |

32% |

24% |

22% |

HEPS growth |

220% |

-8% |

2% |

-26% |

1% |

Dividend payout ratio |

38% |

60% |

70% |

80% |

90% |

Input assumptions |

|

|

|

|

|

Iron ore spot (CIF China), $/t |

69 |

67 |

65 |

61 |

62 |

Manganese ore (44%, CIF China), $/mtu |

5.72 |

6.79 |

6.32 |

5.24 |

5.41 |

Ferro Manganese - CIF, $/t |

1,166 |

1,341 |

1,169 |

1,100 |

1,135 |

Chrome ore, $/t |

278 |

207 |

181 |

189 |

202 |

ZAR/$ |

13.60 |

12.85 |

14.25 |

14.25 |

14.09 |

Required breakeven price |

|

|

|

|

|

Iron ore, $/t |

42 |

45 |

47 |

52 |

53 |

Manganese ore, $/mtu |

4.37 |

5.08 |

4.58 |

4.37 |

4.55 |

Chrome ore, $/t |

208 |

153 |

153 |

158 |

168 |

Assmang sales volumes (100%) |

17.3 |

17.9 |

17.4 |

17.4 |

17.4 |

Iron ore, mnt |

|||||

Manganese ore, mnt |

3.0 |

3.2 |

3.1 |

3.1 |

3.7 |

Manganese alloys, kt |

303 |

378 |

400 |

400 |

400 |

Chrome ore, kt |

1,279 |

1,557 |

1,400 |

1,500 |

1,500 |

Attributable Cu eq volumes, kt |

217 |

227 |

223 |

223 |

233 |

Volume growth |

5.7% |

4.5% |

-1.8% |

0.0% |

4.4% |

Contribution to FY19E attributable underlying EBITDA

Other mining, |

|

|

trading and |

|

|

shipping activities |

Iron ore |

|

21% |

||

38% |

||

|

Manganese

41%

Jun-YE |

|

|

|

2019E |

2020E |

2021E |

2017 |

2018 |

|

||||

Balance sheet |

|

|

|

|

|

|

Net operating assets |

17,547 |

17,915 |

|

17,007 |

17,065 |

17,103 |

Investments |

253 |

270 |

|

208 |

208 |

208 |

Equity |

22,872 |

26,091 |

|

27,670 |

28,226 |

28,862 |

Minority interest |

-24 |

-41 |

|

-44 |

-48 |

-52 |

Net (cash) debt |

-5,047 |

-7,865 |

|

-10,411 |

-10,905 |

-11,500 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing* |

-28.3% |

-43.2% |

|

-60.3% |

-63.0% |

-66.2% |

Net debt to EBITDA plus equity income |

-0.9x |

-1.5x |

|

-2.0x |

-2.9x |

-3.1x |

RoCE |

39.5% |

35.0% |

|

36.7% |

25.9% |

25.1% |

RoIC (after tax) |

30.8% |

27.3% |

|

28.6% |

20.2% |

19.5% |

RoE (ex. cash) |

28.6% |

25.6% |

|

25.6% |

17.2% |

16.3% |

*net debt/(net debt+equity) |

|

|

|

|

|

|

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

4,904 |

4,746 |

|

5,845 |

3,438 |

3,357 |

Capex |

-127 |

-367 |

|

-272 |

-296 |

-295 |

Other cash flows |

-1,422 |

-25 |

|

0 |

0 |

0 |

FCF |

3,356 |

4,354 |

|

5,573 |

3,143 |

3,062 |

Equity shareholders' cash |

3,473 |

4,718 |

|

6,171 |

3,764 |

3,838 |

Dividends and share buy-backs |

-1,095 |

-1,900 |

|

-3,626 |

-3,269 |

-3,243 |

Movement in net debt |

2,378 |

2,818 |

|

2,545 |

495 |

595 |

Cash flow ratios |

|

|

|

|

|

|

Working capital days |

30 |

12 |

|

17 |

14 |

12 |

Capex/EBITDA * |

19.8% |

25.6% |

|

26.6% |

34.1% |

31.6% |

FCF yield |

20.2% |

19.4% |

|

28.0% |

16.2% |

16.3% |

Equity shareholders' yield |

16.0% |

15.5% |

|

20.3% |

12.4% |

12.6% |

Cash conversion |

0.7x |

0.9x |

|

1.2x |

1.0x |

1.0x |

Valuation |

|

|

|

|

|

|

SoTP DCF fair value |

|

|

|

|

ZARmn |

ZAR/sh |

Assmang |

|

|

|

|

18,494 |

132 |

Marketing fee |

|

|

|

|

5,178 |

37 |

Other mining and trading |

|

|

|

|

3,239 |

23 |

Other |

|

|

|

|

0 |

0 |

Enterprise value |

|

|

|

|

26,911 |

193 |

Other Investments |

|

|

|

|

270 |

2 |

Net cash (debt) as at 30 June 2018 |

|

|

|

|

7,865 |

56 |

Dividends retained against BEE vendor loans |

|

|

|

3,500 |

25 |

|

DCF fair value for equity |

|

|

|

|

38,546 |

276 |

Plus: equity shareholders' cash/share |

|

|

|

|

|

47 |

Less: DPS |

|

|

|

|

|

-25 |

Rounded to |

|

|

|

|

|

300 |

Share price on 7/1/2019 |

|

|

|

|

|

294 |

Expected share price return |

|

|

|

|

|

1.9% |

Plus: expected dividend yield |

|

|

|

|

|

8.4% |

Total implied one-year return |

|

|

|

|

|

10.3% |

Share price range, ZAR: |

|

|

|

|

|

|

12-month high on 18/1/2018 |

430 |

12-month low on 20/7/2018 |

252 |

|||

Price move since high |

-31.6% |

Price move since low |

|

16.6% |

||

Calculation of discount rate |

|

|

|

|

|

|

WACC |

15.1% |

Cost of debt |

|

|

9.5% |

|

Risk-free rate |

9.0% |

Tax rate |

|

|

28% |

|

Equity risk premium |

5.0% |

After-tax cost of debt |

|

6.8% |

||

Beta |

1.30 |

Debt weighting |

|

0% |

||

Cost of equity |

15.5% |

Terminal growth rate |

|

3.0% |

||

Valuation ratios |

|

|

|

|

|

|

Jun-YE |

2017 |

2018 |

|

2019E |

2020E |

2021E |

P/E multiple |

4.7x |

7.0x |

|

6.9x |

9.3x |

9.2x |

Dividend yield |

6.7% |

7.5% |

|

8.9% |

7.4% |

8.5% |

Average enterprise value, ZARmn |

24,246 |

33,217 |

|

30,631 |

30,132 |

29,534 |

EV/(EBITDA + equity income) |

4.4x |

6.2x |

|

5.8x |

7.9x |

7.9x |

P/B |

1.3x |

1.6x |

|

1.5x |

1.5x |

1.4x |

NAV per share, ZAR |

164 |

187 |

|

198 |

202 |

207 |

Net cash (debt) per share, ZAR |

36 |

56 |

|

75 |

78 |

82 |

* Proportionately consolidated

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

58

vk.com/id446425943

BHP – HOLD

Renaissance Capital

14 January 2019

Metals & Mining

Figure 94: BHP, $mn (unless otherwise stated) |

|

|

|

BHP |

BILJ.J |

Target price, ZAR: |

300 |

Market capitalisation, $mn: |

110,086 |

Share price, ZAR: |

297 |

Enterprise value, $mn: |

131,291 |

Potential 12-month return: |

9.8% |

Jun-YE |

2017 |

2018 |

2019E |

2020E |

2021E |

Income statement |

|

|

|

|

|

Revenue |

38,285 |

43,650 |

41,690 |

40,472 |

40,917 |

Underlying EBITDA |

20,296 |

23,183 |

22,466 |

20,454 |

20,105 |

Underlying EBIT |

12,391 |

16,564 |

15,643 |

13,852 |

13,489 |

Net interest |

-1,431 |

-1,245 |

-1,091 |

-1,012 |

-992 |

Taxation |

-4,100 |

-7,007 |

-4,780 |

-4,299 |

-4,179 |

Minority interest in profit |

-332 |

-1,118 |

-823 |

-894 |

-968 |

Attributable profit |

5,890 |

4,823 |

8,950 |

7,648 |

7,350 |

Underlying attributable profit |

6,732 |

8,933 |

8,950 |

7,648 |

7,350 |

Underlying EPS, USc |

127 |

168 |

174 |

152 |

145 |

Thomson Reuters consensus EPS, USc |

|

|

184 |

166 |

174 |

DPS declared, USc |

83 |

118 |

241 |

137 |

145 |

Underlying EBIT |

-777 |

467 |

0 |

0 |

0 |

Petroleum - US onshore |

|||||

EBIT margin |

-36% |

47% |

- |

- |

- |

Petroleum - Conventional |

1,349 |

1,082 |

1,710 |

1,295 |

1,145 |

EBIT margin |

29% |

25% |

31% |

27% |

25% |

Copper |

1,985 |

4,330 |

2,494 |

3,185 |

3,595 |

EBIT margin |

27% |

37% |

25% |

29% |

30% |

Iron ore |

7,174 |

7,194 |

7,442 |

6,811 |

6,999 |

EBIT margin |

49% |

49% |

51% |

49% |

49% |

Coal |

3,050 |

3,683 |

4,239 |

2,806 |

1,997 |

EBIT margin |

40% |

41% |

45% |

34% |

26% |

Other |

-390 |

-192 |

-241 |

-245 |

-246 |

Underlying EBIT |

12,391 |

16,564 |

15,643 |

13,852 |

13,489 |

Income statement ratios |

|

|

|

|

|

EBITDA margin |

55% |

55% |

55% |

52% |

51% |

EBIT margin |

32% |

38% |

38% |

34% |

33% |

EPS growth |

455% |

33% |

4% |

-13% |

-5% |

Dividend payout ratio |

66% |

70% |

139% |

90% |

100% |

Input assumptions |

|

|

|

|

|

Brent crude oil, $/bbl |

51 |

64 |

69 |

63 |

61 |

Iron ore fines (62%Fe, CIF China), $/t |

69 |

67 |

65 |

61 |

62 |

Copper, USc/lb |

245 |

306 |

275 |

278 |

296 |

Hard coking coal, $/t |

190 |

200 |

196 |

166 |

157 |

$/AUD |

0.75 |

0.78 |

0.72 |

0.75 |

0.80 |

Oil breakeven price - conventional, $/boe |

29 |

37 |

48 |

47 |

44 |

Copper breakeven price, $/t |

3,752 |

4,001 |

3,960 |

3,866 |

4,018 |

Iron ore breakeven price, $/t |

34 |

34 |

34 |

38 |

36 |

Coking coal breakeven price, $/t |

81 |

92 |

84 |

93 |

102 |

Sales volumes (BHP's share) |

|

|

|

|

|

Petroleum products, MMboe* |

209 |

193 |

118 |

111 |

108 |

Iron ore, mnt |

231 |

237 |

241 |

253 |

256 |

Copper, kt |

991 |

1,238 |

1,179 |

1,235 |

1,258 |

Metallurgical coal, mnt |

38 |

41 |

44 |

45 |

45 |

Export thermal coal, mnt |

28 |

28 |

27 |

28 |

28 |

Attributable Cu eq volumes, kt |

5,989 |

6,300 |

5,888 |

6,014 |

5,907 |

Volume growth |

-6.9% |

5.2% |

-6.5% |

2.1% |

-1.8% |

Contribution to FY19E underlying EBITDA

|

US onshore |

Conventional |

Coal |

petroleum |

petroleum |

22% |

0% |

16% |

|

|

Copper |

|

|

21% |

Iron ore |

|

|

41% |

|

|

Jun-YE |

|

|

|

2019E |

2020E |

2021E |

2017 |

2018 |

|

||||

Balance sheet |

|

|

|

|

|

|

Net operating assets |

79,194 |

71,636 |

|

62,680 |

63,904 |

64,266 |

Investments |

-147 |

-32 |

|

39 |

39 |

39 |

Equity |

57,258 |

55,592 |

|

47,268 |

47,930 |

48,174 |

Minority interest |

5,468 |

5,078 |

|

5,243 |

5,421 |

5,615 |

Net debt |

16,321 |

10,934 |

|

10,208 |

10,591 |

10,515 |

Balance sheet ratios |

|

|

|

|

|

|

Gearing* |

22.2% |

16.4% |

|

17.8% |

18.1% |

17.9% |

Net debt to EBITDA |

0.8x |

0.5x |

|

0.5x |

0.5x |

0.5x |

RoCE |

13.6% |

19.5% |

|

20.2% |

18.8% |

18.0% |

RoIC |

11.0% |

14.6% |

|

12.9% |

12.5% |

12.1% |

RoE |

12.1% |

15.8% |

|

17.4% |

16.1% |

15.3% |

Cash flow statement |

|

|

|

|

|

|

Operating cash flow |

17,837 |

19,610 |

|

16,391 |

15,722 |

15,597 |

Capex (net of disposals) |

-4,252 |

-4,979 |

|

2,800 |

-8,000 |

-7,262 |

Other |

-841 |

1,159 |

|

0 |

0 |

0 |

FCF |

12,744 |

15,790 |

|

19,191 |

7,722 |

8,335 |

Equity shareholders' cash |

12,659 |

10,607 |

|

18,000 |

6,602 |

7,182 |

Dividends and share buy backs |

-2,878 |

-5,220 |

|

-17,274 |

-6,985 |

-7,106 |

Excess cash |

9,781 |

5,387 |

|

726 |

-383 |

76 |

Cash flow ratios |

|

|

|

|

|

|

Working capital days** |

28 |

20 |

|

24 |

26 |

26 |

Capex/EBITDA |

21% |

21% |

|

-12% |

39% |

36% |

FCF yield |

12.3% |

13.0% |

|

15.5% |

6.2% |

6.7% |

Equity shareholders' yield |

15.5% |

10.0% |

|

16.6% |

6.1% |

6.6% |

Cash conversion |

1.9x |

1.2x |

|

2.0x |

0.9x |

1.0x |

Valuation |

|

|

|

|

|

|

SoTP valuation and calculation of target price |

|

|

|

$mn |

ZAR/sh |

|

US onshore petroleum at estimated sales value |

|

|

|

10,369 |

29 |

|

Conventional petroleum |

|

|

|

|

5,855 |

16 |

Copper |

|

|

|

|

19,895 |

55 |

Iron ore |

|

|

|

|

71,911 |

199 |

Coal |

|

|

|

|

18,283 |

51 |

Other |

|

|

|

|

-3,239 |

-9 |

Enterprise value as at 8/1/2019 |

|

|

|

|

123,073 |

341 |

Net debt, investments and buy-backs |

|

|

|

|

-16,166 |

-45 |

Equity value as at 8/1/2019 |

|

|

|

|

106,907 |

296 |

Plus: One year forward FCF/share |

|

|

|

|

|

33 |

Less: DPS |

|

|

|

|

|

-26 |

TP, rounded to |

|

|

|

|

|

300 |

Share price on 7/1/2019 |

|

|

|

|

|

297 |

Expected share price return |

|

|

|

|

|

1.0% |

Plus: expected dividend yield |

|

|

|

|

|

8.8% |

Total implied one-year return |

|

|

|

|

|

9.8% |

Share price range, ZAR: |

|

|

|

|

|

|

12-month high |

327 |

12-month low |

|

226 |

||

Price move since high |

-9.1% |

Price move since low |

|

31.5% |

||

Calculation of discount rate |

|

|

|

|

|

|

WACC |

9.0% |

Cost of debt |

|

|

4.5% |

|

Risk-free rate |

4.0% |

Tax rate |

|

|

30% |

|

Equity risk premium |

5.0% |

After-tax cost of debt |

|

3.2% |

||

Beta |

1.30 |

Debt weighting |

|

20.0% |

||

Cost of equity |

10.5% |

Terminal growth rate |

|

3.0% |

||

Valuation ratios |

|

|

|

|

|

|

Jun-YE |

2017 |

2018 |

|

2019E |

2020E |

2021E |

P/E multiple |

12.1x |

11.8x |

|

12.3x |

14.1x |

14.8x |

Dividend yield |

5.4% |

5.9% |

|

11.3% |

6.4% |

6.8% |

EV/EBITDA |

5.1x |

5.2x |

|

5.5x |

6.1x |

6.2x |

P/B |

1.4x |

1.9x |

|

2.3x |

2.3x |

2.2x |

NAV per share, $ |

10.8 |

10.4 |

|

9.3 |

9.5 |

9.5 |

NAV per share, ZAR |

146 |

134 |

|

133 |

135 |

134 |

*Net debt/(net debt+equity)

** Working capital/revenue*365

Source: Bloomberg, Thomson Reuters, Company data, Renaissance Capital estimates

59