Lectures_micro / Microeconomics_presentation_Chapter_9

.pdfchapter:

9

>> Making Decisions

Krugman/Wells

Economics

©2009 Worth Publishers

WHAT YOU WILL LEARN IN THIS CHAPTER

How economists model decision making by individuals and firms

The importance of implicit as well as explicit costs in decision making

The difference between accounting profit and

economic profit, and why economic profit is the correct basis for decisions

The difference between “either–or” and “how much” decisions

The principle of marginal analysis

What sunk costs are and why they should be ignored How to make decisions in cases where time is a factor

Opportunity Cost and Decisions

Opportunity Cost and Decisions

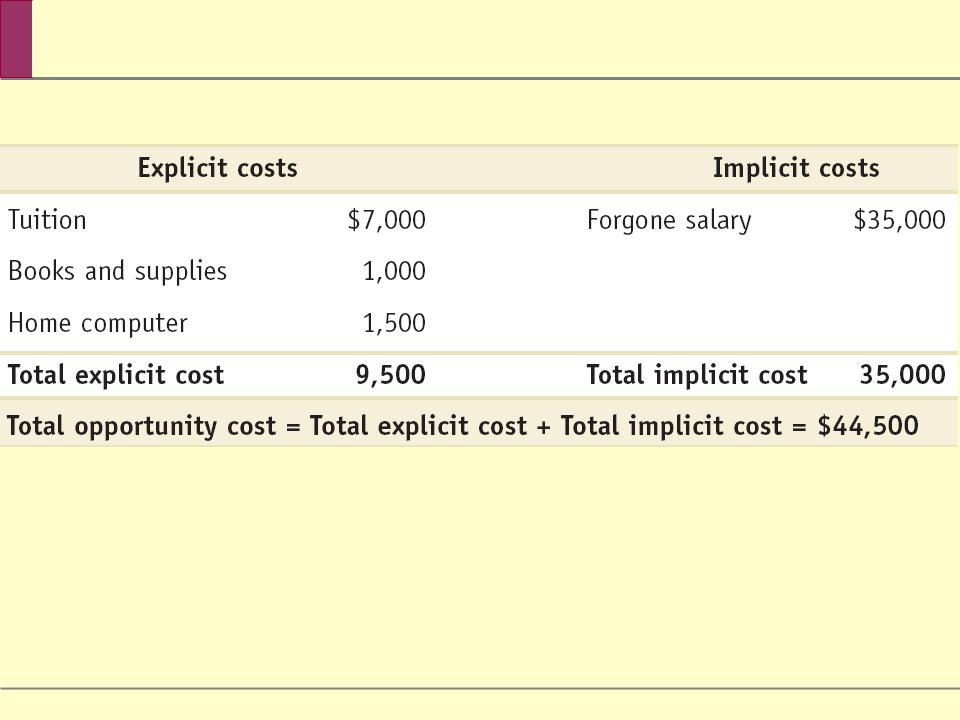

An explicit cost is a cost that involves actually laying out money.

An implicit cost does not require an outlay of money; it is measured by the value, in dollar terms, of the benefits that are forgone.

Opportunity Cost of an Additional Year of School

Opportunity Cost of an Additional Year of School

Accounting Profit Versus Economic Profit

Accounting Profit Versus Economic Profit

The accounting profit of a business is the business’s revenue minus the explicit costs and depreciation.

The economic profit of a business is the business’s revenue minus the opportunity cost of its resources. It is often less than the accounting profit.

Capital

Capital

The capital of a business is the value of its assets.

The implicit cost of capital is the opportunity cost of the capital used by a business.

Profits at Babette’s Cajun Cafe

Profits at Babette’s Cajun Cafe

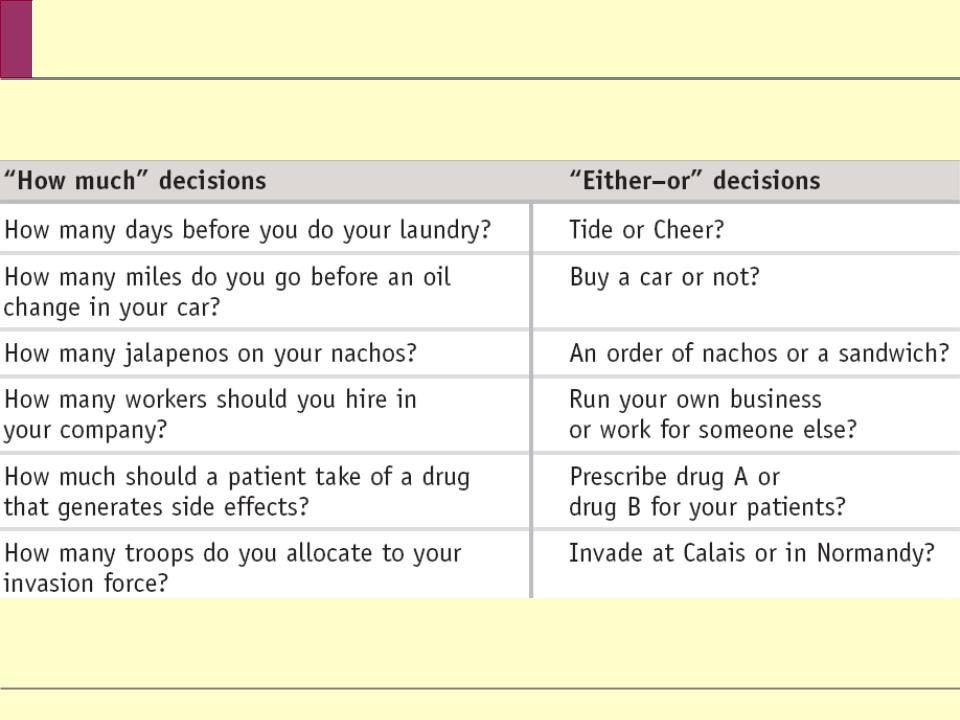

“How Much” Versus “Either–Or” Decisions

“How Much” Versus “Either–Or” Decisions

Marginal Cost

Marginal Cost

The marginal cost of producing a good or service is the additional cost incurred by producing one more unit of that good or service.

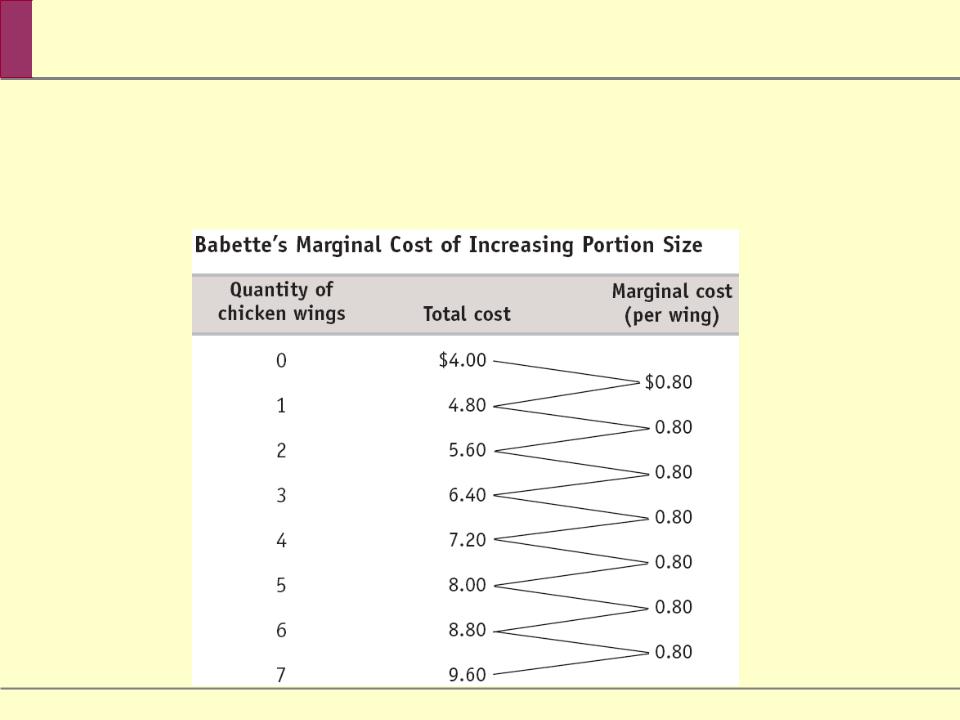

Constant Marginal Cost

Constant Marginal Cost

For every additional chicken wing per serving, Babette’s marginal cost is $0.80. Babette’s portion size decision has what economists call constant marginal cost: each chicken wing costs the same amount to produce as the previous one.

Production of a good or service has constant marginal cost when each additional unit costs the same to produce as the previous one.