МИНИСТЕРСТВО ОБЩЕГО И ПРОФЕССИОНАЛЬНОГО ОБРАЗОВАНИЯ РОССИЙСКОЙ ФЕДЕРАЦИИ

Государственный Университет Управления

Кафедра Экономической кибернетики

Лабораторная работа №1 по дисциплине:

«Методы социально-экономического прогнозирования»

На тему:

«Анализ одномерных временных рядов»

Выполнил: студент ИИСУ

специальности ММиИОЭ IV-1

Мирончук Евгений

Проверила: Писарева О.М.

Москва 1999

Исходные данные для выполнения лабораторной работы №1 представлены в Приложении №1

Последовательность выполнения каждого этапа задания: на основе исходных данных временного ряда (30 значений) необходимо построить прогноз на один период вперед (на 31 период). Чтобы построить более точный прогноз предполагается провести ряд опытов. Для этого исходный ряд разбивается на два участка: тестовый (25 значений) и проверочный (5 последних значений исх. ряда). Используя методы прогнозирования, на основе значений тестового участка строим прогноз на 5 периодов вперед. Затем, сравнивая прогнозные значения со значениями проверочного участка исходного ряда, выбираем наилучший метод и модель прогнозирования, с помощью которых и будет построен прогноз на 31 период.

Этап 1. Сглаживание временного ряда методом простой скользящей средней. Оценка точности прогнозирования уровня показателя.

Для определение расчетных значений показателя используется следующая формула:

где m – продолжительность интервала сглаживания.

В данной работе сглаживание производится для m=3,5,7,9,11,13

Для построения прогнозов используется

адаптивная скользящая средняя

![]()

Результаты сглаживания и построения прогнозов смотрите в Приложениях № 2-3.

Для оценки точности прогноза используется коэффициент несоответствия:

![]() ,

где L - продолжительность периода

упреждения

,

где L - продолжительность периода

упреждения

Чем ближе КТ к нулю, тем совершеннее прогноз. Коэффициенты несоответствия для построенных прогнозов приведены в таблице:

|

p |

Simple Moving Average |

|

KT |

|

|

1 (m=3) |

0,223 |

|

2 (m=5) |

0,232 |

|

3 (m=7) |

0,286 |

|

4 (m=9) |

0,430 |

|

5 (m=11) |

0,529 |

|

6 (m=13) |

0,629 |

Видно, что наименьшее значение KT получается при продолжительности интервала сглаживая m=3 (p=1). Следовательно, прогноз на 31 период будем строить при m = 3 (по исходному ряду).

Точечный прогноз (см. Приложение №

4): ![]()

Интервальная оценка прогноза:

![]()

![]()

![]()

Этап 2. Сглаживание временного ряда с использованием модели Брауна (экспоненциальное сглаживание). Оценка точности прогнозирования уровня показателя.

Для определение расчетных значений показателя используется следующая формула:

![]() ,

где - параметр

определяющий влияние устаревших данных

на сглаживаемый показатель.

,

где - параметр

определяющий влияние устаревших данных

на сглаживаемый показатель.

Прогнозирование с помощью процедур экспоненциального сглаживания осуществляется с помощью так называемых прогнозирующих полиномов. Прогноз уровня ряда yt на период t+ может быть представлен в виде:

![]() , где

- период упреждения

, где

- период упреждения

N – степень аппроксимирующего полинома

При N=0 ![]() (Simple

Exp. Smoothing)

(Simple

Exp. Smoothing)

При N=1 ![]() (Linear

Exp. Smoothing)

(Linear

Exp. Smoothing)

При N=2 ![]() (Quadratic

Exp. Smoothing)

(Quadratic

Exp. Smoothing)

Результаты построения 5-ти прогнозных значений с использованием Simple Exp. Smoothing приведены в Приложении № 5. Результаты оценки точности прогнозных значений со значениями проверочного участка представлены в таблице:

|

|

Simple Exp. Smoothing |

|

|

S |

KT |

|

|

0,1 |

18,72 |

0,507 |

|

0,2 |

15,32 |

0,373 |

|

0,3 |

12,96 |

0,256 |

|

0,4 |

11,35 |

0,216 |

|

0,5 |

10,28 |

0,213 |

|

0,6 |

9,57 |

0,220 |

|

0,7 |

9,09 |

0,229 |

|

0,8 |

8,76 |

0,233 |

|

0,9 |

8,53 |

0,238 |

Из таблицы видно, что наилучший прогноз получается при = 0,5. Прогноз на 31 период строим при = 0,5 (см. Приложение № 6).

Точечный прогноз: ![]()

Интервальная оценка прогноза:

![]()

![]()

Результаты построения прогнозных значений на 5 периодов вперед с использованием Linear Exp. Smoothing приведены в Приложении № 7. Результаты оценки точности прогноза представлены в таблице:

|

|

Linear Exp. Smoothing |

|

|

S |

KT |

|

|

0,1 |

16,23 |

0,508 |

|

0,2 |

12,93 |

0,338 |

|

0,3 |

10,28 |

0,647 |

|

0,4 |

9,21 |

0,754 |

|

0,5 |

8,99 |

0,720 |

|

0,6 |

9,13 |

0,632 |

|

0,7 |

9,42 |

0,545 |

|

0,8 |

9,83 |

0,484 |

|

0,9 |

10,37 |

0,449 |

КТ принимает минимальное значение при = 0,2.

Результаты построения прогнозного значение на 31 период приведены в Приложении № 8:

Точечный прогноз: ![]()

Интервальная оценка

прогноза: ![]()

Результаты построения прогнозных значений на 5 периодов вперед с использованием Quadratic Exp. Smoothing смотрите в Приложении № 9. Результаты оценки точности прогноза представлены в таблице:

|

|

Quadratic Exp. Smoothing |

|

|

S |

KT |

|

|

0,1 |

16,03 |

0,305 |

|

0,2 |

11,46 |

1,083 |

|

0,3 |

9,54 |

1,236 |

|

0,4 |

9,69 |

0,831 |

|

0,5 |

10,39 |

0,328 |

|

0,6 |

11,31 |

0,139 |

|

0,7 |

12,43 |

0,219 |

|

0,8 |

13,87 |

0,144 |

|

0,9 |

15,87 |

0,152 |

В данном случае минимальному значению КТ соответствует =0,6

Результаты прогнозирования на 31 период приведены в Приложении № 10:

Точечный прогноз: ![]()

Интервальная оценка

прогноза: ![]()

Этап 3. Сглаживание временного ряда с использованием модели тренда. Оценка точности прогнозирования уровня показателя.

Уровни временного ряда в данном случае могут быть описаны следующим уравнением:

![]()

Прогнозные значения показателя yt рассчитываются по формуле:

![]() ,

где l=1,L

,

где l=1,L

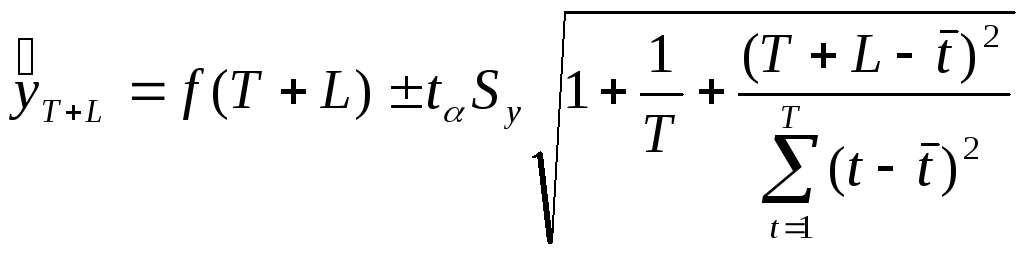

Для прогнозирования на основе модели линейного тренда доверительный интервал определяется по формуле:

или

![]()

![]()

Однако, перед тем как использовать модели трендов необходимо проверить гипотезы о существовании тенденции в развитии.

Сформулируем основную гипотезу (гипотеза о наличии тенденции в средних):

![]()

tтабл

(0,05;n+m-2)

tтабл

(0,05;n+m-2)

Если t>tкр принимаем гипотезу H1, тенденция в средних есть.

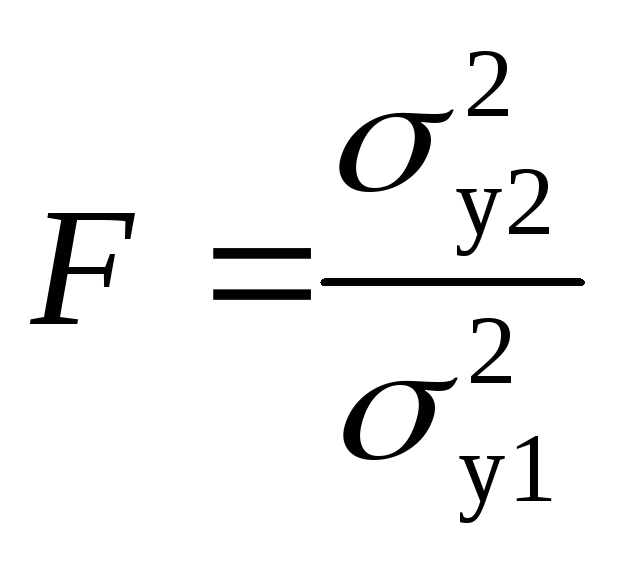

Перед проверкой основной гипотезы необходимо сформулировать и проверить вспомогательную (гипотеза о проверки однородности ряда):

![]()

![]()

![]()

Fтабл

(0.05;m-1;n-1)

Fтабл

(0.05;m-1;n-1)

Если F<Fтабл принимаем гипотезу H0, совокупность однородная

В данной работе было выполнено 16 различных разбиений тестового ряда (первые 25 значений) на 2 совокупности и проверены вспомогательная и основная гипотезы (см. Приложения № 11-18).

Только в одном случае была выявлена тенденция в средних (основная гипотеза Н1) при одновременной однородности совокупности (вспомогательная гипотеза Н0) (см. Приложение № 13).

Fрасч =1,903404 < Fтабл(0,05;17;6)=3,91 совокупность однородна

tрасч=2,309429 > tтабл(0,05;23)=2,0686 существует тенденция в средних

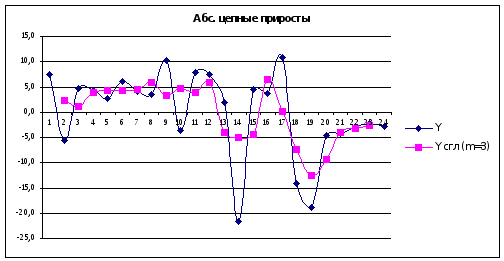

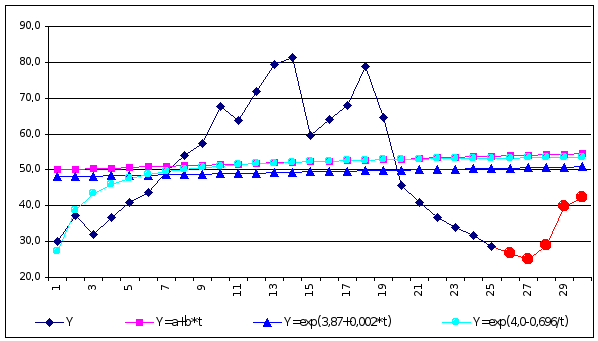

После проверки гипотез можно приступать к построению трендовых моделей. Однако для того, чтобы выбрать модель тренда необходимо определить тип экономического роста. Для этого рассчитаем абсолютные цепные приросты по следующей формуле:

![]()

Результаты расчетов и их графическое изображение представлены в Приложении № 29.

Заметим, что идентификация типа экономического роста, исходя из полученных результатов, представляется достаточно непростой задачей. Поэтому просто построим ряд простейших трендов и посмотрим их характеристики (см. Приложения № 19-26).

Основные характеристики использованных трендовых моделей, а также оценка качества прогнозов приведены в таблице:

|

№ |

Модели тренда |

Характеристики модели |

|||

|

S2 |

R2 |

Fрасч (Fтабл) |

KT |

||

|

1 |

Y=49,9+0,155*t |

301,186 |

0,00452 |

0,1 (4,297) |

0,682 |

|

2 |

Y=exp(3,87+0,002*t) |

0,118 |

0,00182 |

0,04 (4,297) |

0,582 |

|

3 |

Y=exp(4,0-0,696/t) |

0,0968 |

0,182 |

5,12 (4,297) |

0,659 |

|

4 |

Y=12,34+8,5*t-0,32*t^2 |

62,6173 |

0,802 |

44,57 (3,44) |

1,199 |

|

5 |

Y=1/(0,02+0,015/t) |

0,000043 |

0,198 |

5,69 (4,297) |

0,589 |

|

6 |

Y=39,6-7,3t+2,0t^2-0,13t^3+0,002t^4 |

39,098 |

0,888 |

39,5 (2,87) |

0,184 |

Из таблицы видно, что лучшими прогнозными (по KT ) и модельными (по R2 ) характеристиками обладает полином 4 порядка (модель № 6).

Линейная (№1) и экспоненциальная (№2) модели вообще говоря незначимы, так как Fрасч<Fтабл. Это подтверждает тот факт, что использовать эти модели в данном случае не следовало бы.

Итак, для построения прогноза на 31 период по исходному временному ряду используем полином 4-го порядка. Результаты построения смотрите в Приложении № 27 :

Точечный прогноз: ![]()

Интервальная оценка

прогноза: ![]()

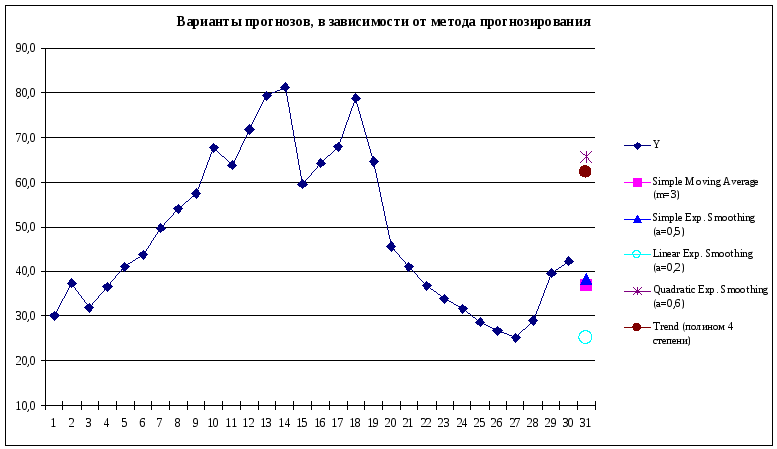

Все варианты прогнозных значений, полученных в этой лабораторной работе, можно наглядно увидеть на диаграмме, представленной в Приложении № 28. Как видно, полученные значения существенно отличаются друг от друга, и не дают возможности однозначно определить поведения исследуемой системы в будущем. Вероятнее всего в данном случае нужно применять другие методы и модели для построения прогноза.

Приложения

Приложение №1

|

|

|

t |

Y |

|

Ретроспективный период |

Тестовый участок |

1 |

30,0 |

|

2 |

37,4 |

||

|

3 |

31,9 |

||

|

4 |

36,7 |

||

|

5 |

41,0 |

||

|

6 |

43,7 |

||

|

7 |

49,7 |

||

|

8 |

53,9 |

||

|

9 |

57,4 |

||

|

10 |

67,6 |

||

|

11 |

63,9 |

||

|

12 |

71,8 |

||

|

13 |

79,3 |

||

|

14 |

81,3 |

||

|

15 |

59,6 |

||

|

16 |

64,2 |

||

|

17 |

67,9 |

||

|

18 |

78,8 |

||

|

19 |

64,6 |

||

|

20 |

45,7 |

||

|

21 |

41,0 |

||

|

22 |

36,8 |

||

|

23 |

33,9 |

||

|

24 |

31,6 |

||

|

25 |

28,7 |

||

|

Проверочный участок |

26 |

26,7 |

|

|

27 |

25,1 |

||

|

28 |

29 |

||

|

29 |

39,7 |

||

|

30 |

42,4 |

Приложение №2

(Simple Moving Average)

|

t |

Y |

|

Y^ |

m=3 (p=1) |

Y^ |

m=5 (p=2) |

Y^ |

m=7 (p=3) |

||||||||||||

|

1 |

30,0 |

|

30,0 |

|

|

|

|

|

30,0 |

|

|

|

|

|

30,0 |

|

|

|

|

|

|

2 |

37,4 |

|

37,4 |

|

|

|

|

|

37,4 |

|

|

|

|

|

37,4 |

|

|

|

|

|

|

3 |

31,9 |

|

31,9 |

|

|

|

|

|

31,9 |

|

|

|

|

|

31,9 |

|

|

|

|

|

|

4 |

36,7 |

|

36,7 |

|

|

|

|

|

36,7 |

|

|

|

|

|

36,7 |

|

|

|

|

|

|

5 |

41,0 |

|

41,0 |

|

|

|

|

|

41,0 |

|

|

|

|

|

41,0 |

|

|

|

|

|

|

6 |

43,7 |

|

43,7 |

|

|

|

|

|

43,7 |

|

|

|

|

|

43,7 |

|

|

|

|

|

|

7 |

49,7 |

|

49,7 |

|

|

|

|

|

49,7 |

|

|

|

|

|

49,7 |

|

|

|

|

|

|

8 |

53,9 |

|

53,9 |

|

|

|

|

|

53,9 |

|

|

|

|

|

53,9 |

|

|

|

|

|

|

9 |

57,4 |

|

57,4 |

|

|

|

|

|

57,4 |

|

|

|

|

|

57,4 |

|

|

|

|

|

|

10 |

67,6 |

|

67,6 |

|

|

|

|

|

67,6 |

|

|

|

|

|

67,6 |

|

|

|

|

|

|

11 |

63,9 |

|

63,9 |

|

|

|

|

|

63,9 |

|

|

|

|

|

63,9 |

|

|

|

|

|

|

12 |

71,8 |

|

71,8 |

|

|

|

|

|

71,8 |

|

|

|

|

|

71,8 |

|

|

|

|

|

|

13 |

79,3 |

|

79,3 |

|

|

|

|

|

79,3 |

|

|

|

|

|

79,3 |

|

|

|

|

|

|

14 |

81,3 |

|

81,3 |

|

|

|

|

|

81,3 |

|

|

|

|

|

81,3 |

|

|

|

|

|

|

15 |

59,6 |

|

59,6 |

|

|

|

|

|

59,6 |

|

|

|

|

|

59,6 |

|

|

|

|

|

|

16 |

64,2 |

|

64,2 |

|

|

|

|

|

64,2 |

|

|

|

|

|

64,2 |

|

|

|

|

|

|

17 |

67,9 |

|

67,9 |

|

|

|

|

|

67,9 |

|

|

|

|

|

67,9 |

|

|

|

|

|

|

18 |

78,8 |

|

78,8 |

|

|

|

|

|

78,8 |

|

|

|

|

|

78,8 |

|

|

|

|

|

|

19 |

64,6 |

|

64,6 |

|

|

|

|

|

64,6 |

|

|

|

|

|

64,6 |

|

|

|

|

|

|

20 |

45,7 |

|

45,7 |

|

|

|

|

|

45,7 |

|

|

|

|

|

45,7 |

|

|

|

|

|

|

21 |

41,0 |

|

41,0 |

|

|

|

|

|

41,0 |

|

|

|

|

|

41,0 |

|

|

|

|

|

|

22 |

36,8 |

|

36,8 |

|

|

|

|

|

36,8 |

|

|

|

|

|

36,8 |

40,3 |

|

|

|

|

|

23 |

33,9 |

|

33,9 |

|

|

|

|

|

33,9 |

34,4 |

|

|

|

|

33,9 |

|

36,9 |

|

|

|

|

24 |

31,6 |

|

31,6 |

31,4 |

|

|

|

|

31,6 |

|

33,1 |

|

|

|

31,6 |

|

|

35,6 |

|

|

|

25 |

28,7 |

|

28,7 |

|

30,6 |

|

|

|

28,7 |

|

|

32,3 |

|

|

28,7 |

|

|

|

34,8 |

|

|

26 |

26,7 |

|

31,4 |

|

|

30,2 |

|

|

34,4 |

|

|

|

32,0 |

|

40,3 |

|

|

|

|

34,5 |

|

27 |

25,1 |

|

30,6 |

|

|

|

30,7 |

|

33,1 |

|

|

|

|

32,1 |

36,9 |

|

|

|

|

|

|

28 |

29 |

|

30,2 |

|

|

|

|

30,5 |

32,3 |

|

|

|

|

|

35,6 |

|

|

|

|

|

|

29 |

39,7 |

|

30,7 |

|

|

|

|

|

32,0 |

|

|

|

|

|

34,8 |

|

|

|

|

|

|

30 |

42,4 |

|

30,5 |

|

|

|

|

|

32,1 |

|

|

|

|

|

34,5 |

|

|

|

|

|

|

|

|

Кт = |

0,223 |

|

|

|

|

|

0,232 |

|

|

|

|

|

0,286 |

|

|

|

|

|

Приложение №3

(Simple Moving Average)

|

|

Y^ |

m=9 (p=4) |

Y^ |

m=11 (p=5) |

Y^ |

m=13 (p=6) |

||||||||||||

|

|

30,0 |

|

|

|

|

|

30,0 |

|

|

|

|

|

30,0 |

|

|

|

|

|

|

|

37,4 |

|

|

|

|

|

37,4 |

|

|

|

|

|

37,4 |

|

|

|

|

|

|

|

31,9 |

|

|

|

|

|

31,9 |

|

|

|

|

|

31,9 |

|

|

|

|

|

|

|

36,7 |

|

|

|

|

|

36,7 |

|

|

|

|

|

36,7 |

|

|

|

|

|

|

|

41,0 |

|

|

|

|

|

41,0 |

|

|

|

|

|

41,0 |

|

|

|

|

|

|

|

43,7 |

|

|

|

|

|

43,7 |

|

|

|

|

|

43,7 |

|

|

|

|

|

|

|

49,7 |

|

|

|

|

|

49,7 |

|

|

|

|

|

49,7 |

|

|

|

|

|

|

|

53,9 |

|

|

|

|

|

53,9 |

|

|

|

|

|

53,9 |

|

|

|

|

|

|

|

57,4 |

|

|

|

|

|

57,4 |

|

|

|

|

|

57,4 |

|

|

|

|

|

|

|

67,6 |

|

|

|

|

|

67,6 |

|

|

|

|

|

67,6 |

|

|

|

|

|

|

|

63,9 |

|

|

|

|

|

63,9 |

|

|

|

|

|

63,9 |

|

|

|

|

|

|

|

71,8 |

|

|

|

|

|

71,8 |

|

|

|

|

|

71,8 |

|

|

|

|

|

|

|

79,3 |

|

|

|

|

|

79,3 |

|

|

|

|

|

79,3 |

|

|

|

|

|

|

|

81,3 |

|

|

|

|

|

81,3 |

|

|

|

|

|

81,3 |

|

|

|

|

|

|

|

59,6 |

|

|

|

|

|

59,6 |

|

|

|

|

|

59,6 |

|

|

|

|

|

|

|

64,2 |

|

|

|

|

|

64,2 |

|

|

|

|

|

64,2 |

|

|

|

|

|

|

|

67,9 |

|

|

|

|

|

67,9 |

|

|

|

|

|

67,9 |

|

|

|

|

|

|

|

78,8 |

|

|

|

|

|

78,8 |

|

|

|

|

|

78,8 |

|

|

|

|

|

|

|

64,6 |

|

|

|

|

|

64,6 |

|

|

|

|

|

64,6 |

54,9 |

|

|

|

|

|

|

45,7 |

|

|

|

|

|

45,7 |

50,3 |

|

|

|

|

45,7 |

|

53,0 |

|

|

|

|

|

41,0 |

47,7 |

|

|

|

|

41,0 |

|

49,4 |

|

|

|

41,0 |

|

|

50,8 |

|

|

|

|

36,8 |

|

45,4 |

|

|

|

36,8 |

|

|

48,1 |

|

|

36,8 |

|

|

|

50,1 |

|

|

|

33,9 |

|

|

41,7 |

|

|

33,9 |

|

|

|

46,3 |

|

33,9 |

|

|

|

|

49,1 |

|

|

31,6 |

|

|

|

39,2 |

|

31,6 |

|

|

|

|

43,3 |

31,6 |

|

|

|

|

|

|

|

28,7 |

|

|

|

|

38,4 |

28,7 |

|

|

|

|

|

28,7 |

|

|

|

|

|

|

|

47,7 |

|

|

|

|

|

50,3 |

|

|

|

|

|

54,9 |

|

|

|

|

|

|

|

45,4 |

|

|

|

|

|

49,4 |

|

|

|

|

|

53,0 |

|

|

|

|

|

|

|

41,7 |

|

|

|

|

|

48,1 |

|

|

|

|

|

50,8 |

|

|

|

|

|

|

|

39,2 |

|

|

|

|

|

46,3 |

|

|

|

|

|

50,1 |

|

|

|

|

|

|

|

38,4 |

|

|

|

|

|

43,3 |

|

|

|

|

|

49,1 |

|

|

|

|

|

|

Kт = |

0,430 |

|

|

|

|

|

0,529 |

|

|

|

|

|

0,629 |

|

|

|

|

|

Приложение № 4

(Simple Moving Average)

Forecast Table for Y

Model: Simple moving average of 3 terms

Period Data Forecast Residual

------------------------------------------------------------------------------

1,0 30,0

2,0 37,4

3,0 31,9

4,0 36,7 33,1 3,6

5,0 41,0 35,3333 5,66667

6,0 43,7 36,5333 7,16667

7,0 49,7 40,4667 9,23333

8,0 53,9 44,8 9,1

9,0 57,4 49,1 8,3

10,0 67,6 53,6667 13,9333

11,0 63,9 59,6333 4,26667

12,0 71,8 62,9667 8,83333

13,0 79,3 67,7667 11,5333

14,0 81,3 71,6667 9,63333

15,0 59,6 77,4667 -17,8667

16,0 64,2 73,4 -9,2

17,0 67,9 68,3667 -0,466667

18,0 78,8 63,9 14,9

19,0 64,6 70,3 -5,7

20,0 45,7 70,4333 -24,7333

21,0 41,0 63,0333 -22,0333

22,0 36,8 50,4333 -13,6333

23,0 33,9 41,1667 -7,26667

24,0 31,6 37,2333 -5,63333

25,0 28,7 34,1 -5,4

26,0 26,7 31,4 -4,7

27,0 25,1 29,0 -3,9

28,0 29,0 26,8333 2,16667

29,0 39,7 26,9333 12,7667

30,0 42,4 31,2667 11,1333

------------------------------------------------------------------------------

Lower 95,0% Upper 95,0%

Period Forecast Limit Limit

------------------------------------------------------------------------------

31,0 37,0333 12,265 61,8017

------------------------------------------------------------------------------

Forecast Summary

----------------

Forecast model selected: Simple moving average of 3 terms

Number of forecasts generated: 1

Number of periods withheld for validation: 0

Estimation Validation

Statistic Period Period

--------------------------------------------

MSE 119,772

MAE 9,36173

MAPE 19,6547

ME 0,433333

MPE -1,82275

The StatAdvisor

---------------

This model assumes that the best forecast for future data is given by

the average of the 3 most recent data values.You can select a

different forecasting model by pressing the alternate mouse button and

selecting Analysis Options.

The table also summarizes the performance of the currently selected

model in fitting the previous data. It displays:

(1) the mean squared error (MSE)

(2) the mean absolute error (MAE)

(3) the mean absolute percentage error (MAPE)

(4) the mean error (ME)

(5) the mean percentage error (MPE)

Each of the statistics is based on the one-ahead forecast errors,

which are the differences between the data value at time t and the

forecast of that value made at time t-1. The first three statistics

measure the magnitude of the errors. A better model will give a

smaller value. The last two statistics measure bias. A better model

will give a value close to 0.0.

Приложение №5

(Simple Exp. Smoothing)

|

t |

Y |

|

= 0,1 |

= 0,2 |

= 0,3 |

= 0,4 |

= 0,5 |

= 0,6 |

= 0,7 |

= 0,8 |

= 0,9 |

|

1 |

30,0 |

|

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

|

2 |

37,4 |

|

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

30,0 |

|

3 |

31,9 |

|

30,7 |

31,5 |

32,2 |

33,0 |

33,7 |

34,4 |

35,2 |

35,9 |

36,7 |

|

4 |

36,7 |

|

30,9 |

31,6 |

32,1 |

32,5 |

32,8 |

32,9 |

32,9 |

32,7 |

32,4 |

|

5 |

41,0 |

|

31,4 |

32,6 |

33,5 |

34,2 |

34,8 |

35,2 |

35,6 |

35,9 |

36,3 |

|

6 |

43,7 |

|

32,4 |

34,3 |

35,7 |

36,9 |

37,9 |

38,7 |

39,4 |

40,0 |

40,5 |

|

7 |

49,7 |

|

33,5 |

36,2 |

38,1 |

39,6 |

40,8 |

41,7 |

42,4 |

43,0 |

43,4 |

|

8 |

53,9 |

|

35,1 |

38,9 |

41,6 |

43,7 |

45,2 |

46,5 |

47,5 |

48,4 |

49,1 |

|

9 |

57,4 |

|

37,0 |

41,9 |

45,3 |

47,8 |

49,6 |

50,9 |

52,0 |

52,8 |

53,4 |

|

10 |

67,6 |

|

39,1 |

45,0 |

48,9 |

51,6 |

53,5 |

54,8 |

55,8 |

56,5 |

57,0 |

|

11 |

63,9 |

|

41,9 |

49,5 |

54,5 |

58,0 |

60,5 |

62,5 |

64,1 |

65,4 |

66,5 |

|

12 |

71,8 |

|

44,1 |

52,4 |

57,3 |

60,4 |

62,2 |

63,3 |

63,9 |

64,2 |

64,2 |

|

13 |

79,3 |

|

46,9 |

56,3 |

61,7 |

64,9 |

67,0 |

68,4 |

69,4 |

70,3 |

71,0 |

|

14 |

81,3 |

|

50,1 |

60,9 |

67,0 |

70,7 |

73,2 |

74,9 |

76,3 |

77,5 |

78,5 |

|

15 |

59,6 |

|

53,2 |

65,0 |

71,3 |

74,9 |

77,2 |

78,8 |

79,8 |

80,5 |

81,0 |

|

16 |

64,2 |

|

53,9 |

63,9 |

67,8 |

68,8 |

68,4 |

67,3 |

65,7 |

63,8 |

61,7 |

|

17 |

67,9 |

|

54,9 |

63,9 |

66,7 |

67,0 |

66,3 |

65,4 |

64,6 |

64,1 |

64,0 |

|

18 |

78,8 |

|

56,2 |

64,7 |

67,1 |

67,3 |

67,1 |

66,9 |

66,9 |

67,1 |

67,5 |

|

19 |

64,6 |

|

58,5 |

67,6 |

70,6 |

71,9 |

73,0 |

74,0 |

75,2 |

76,5 |

77,7 |

|

20 |

45,7 |

|

59,1 |

67,0 |

68,8 |

69,0 |

68,8 |

68,4 |

67,8 |

67,0 |

65,9 |

|

21 |

41,0 |

|

57,7 |

62,7 |

61,9 |

59,7 |

57,2 |

54,8 |

52,3 |

50,0 |

47,7 |

|

22 |

36,8 |

|

56,1 |

58,4 |

55,6 |

52,2 |

49,1 |

46,5 |

44,4 |

42,8 |

41,7 |

|

23 |

33,9 |

|

54,1 |

54,1 |

50,0 |

46,0 |

43,0 |

40,7 |

39,1 |

38,0 |

37,3 |

|

24 |

31,6 |

|

52,1 |

50,0 |

45,1 |

41,2 |

38,4 |

36,6 |

35,5 |

34,7 |

34,2 |

|

25 |

28,7 |

|

50,1 |

46,3 |

41,1 |

37,4 |

35,0 |

33,6 |

32,8 |

32,2 |

31,9 |

|

26 |

26,7 |

|

47,9 |

42,8 |

37,4 |

33,9 |

31,9 |

30,7 |

29,9 |

29,4 |

29,0 |

|

27 |

25,1 |

|

47,9 |

42,8 |

37,4 |

33,9 |

31,9 |

30,7 |

29,9 |

29,4 |

29,0 |

|

28 |

29 |

|

47,9 |

42,8 |

37,4 |

33,9 |

31,9 |

30,7 |

29,9 |

29,4 |

29,0 |

|

29 |

39,7 |

|

47,9 |

42,8 |

37,4 |

33,9 |

31,9 |

30,7 |

29,9 |

29,4 |

29,0 |

|

30 |

42,4 |

|

47,9 |

42,8 |

37,4 |

33,9 |

31,9 |

30,7 |

29,9 |

29,4 |

29,0 |

|

|

|

Кт = |

0,507 |

0,373 |

0,256 |

0,216 |

0,213 |

0,220 |

0,227 |

0,233 |

0,238 |

|

|

|

S^2 = |

350,3 |

234,6 |

167,9 |

128,7 |

105,6 |

91,58 |

82,62 |

76,71 |

72,75 |

|

|

|

|

18,72 |

15,32 |

12,96 |

11,35 |

10,28 |

9,569 |

9,09 |

8,758 |

8,529 |

Приложение №6

(Simple Exp. Smoothing)

Forecast Table for Y

Model: Simple exponential smoothing with alpha = 0,5

Period Data Forecast Residual

------------------------------------------------------------------------------

1,0 30,0 33,4395 -3,43946

2,0 37,4 31,7197 5,68027

3,0 31,9 34,5599 -2,65986

4,0 36,7 33,2299 3,47007

5,0 41,0 34,965 6,03503

6,0 43,7 37,9825 5,71752

7,0 49,7 40,8412 8,85876

8,0 53,9 45,2706 8,62938

9,0 57,4 49,5853 7,81469

10,0 67,6 53,4927 14,1073

11,0 63,9 60,5463 3,35367

12,0 71,8 62,2232 9,57684

13,0 79,3 67,0116 12,2884

14,0 81,3 73,1558 8,14421

15,0 59,6 77,2279 -17,6279

16,0 64,2 68,4139 -4,21395

17,0 67,9 66,307 1,59303

18,0 78,8 67,1035 11,6965

19,0 64,6 72,9517 -8,35174

20,0 45,7 68,7759 -23,0759

21,0 41,0 57,2379 -16,2379

22,0 36,8 49,119 -12,319

23,0 33,9 42,9595 -9,05948

24,0 31,6 38,4297 -6,82974

25,0 28,7 35,0149 -6,31487

26,0 26,7 31,8574 -5,15744

27,0 25,1 29,2787 -4,17872

28,0 29,0 27,1894 1,81064

29,0 39,7 28,0947 11,6053

30,0 42,4 33,8973 8,50266

------------------------------------------------------------------------------

Lower 95,0% Upper 95,0%

Period Forecast Limit Limit

------------------------------------------------------------------------------

31,0 38,1487 19,3014 56,9959

------------------------------------------------------------------------------

Forecast Summary

----------------

Forecast model selected: Simple exponential smoothing with alpha = 0,5

Number of forecasts generated: 1

Number of periods withheld for validation: 0

Estimation Validation

Statistic Period Period

--------------------------------------------

MSE 92,4695

MAE 8,27834

MAPE 17,8778

ME 0,313947

MPE -2,03894

The StatAdvisor

---------------

The table also summarizes the performance of the currently selected

model in fitting the previous data. It displays:

(1) the mean squared error (MSE)

(2) the mean absolute error (MAE)

(3) the mean absolute percentage error (MAPE)

(4) the mean error (ME)

(5) the mean percentage error (MPE)

Приложение №7

(Linear Exp. Smoothing)

|

t |

Y |

|

= 0,1 |

= 0,2 |

= 0,3 |

= 0,4 |

= 0,5 |

= 0,6 |

= 0,7 |

= 0,8 |

= 0,9 |

|

1 |

30,0 |

|

44,8 |

30,8 |

27,4 |

27,6 |

28,1 |

28,2 |

27,6 |

26,5 |

24,9 |

|

2 |

37,4 |

|

41,6 |

28,3 |

26,0 |

26,6 |

27,3 |

27,7 |

28,0 |

28,3 |

28,9 |

|

3 |

31,9 |

|

40,5 |

29,7 |

30,1 |

32,7 |

35,2 |

37,4 |

39,3 |

41,3 |

43,1 |

|

4 |

36,7 |

|

38,4 |

28,8 |

29,5 |

31,3 |

32,2 |

32,3 |

31,7 |

30,5 |

28,7 |

|

5 |

41,0 |

|

37,6 |

30,2 |

32,3 |

34,7 |

36,2 |

37,1 |

37,8 |

38,7 |

39,8 |

|

6 |

43,7 |

|

37,8 |

33,1 |

36,6 |

39,7 |

41,6 |

42,9 |

43,9 |

44,6 |

45,1 |

|

7 |

49,7 |

|

38,5 |

36,3 |

40,7 |

43,9 |

45,5 |

46,4 |

46,8 |

46,9 |

46,7 |

|

8 |

53,9 |

|

40,4 |

41,1 |

46,6 |

50,1 |

52,0 |

53,2 |

53,9 |

54,5 |

55,1 |

|

9 |

57,4 |

|

42,8 |

46,2 |

52,3 |

55,7 |

57,3 |

58,0 |

58,4 |

58,5 |

58,4 |

|

10 |

67,6 |

|

45,6 |

51,1 |

57,4 |

60,2 |

61,2 |

61,5 |

61,5 |

61,3 |

61,1 |

|

11 |

63,9 |

|

50,0 |

58,6 |

65,9 |

69,5 |

71,5 |

72,8 |

74,0 |

75,2 |

76,5 |

|

12 |

71,8 |

|

53,0 |

62,3 |

68,1 |

69,6 |

69,4 |

68,3 |

66,8 |

65,0 |

62,8 |

|

13 |

79,3 |

|

57,1 |

67,9 |

73,5 |

75,1 |

75,4 |

75,5 |

75,8 |

76,5 |

77,8 |

|

14 |

81,3 |

|

62,1 |

74,6 |

80,5 |

82,5 |

83,5 |

84,3 |

85,2 |

86,0 |

86,6 |

|

15 |

59,6 |

|

66,7 |

79,9 |

85,0 |

86,3 |

86,5 |

86,3 |

85,9 |

85,3 |

84,4 |

|

16 |

64,2 |

|

66,3 |

74,7 |

73,9 |

69,5 |

64,2 |

58,8 |

53,3 |

48,0 |

42,8 |

|

17 |

67,9 |

|

66,8 |

72,6 |

69,9 |

65,5 |

62,1 |

60,2 |

59,9 |

61,3 |

64,3 |

|

18 |

78,8 |

|

67,9 |

72,4 |

69,6 |

66,8 |

65,8 |

66,3 |

67,8 |

69,6 |

71,1 |

|

19 |

64,6 |

|

70,9 |

76,4 |

75,9 |

76,2 |

78,1 |

80,9 |

83,8 |

86,3 |

88,2 |

|

20 |

45,7 |

|

70,7 |

73,4 |

70,7 |

68,6 |

67,2 |

65,5 |

62,9 |

59,4 |

55,2 |

|

21 |

41,0 |

|

66,6 |

63,6 |

56,3 |

50,1 |

44,9 |

40,0 |

35,4 |

31,4 |

28,5 |

|

22 |

36,8 |

|

62,2 |

54,7 |

45,4 |

39,0 |

34,8 |

32,3 |

31,4 |

31,9 |

33,7 |

|

23 |

33,9 |

|

57,5 |

46,8 |

37,2 |

32,0 |

29,7 |

29,2 |

29,9 |

31,0 |

32,1 |

|

24 |

31,6 |

|

53,0 |

40,2 |

31,4 |

27,9 |

27,2 |

27,9 |

29,1 |

30,0 |

30,7 |

|

25 |

28,7 |

|

48,6 |

34,7 |

27,4 |

25,5 |

26,0 |

27,1 |

28,1 |

28,8 |

29,1 |

|

26 |

26,7 |

|

48,4 |

32,4 |

23,3 |

20,8 |

21,5 |

23,2 |

24,9 |

26,0 |

26,7 |

|

27 |

25,1 |

|

48,1 |

30,1 |

19,2 |

16,1 |

17,0 |

19,4 |

21,7 |

23,3 |

24,2 |

|

28 |

29 |

|

47,8 |

27,8 |

15,1 |

11,4 |

12,5 |

15,5 |

18,4 |

20,6 |

21,8 |

|

29 |

39,7 |

|

47,5 |

25,4 |

11,0 |

6,6 |

8,0 |

11,6 |

15,2 |

17,8 |

19,3 |

|

30 |

42,4 |

|

47,3 |

23,1 |

6,9 |

1,9 |

3,5 |

7,7 |

12,0 |

15,1 |

16,8 |

|

|

|

Кт = |

0,51 |

0,34 |

0,65 |

0,75 |

0,72 |

0,63 |

0,54 |

0,48 |

0,45 |

|

|

|

S^2 = |

263,4 |

167,3 |

105,7 |

84,8 |

80,9 |

83,4 |

88,8 |

96,6 |

107,4 |

|

|

|

|

16,23 |

12,93 |

10,28 |

9,21 |

8,99 |

9,13 |

9,42 |

9,83 |

10,37 |

Приложение № 8

(Linear Exp. Smoothing)

Forecast Table for Y

Model: Brown's linear exp. smoothing with alpha = 0,2

Period Data Forecast Residual

------------------------------------------------------------------------------

1,0 30,0 30,6777 -0,677734

2,0 37,4 28,1963 9,20369

3,0 31,9 29,6403 2,25965

4,0 36,7 28,6749 8,02508

5,0 41,0 30,106 10,894

6,0 43,7 33,0057 10,6943

7,0 49,7 36,2613 13,4387

8,0 53,9 41,0424 12,8576

9,0 57,4 46,1286 11,2714

10,0 67,6 51,0947 16,5053

11,0 63,9 58,6051 5,29487

12,0 71,8 62,2916 9,50837

13,0 79,3 67,8753 11,4247

14,0 81,3 74,6059 6,69413

15,0 59,6 79,9012 -20,3012

16,0 64,2 74,6661 -10,4661

17,0 67,9 72,5531 -4,65307

18,0 78,8 72,3466 6,45342

19,0 64,6 76,3966 -11,7966

20,0 45,7 73,4047 -27,7047

21,0 41,0 63,5777 -22,5777

22,0 36,8 54,6933 -17,8933

23,0 33,9 46,7796 -12,8796

24,0 31,6 40,1556 -8,55561

25,0 28,7 34,746 -6,04605

26,0 26,7 29,9981 -3,29808

27,0 25,1 26,1075 -1,00746

28,0 29,0 23,0012 5,99884

29,0 39,7 22,6571 17,0429

30,0 42,4 26,9706 15,4294

------------------------------------------------------------------------------

Lower 95,0% Upper 95,0%

Period Forecast Limit Limit

------------------------------------------------------------------------------

31,0 25,1487 0,877376 49,4199

------------------------------------------------------------------------------

Forecast Summary

----------------

Forecast model selected: Brown's linear exp. smoothing with alpha = 0,2

Number of forecasts generated: 1

Number of periods withheld for validation: 0

Estimation Validation

Statistic Period Period

--------------------------------------------

MSE 153,351

MAE 10,6951

MAPE 23,2155

ME 0,83797

MPE 0,245385

The StatAdvisor

---------------

The table also summarizes the performance of the currently selected

model in fitting the previous data. It displays:

(1) the mean squared error (MSE)

(2) the mean absolute error (MAE)

(3) the mean absolute percentage error (MAPE)

(4) the mean error (ME)

(5) the mean percentage error (MPE)

Приложение №9

(Quadratic Exp. Smoothing)

|

t |

Y |

|

= 0,1 |

= 0,2 |

= 0,3 |

= 0,4 |

= 0,5 |

= 0,6 |

= 0,7 |

= 0,8 |

= 0,9 |

|

1 |

30,0 |

|

35,5 |

23,2 |

26,3 |

28,8 |

28,9 |

27,5 |

24,8 |

21,0 |

16,0 |

|

2 |

37,4 |

|

31,8 |

22,1 |

26,0 |

28,3 |

28,7 |

28,6 |

28,8 |

29,9 |

32,6 |

|

3 |

31,9 |

|

31,2 |

26,6 |

33,6 |

38,1 |

40,9 |

43,5 |

46,2 |

48,9 |

51,2 |

|

4 |

36,7 |

|

29,2 |

26,7 |

32,4 |

34,1 |

33,4 |

31,5 |

28,6 |

24,5 |

19,4 |

|

5 |

41,0 |

|

29,1 |

30,1 |

36,5 |

38,6 |

39,0 |

39,4 |

40,4 |

42,4 |

46,0 |

|

6 |

43,7 |

|

30,5 |

35,2 |

42,2 |

44,5 |

45,4 |

46,1 |

46,8 |

47,2 |

46,8 |

|

7 |

49,7 |

|

32,6 |

40,1 |

46,8 |

48,4 |

48,5 |

48,2 |

47,6 |

46,7 |

45,6 |

|

8 |

53,9 |

|

36,1 |

46,8 |

53,6 |

55,2 |

55,6 |

55,9 |

56,2 |

56,8 |

57,7 |

|

9 |

57,4 |

|

40,3 |

53,3 |

59,4 |

60,2 |

60,0 |

59,6 |

59,0 |

58,4 |

57,6 |

|

10 |

67,6 |

|

44,8 |

59,1 |

63,8 |

63,6 |

62,7 |

61,8 |

61,0 |

60,4 |

60,1 |

|

11 |

63,9 |

|

51,5 |

68,3 |

73,5 |

74,5 |

75,4 |

76,6 |

78,2 |

80,1 |

82,3 |

|

12 |

71,8 |

|

55,8 |

71,1 |

72,8 |

70,4 |

67,5 |

64,4 |

61,0 |

56,9 |

52,0 |

|

13 |

79,3 |

|

61,5 |

76,8 |

77,9 |

76,4 |

75,7 |

76,0 |

77,5 |

80,4 |

84,8 |

|

14 |

81,3 |

|

68,3 |

84,0 |

85,3 |

85,0 |

85,6 |

86,8 |

88,1 |

89,0 |

88,7 |

|

15 |

59,6 |

|

74,2 |

88,8 |

88,6 |

87,3 |

86,4 |

85,5 |

84,1 |

82,1 |

79,8 |

|

16 |

64,2 |

|

72,3 |

77,7 |

68,8 |

59,4 |

50,8 |

42,4 |

34,4 |

26,8 |

20,1 |

|

17 |

67,9 |

|

71,9 |

72,9 |

63,4 |

57,4 |

55,4 |

56,9 |

61,8 |

70,0 |

81,3 |

|

18 |

78,8 |

|

72,6 |

71,7 |

64,5 |

62,9 |

65,3 |

69,6 |

73,9 |

76,6 |

76,1 |

|

19 |

64,6 |

|

76,3 |

77,2 |

75,1 |

78,6 |

84,4 |

89,8 |

93,4 |

95,1 |

95,6 |

|

20 |

45,7 |

|

74,9 |

71,7 |

66,7 |

65,4 |

63,6 |

59,2 |

52,3 |

43,8 |

34,7 |

|

21 |

41,0 |

|

67,9 |

56,6 |

46,0 |

39,1 |

32,3 |

25,6 |

20,2 |

17,3 |

17,9 |

|

22 |

36,8 |

|

60,8 |

44,6 |

33,6 |

28,7 |

26,6 |

27,2 |

30,7 |

36,8 |

43,9 |

|

23 |

33,9 |

|

53,7 |

35,1 |

26,4 |

24,9 |

26,5 |

29,8 |

33,4 |

35,9 |

35,9 |

|

24 |

31,6 |

|

47,2 |

28,3 |

22,8 |

24,4 |

27,8 |

31,0 |

33,0 |

33,3 |

32,7 |

|

25 |

28,7 |

|

41,3 |

23,5 |

21,4 |

24,9 |

28,5 |

30,6 |

31,1 |

30,7 |

30,2 |

|

26 |

26,7 |

|

39,6 |

16,7 |

13,8 |

19,7 |

26,4 |

30,8 |

32,0 |

31,0 |

29,6 |

|

27 |

25,1 |

|

37,8 |

9,4 |

5,6 |

14,4 |

25,0 |

32,2 |

34,3 |

32,5 |

29,8 |

|

28 |

29 |

|

35,9 |

1,7 |

-3,2 |

9,0 |

24,1 |

34,9 |

38,1 |

35,2 |

30,9 |

|

29 |

39,7 |

|

33,9 |

-6,4 |

-12,5 |

3,6 |

23,9 |

38,8 |

43,3 |

39,1 |

32,8 |

|

30 |

42,4 |

|

31,9 |

-15,0 |

-22,3 |

-2,0 |

24,3 |

44,0 |

50,0 |

44,3 |

35,6 |

|

|

|

Кт = |

0,305 |

1,083 |

1,236 |

0,831 |

0,328 |

0,138 |

0,219 |

0,144 |

0,152 |

|

|

|

S^2 = |

256,9 |

131,4 |

91,1 |

94,0 |

108,0 |

127,9 |

154,6 |

192,5 |

251,9 |

|

|

|

|

16,03 |

11,46 |

9,54 |

9,69 |

10,39 |

11,31 |

12,43 |

13,87 |

15,87 |

Приложение № 10

(Quadratic Exp. Smoothing)

Forecast Table for Y

Model: Brown's quadratic exp. smoothing with alpha = 0,6

Period Data Forecast Residual

------------------------------------------------------------------------------

1,0 30,0 27,4744 2,52556

2,0 37,4 28,5612 8,83884

3,0 31,9 43,4951 -11,5951

4,0 36,7 31,4951 5,20485

5,0 41,0 39,4228 1,57717

6,0 43,7 46,1478 -2,44782

7,0 49,7 48,1613 1,53869

8,0 53,9 55,8777 -1,97768

9,0 57,4 59,5684 -2,16845

10,0 67,6 61,7544 5,84562

11,0 63,9 76,571 -12,671

12,0 71,8 64,4498 7,35016

13,0 79,3 76,0236 3,27638

14,0 81,3 86,8074 -5,50737

15,0 59,6 85,5111 -25,9111

16,0 64,2 42,4401 21,7599

17,0 67,9 56,9032 10,9968

18,0 78,8 69,607 9,19303

19,0 64,6 89,7542 -25,1542

20,0 45,7 59,1939 -13,4939

21,0 41,0 25,6303 15,3697

22,0 36,8 27,1892 9,61085

23,0 33,9 29,8081 4,09195

24,0 31,6 31,0192 0,580791

25,0 28,7 30,5521 -1,85209

26,0 26,7 27,4394 -0,739404

27,0 25,1 25,5611 -0,461111

28,0 29,0 24,217 4,78305

29,0 39,7 32,4863 7,21367

30,0 42,4 50,869 -8,46897

------------------------------------------------------------------------------

Lower 95,0% Upper 95,0%

Period Forecast Limit Limit

------------------------------------------------------------------------------

31,0 65,6634 45,3673 85,9594

------------------------------------------------------------------------------

Forecast Summary

----------------

Forecast model selected: Brown's quadratic exp. smoothing with alpha = 0,6

Number of forecasts generated: 1

Number of periods withheld for validation: 0

Estimation Validation

Statistic Period Period

--------------------------------------------

MSE 107,232

MAE 7,74017

MAPE 15,6366

ME 0,243629

MPE 1,03833

The StatAdvisor

---------------

The table also summarizes the performance of the currently selected

model in fitting the previous data. It displays:

(1) the mean squared error (MSE)

(2) the mean absolute error (MAE)

(3) the mean absolute percentage error (MAPE)

(4) the mean error (ME)

(5) the mean percentage error (MPE)

Приложение № 11

Y1 Y2

1 30,000 81,300

2 37,400 59,600

3 31,900 64,200

4 36,700 67,900

5 41,000 78,800

6 43,700 64,600

7 49,700 45,700

8 53,900 41,000

9 57,400 36,800

10 67,600 33,900

11 63,900 31,600

12 71,800 28,700

13 79,300

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

51,10000 |

52,84167 |

-,250466 |

23 |

,804451 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

13 |

12 |

16,00776 |

18,74418 |

1,371109 |

,594767 |

Fтабл(0,05;11;12)=2,72

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 59,600

2 37,400 64,200

3 31,900 67,900

4 36,700 78,800

5 41,000 64,600

6 43,700 45,700

7 49,700 41,000

8 53,900 36,800

9 57,400 33,900

10 67,600 31,600

11 63,900 28,700

12 71,800

13 79,300

14 81,300

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

53,25714 |

50,25455 |

,430157 |

23 |

,671085 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

14 |

11 |

17,36901 |

17,26640 |

1,011921 |

1,000000 |

Fтабл(0,05;13;10)=2,887

tтабл(0,05;23)=2,0686

Приложение № 12

Y1 Y2

1 30,000 64,200

2 37,400 67,900

3 31,900 78,800

4 36,700 64,600

5 41,000 45,700

6 43,700 41,000

7 49,700 36,800

8 53,900 33,900

9 57,400 31,600

10 67,600 28,700

11 63,900

12 71,800

13 79,300

14 81,300

15 59,600

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

53,68000 |

49,32000 |

,619086 |

23 |

,541944 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

15 |

10 |

16,81713 |

17,90474 |

1,133527 |

,804102 |

Fтабл(0,05;9;14)=2,646

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 67,900

2 37,400 78,800

3 31,900 64,600

4 36,700 45,700

5 41,000 41,000

6 43,700 36,800

7 49,700 33,900

8 53,900 31,600

9 57,400 28,700

10 67,600

11 63,900

12 71,800

13 79,300

14 81,300

15 59,600

16 64,200

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

54,33750 |

47,66667 |

,937866 |

23 |

,358058 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

16 |

9 |

16,45839 |

18,16315 |

1,217889 |

,705650 |

Fтабл(0,05;8;15)=2,641

tтабл(0,05;23)=2,0686

Приложение №13

Y1 Y2

1 30,000 78,800

2 37,400 64,600

3 31,900 45,700

4 36,700 41,000

5 41,000 36,800

6 43,700 33,900

7 49,700 31,600

8 53,900 28,700

9 57,400

10 67,600

11 63,900

12 71,800

13 79,300

14 81,300

15 59,600

16 64,200

17 67,900

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

55,13529 |

45,13750 |

1,396276 |

23 |

,175963 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

17 |

8 |

16,27171 |

17,64183 |

1,175494 |

,738682 |

Fтабл(0,05;7;16)=2,66

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 64,600

2 37,400 45,700

3 31,900 41,000

4 36,700 36,800

5 41,000 33,900

6 43,700 31,600

7 49,700 28,700

8 53,900

9 57,400

10 67,600

11 63,900

12 71,800

13 79,300

14 81,300

15 59,600

16 64,200

17 67,900

18 78,800

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

56,45000* |

40,32857* |

2,309429* |

23* |

,030245* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

18* |

7* |

16,74235* |

12,13531* |

1,903404* |

,437201* |

Fтабл(0,05;17;6)=3,91

tтабл(0,05;23)=2,0686

Приложение №14

Y1 Y2

1 30,000 45,700

2 37,400 41,000

3 31,900 36,800

4 36,700 33,900

5 41,000 31,600

6 43,700 28,700

7 49,700

8 53,900

9 57,400

10 67,600

11 63,900

12 71,800

13 79,300

14 81,300

15 59,600

16 64,200

17 67,900

18 78,800

19 64,600

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

56,87895* |

36,28333* |

2,975619* |

23* |

,006766* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

19* |

6* |

16,37771* |

6,265913* |

6,831843* |

,042820* |

Fтабл(0,05;18;5)=4,58

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 41,000

2 37,400 36,800

3 31,900 33,900

4 36,700 31,600

5 41,000 28,700

6 43,700

7 49,700

8 53,900

9 57,400

10 67,600

11 63,900

12 71,800

13 79,300

14 81,300

15 59,600

16 64,200

17 67,900

18 78,800

19 64,600

20 45,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

56,32000* |

34,40000* |

2,962506* |

23* |

,006977* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

20* |

5* |

16,13569* |

4,740781* |

11,58446* |

,028721* |

Fтабл(0,05;19;4)=5,81

tтабл(0,05;23)=2,0686

Приложение №15

Y1 Y2

1 30,000 79,300

2 37,400 81,300

3 31,900 59,600

4 36,700 64,200

5 41,000 67,900

6 43,700 78,800

7 49,700 64,600

8 53,900 45,700

9 57,400 41,000

10 67,600 36,800

11 63,900 33,900

12 71,800 31,600

13 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

48,75000 |

54,87692 |

-,895097 |

23 |

,380007 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

12 |

13 |

14,18536 |

19,38853 |

1,868138 |

,310251 |

Fтабл(0,05;12;11)=2,788

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 71,800

2 37,400 79,300

3 31,900 81,300

4 36,700 59,600

5 41,000 64,200

6 43,700 67,900

7 49,700 78,800

8 53,900 64,600

9 57,400 45,700

10 67,600 41,000

11 63,900 36,800

12 33,900

13 31,600

14 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

46,65455 |

56,08571 |

-1,40205 |

23 |

,174252 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

11 |

14 |

12,78228 |

19,16912 |

2,248990 |

,204734 |

Fтабл(0,05;13;10)=2,89

tтабл(0,05;23)=2,0686

Приложение №16

Y1 Y2

1 30,000 63,900

2 37,400 71,800

3 31,900 79,300

4 36,700 81,300

5 41,000 59,600

6 43,700 64,200

7 49,700 67,900

8 53,900 78,800

9 57,400 64,600

10 67,600 45,700

11 41,000

12 36,800

13 33,900

14 31,600

15 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

44,93000 |

56,60667 |

-1,75046 |

23 |

,093369 |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

10 |

15 |

12,04953 |

18,58169 |

2,378100 |

,194169 |

Fтабл(0,05;14;9)=3,025

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 67,600

2 37,400 63,900

3 31,900 71,800

4 36,700 79,300

5 41,000 81,300

6 43,700 59,600

7 49,700 64,200

8 53,900 67,900

9 57,400 78,800

10 64,600

11 45,700

12 41,000

13 36,800

14 33,900

15 31,600

16 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

42,41111* |

57,29375* |

-2,27232* |

23* |

,032731* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

9* |

16* |

9,589636* |

18,16078* |

3,586450* |

,073883* |

Fтабл(0,05;15;8)=3,22

tтабл(0,05;23)=2,0686

Приложение №17

Y1 Y2

1 30,000 57,400

2 37,400 67,600

3 31,900 63,900

4 36,700 71,800

5 41,000 79,300

6 43,700 81,300

7 49,700 59,600

8 53,900 64,200

9 67,900

10 78,800

11 64,600

12 45,700

13 41,000

14 36,800

15 33,900

16 31,600

17 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

40,53750* |

57,30000* |

-2,54446* |

23* |

,018120* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

8* |

17* |

8,306097* |

17,58412* |

4,481746* |

,051883* |

Fтабл(0,05;16;7)=3,49

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 53,900

2 37,400 57,400

3 31,900 67,600

4 36,700 63,900

5 41,000 71,800

6 43,700 79,300

7 49,700 81,300

8 59,600

9 64,200

10 67,900

11 78,800

12 64,600

13 45,700

14 41,000

15 36,800

16 33,900

17 31,600

18 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

38,62857* |

57,11111* |

-2,74979* |

23* |

,011410* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

7* |

18* |

6,817554* |

17,07791* |

6,274981* |

,031526* |

Fтабл(0,05;17;6)=3,91

tтабл(0,05;23)=2,0686

Приложение №18

Y1 Y2

1 30,000 49,700

2 37,400 53,900

3 31,900 57,400

4 36,700 67,600

5 41,000 63,900

6 43,700 71,800

7 79,300

8 81,300

9 59,600

10 64,200

11 67,900

12 78,800

13 64,600

14 45,700

15 41,000

16 36,800

17 33,900

18 31,600

19 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

36,78333* |

56,72105* |

-2,84633* |

23* |

,009140* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

6* |

19* |

5,212837* |

16,68361* |

10,24311* |

,017291* |

Fтабл(0,05;18;5)=4,58

tтабл(0,05;23)=2,0686

Y1 Y2

1 30,000 43,700

2 37,400 49,700

3 31,900 53,900

4 36,700 57,400

5 41,000 67,600

6 63,900

7 71,800

8 79,300

9 81,300

10 59,600

11 64,200

12 67,900

13 78,800

14 64,600

15 45,700

16 41,000

17 36,800

18 33,900

19 31,600

20 28,700

STAT. T-test for Independent Samples (lab1.sta)

BASIC Note: Variables were treated as independent samples

STATS

|

Group 1 vs. Group 2 |

Mean Group 1 |

Mean Group 2 |

t-value |

df |

p |

|

Y1 vs. Y2 |

35,40000* |

56,07000* |

-2,73632* |

23* |

,011766* |

|

Group 1 vs. Group 2 |

Valid N Group 1 |

Valid N Group 2 |

Std.Dev. Group 1 |

Std.Dev. Group 2 |

F-ratio variancs |

p variancs |

|

Y1 vs. Y2 |

5* |

20* |

4,428882* |

16,49759* |

13,87564* |

,020472* |

Fтабл(0,05;19;4)=5,8

tтабл(0,05;23)=2,0686

Приложение № 19

Regression Analysis - Linear model: Y = a + b*X

-----------------------------------------------------------------------------

Dependent variable: Y1

Independent variable: t1

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 49,915 7,15553 6,97572 0,0000

Slope 0,155462 0,481333 0,322981 0,7496

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 31,4188 1 31,4188 0,10 0,7496

Residual 6927,28 23 301,186

-----------------------------------------------------------------------------

Total (Corr.) 6958,7 24

Correlation Coefficient = 0,067194

R-squared = 0,451504 percent

Standard Error of Est. = 17,3547

The StatAdvisor

---------------

The output shows the results of fitting a linear model to describe

the relationship between Y1 and t1. The equation of the fitted model

is

Y1 = 49,915 + 0,155462*t1

Since the P-value in the ANOVA table is greater or equal to 0.10,

there is not a statistically significant relationship between Y1 and

t1 at the 90% or higher confidence level.

The R-Squared statistic indicates that the model as fitted explains

0,451504% of the variability in Y1. The correlation coefficient

equals 0,067194, indicating a relatively weak relationship between the

variables. The standard error of the estimate shows the standard

deviation of the residuals to be 17,3547. This value can be used to

construct prediction limits for new observations by selecting the

Forecasts option from the text menu.

Predicted Values

------------------------------------------------------------------------------

95,00% 95,00%

Predicted Prediction Limits Confidence Limits

X Y Lower Upper Lower Upper

------------------------------------------------------------------------------

26,0 53,957 15,1241 92,7899 39,1546 68,7594

27,0 54,1125 14,9364 93,2885 38,4319 69,793

28,0 54,2679 14,7266 93,8092 37,6959 70,8399

29,0 54,4234 14,4953 94,3515 36,9486 71,8981

30,0 54,5788 14,2432 94,9145 36,1918 72,9659

------------------------------------------------------------------------------

The StatAdvisor

---------------

This table shows the predicted values for Y1 using the fitted

model. In addition to the best predictions, the table shows:

(1) 95,0% prediction intervals for new observations

(2) 95,0% confidence intervals for the mean of many observations

The prediction and confidence intervals correspond to the inner and

outer bounds on the graph of the fitted model.

Приложение № 20

Regression Analysis - Exponential model: Y = exp(a + b*X)

-----------------------------------------------------------------------------

Dependent variable: Y1

Independent variable: t1

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 3,87129 0,141687 27,3229 0,0000

Slope 0,00194987 0,00953089 0,204585 0,8397

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 0,00494261 1 0,00494261 0,04 0,8397

Residual 2,71605 23 0,118089

-----------------------------------------------------------------------------

Total (Corr.) 2,721 24

Correlation Coefficient = 0,0426201

R-squared = 0,181647 percent

Standard Error of Est. = 0,343641

The StatAdvisor

---------------

The output shows the results of fitting a exponential model to

describe the relationship between Y1 and t1. The equation of the

fitted model is

Y1 = exp(3,87129 + 0,00194987*t1)

Since the P-value in the ANOVA table is greater or equal to 0.10,

there is not a statistically significant relationship between Y1 and

t1 at the 90% or higher confidence level.

The R-Squared statistic indicates that the model as fitted explains

0,181647% of the variability in Y1 after transforming to a logarithmic

scale to linearize the model. The correlation coefficient equals

0,0426201, indicating a relatively weak relationship between the

variables. The standard error of the estimate shows the standard

deviation of the residuals to be 0,343641. This value can be used to

construct prediction limits for new observations by selecting the

Forecasts option from the text menu.

Predicted Values

------------------------------------------------------------------------------

95,00% 95,00%

Predicted Prediction Limits Confidence Limits

X Y Lower Upper Lower Upper

------------------------------------------------------------------------------

26,0 50,5008 23,4075 108,953 37,6708 67,7003

27,0 50,5993 23,2944 109,91 37,0937 69,0223

28,0 50,6981 23,1717 110,924 36,5158 70,3886

29,0 50,797 23,0398 111,995 35,9389 71,798

30,0 50,8962 22,8991 113,123 35,3644 73,2495

------------------------------------------------------------------------------

The StatAdvisor

---------------

This table shows the predicted values for Y1 using the fitted

model. In addition to the best predictions, the table shows:

(1) 95,0% prediction intervals for new observations

(2) 95,0% confidence intervals for the mean of many observations

The prediction and confidence intervals correspond to the inner and

outer bounds on the graph of the fitted model.

Приложение № 21

Regression Analysis - Double reciprocal model: Y = 1/(a + b/X)

-----------------------------------------------------------------------------

Dependent variable: Y1

Independent variable: t1

-----------------------------------------------------------------------------

Standard T

Parameter Estimate Error Statistic P-Value

-----------------------------------------------------------------------------

Intercept 0,0190765 0,00164577 11,5912 0,0000

Slope 0,015485 0,00649388 2,38455 0,0257

-----------------------------------------------------------------------------

Analysis of Variance

-----------------------------------------------------------------------------

Source Sum of Squares Df Mean Square F-Ratio P-Value

-----------------------------------------------------------------------------

Model 0,000245363 1 0,000245363 5,69 0,0257

Residual 0,000992483 23 0,0000431514

-----------------------------------------------------------------------------

Total (Corr.) 0,00123785 24

Correlation Coefficient = 0,445217

R-squared = 19,8218 percent

Standard Error of Est. = 0,00656898

The StatAdvisor

---------------

The output shows the results of fitting a double reciprocal model

to describe the relationship between Y1 and t1. The equation of the

fitted model is

Y1 = 1/(0,0190765 + 0,015485/t1)

Since the P-value in the ANOVA table is less than 0.05, there is a

statistically significant relationship between Y1 and t1 at the 95%

confidence level.

The R-Squared statistic indicates that the model as fitted explains

19,8218% of the variability in Y1 after transforming to a reciprocal

scale to linearize the model. The correlation coefficient equals

0,445217, indicating a relatively weak relationship between the

variables. The standard error of the estimate shows the standard

deviation of the residuals to be 0,00656898. This value can be used

to construct prediction limits for new observations by selecting the

Forecasts option from the text menu.

Predicted Values

------------------------------------------------------------------------------

95,00% 95,00%

Predicted Prediction Limits Confidence Limits

X Y Lower Upper Lower Upper

------------------------------------------------------------------------------

26,0 50,8335 29,7488 174,54 43,8735 60,4181

27,0 50,8906 29,7665 175,28 43,8978 60,5334

28,0 50,9437 29,7829 175,973 43,9202 60,641

29,0 50,9932 29,7981 176,624 43,941 60,7419

30,0 51,0395 29,8124 177,237 43,9603 60,8366

------------------------------------------------------------------------------

The StatAdvisor

---------------

This table shows the predicted values for Y1 using the fitted

model. In addition to the best predictions, the table shows:

(1) 95,0% prediction intervals for new observations

(2) 95,0% confidence intervals for the mean of many observations

The prediction and confidence intervals correspond to the inner and