80

companies.

4.6.1.4 Debt finance via bond issuance

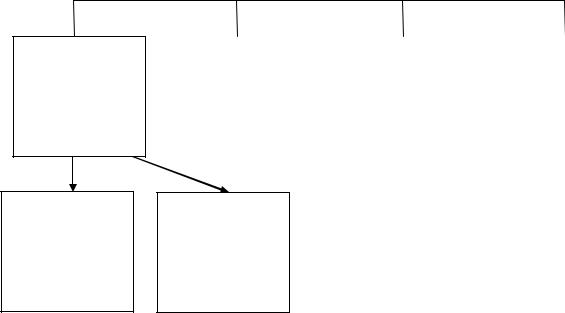

In addition to the credit facilities mentioned above, large companies can also raise funds in the capital markets by issuing debt instruments known as bonds.2 Bonds are simply contracts between a lender and borrower by which the borrower promises to repay a loan with interest. Typically, bonds are traded in the market after issue so their price and yields vary. Bonds can take on various features and a classification of bond types depends on the issuer, priority, coupon rate and redemption features as shown in Figure 4.2.

Large companies as well as governments and international organisations all issue bonds to raise mediumto long-term finance. The most important feature relating to a bond is the credit quality of the issuer - typically governments (especially in the developed world) are believed to be lower risk than firms and so their bonds pay lower interest than those of commercial concerns. However, since some of the world's largest companies have better credit ratings than some fragile economies, this means that the former can raise bond finance cheaper than the latter. Nearly all bond issuers have to be credit rated in order to assess their ability to make interest (and ultimately principal) payments for their bond financing. The credit rating process is the same as that outlined for syndicated credits and shown in Table 4.1.

There are many types of corporate bonds that a firm can issue. It can raise funds in its home market (and currency) by issuing domestic bonds, or it maywish to issue an international bond the main types of which include:

•Eurobonds - any bond that is denominated in a currency other than that of the country in which it is issued. Bonds in the Eurobond market are classified according to the currency in which they are denominated. So, for example, a Eurobond denominated in US dollars issued in Japan (or anywhere outside the US) would be known as a Eurodollar bond.

•Foreign bonds - denominated in the currency of the country into which a foreign entity issues the bond. For instance a yen-denominated bond issued in Japan by a US firm is (a foreign bond) known as a Samurai bond. Similarly, a UK firm issuing a dollar bond in the US is known as a Yankee bond, and a French firm issuing a sterling bond in the UK is known as a Bulldog bond.

Figure 4.2 Bond features

Bond characteristics

81

Issuer

•Corporation

•Municipality

•Government

•International

US Government treasuries

•Bond (1Oyrs+)

•Note (1-10 yrs)

•T-Bill (<1 yr)

|

|

|

|

|

|

|

|

|

|

|

|

|

Priority |

|

|

|

Coupon rate |

|

|

|

Redemption |

|

|

|

|

|

|

|

|

|

|

|

|

features |

|

|

• Junior or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• Fixed income |

|

|

|

|

|||

|

|

|

|

|

|

|

• Callable |

||||

|

Subordinated |

|

|

|

|

• Floater |

|

|

|||

|

|

|

|

|

|

• Convertible |

|||||

|

• Senior or |

|

|

• Inverse floater |

|

|

|||||

|

|

|

|

|

• Puttable |

||||||

|

Unsubordinated |

|

|

• Zero coupon |

|

|

|||||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

International bond issues

•Eurobond

•Foreign

•Global

•Global bonds - can be issued in both foreign and Eurobond markets. In general, a global bond is similar to a Eurobond but it can be offered within the country whose currency is used to denominate the bond. For example, a global bond denominated in dollars could be sold either in the US or any other country through the Eurobond market.

Companies have therefore a broad range of bond types with which they can raise debt finance. In addition to the creditworthiness of the borrower, bonds are characterised by their priority, coupon rate and redemption features.

The priority of the bond relates to the holder of the bond's repayment standing in the event that the issuer defaults on payments. Bonds that are classified as senior debt (otherwise known as unsubordinated debt) mean that the holders of such bonds are first in line to receive payment if the company defaults and payment is to be made from a liquidation of assets. In contrast, junior (or subordinated) bondholders would receive payment after senior bond investors - as such this form of debt is more risky and commands a higher premium than senior debt.

Companies can choose a variety of types of interest payments, or coupons, to pay on their bonds. The traditional (or plain vanilla) bond just pays a fixed rate semiannual coupon over the life of the bond and the last payment will include both the final coupon payment and the repayment of principal (which is the par value of the bond). In addition, the coupon can be set at a floating rate, usually relating to LIBOR or some other variable market rate.

Both bond investors and issuers are exposed to interest rate risk since they are locked into either receiving or paying a set coupon rate over a specified period of

82

time. For this reason, various types of bonds offer additional redemption features in order to minimise these risks. For example, there are callable bonds that give the issuer the right but not the obligation to redeem their issue of bonds before the bond's maturity date. In this case the issuer of the bond has to pay the bondholders a premium to compensate the holder for the fact that the bond may be redeemed before maturity. For American callable bonds the bond can be redeemed at any date (after a set period) whereas European callable bonds can only be redeemed on dates specified by the issuer. Typically, an issuer will redeem its bonds when current interest rates are lower than that being paid on its bonds - so the firm could redeem its bonds and make a new issue at a lower coupon rate. There are also puttable bonds that give holders the right to sell back the bonds to the issuer at a predetermined price and date.

Another type of bond is the convertible bond that gives holders the right but not the obligation to convert their bonds into a predetermined number of shares at a set date before maturity.

4.6.1.5 Other debt finance including asset-backed financing

The access to external finance is a critical success ingredient in the development of any business. Traditional bank loan and overdraft finance are the main sources of external finance for relatively small firms that conduct international business, whereas bond and syndicated loans form a major feature of multinational financing. In addition to these sources of debt finance, all firms (irrespective of size) have access to other forms of debt finance that can involve both domestic and/or international relationships and they include:

•asset-based finance; and

•factoring and invoice discounting.

As introduced in Section 3.5.1, asset-based finance encompasses both leasing and hire purchase and the main difference between them is that in the former the asset remains the property of the leasing company at the end of the contract, whereas in the case of hire purchase the firm making payments obtains ownership. More formally, a lease is an agreement where the owner conveys to the user the right to use equipment and (say) vehicles in return for a number of specified payments over an agreed period of time. Unlike a bank loan a lease is an asset-based financing product with the equipment leased usually the only collateral security for the transaction. Typically a company will be offered a leasing agreement that covers not only the equipment costs but also the delivery, installation, servicing and insurance.

83

There are two main kinds of leases used by companies:

•Capital or lease finance - a standard finance lease is defined as one which transfers substantially all the risks and rewards inherent in the ownership of the asset to the lessee (the lessee is the user of the leased asset). The risks include any loss in value of the asset value through such things as obsolescence, unsatisfactory performance, wear and tear, and so on. Under the terms of a finance lease, the lessor (the person who rents land or property to a lessee) usually receives lease payments amounting to the full cost of the leased asset, together with a return on the finance that has been provided. This means that the lessor is not exposed to any financial risks associated with the residual value of the asset. Under a finance lease there is no statutory obligation to have a purchase option over the leased asset.

•Operating lease - is any lease other than a finance lease. As such operating leases embrace a broad range of different types of lease in which a substantial proportion of risks and rewards associated with ownership of the asset remain with the lessor. Operating leases have two main features. First, they have a noncancellable lease period that is much shorter than the life of the asset. Second, the lessee has little or no interest in the residual value of the asset at the end of the lease. The residual guarantees from the proceeds of the sale of the asset -which is a hallmark of many finance leases (think about car finance leases) – are absent in the case of standard operating leases. Again there is no statutory obligation to have a purchase option over the leased asset.

Hire purchase differs from lease contracts in that customers pay for the cost of the asset, together with the financing charges, over the hire period and take legal title on the equipment at the time of final payment (or there may be a nominal purchase option fee at the end of the payment period). For tax and accounting purposes the customer in a hire purchase agreement is treated as the owner from the outset and this allows them to claim capital allowances for taxation purposes and they can also report the asset on the company's balance sheet. The main attractions of leasing are as follows:

•As the bank/finance company holds title to the asset while repayments remain outstanding, and the asset belongs to the bank/finance company should the j company go bankrupt, the bank or finance company has some assurance that I payments will be maintained by the customer (even if this relates to the return of the asset being financed).

•Bank overdraft or loan facilities may not be available of the size required to finance outright purchase of the asset. A lease agreement provides

84

up-front finance for the whole cost of the asset subject to one advance or rental. More important though, a lease once obtained will provide guaranteed continuity of credit over the agreed hire period. In contrast, an overdraft facility can be withdrawn at short notice.

• Companies are able to avoid tying up their working capital by using leasing agreements.

• There may be certain tax advantages associated with lease finance compared with outright purchase of assets and this is a more important consideration for 'Bigticket' lease deals (as in such things as aircraft and computer systems leasing).

The main disadvantages of lease finance relate to the typically higher costs compared with traditional bank funding and the fact that the firm does not own the asset, thereby reducing the value of company fixed assets.

Other sources of finance for companies are through the use of factoring and invoice discounting services. As illustrated in Section 3.5.1, factoring is a lending product that enables a company to collect money on credit sales. The factor purchases the company's invoice debts for cash, but at a discount, and subsequently seeks repayment from the original purchaser of the company's goods or services. Factoring involves the factor managing the sales ledger of a company whereas invoice discounting is a narrower service where the discounting firm collects sales receipts but the firm still manages its ledger.

Factors and invoice discounters charge for providing an advance to the company and this is usually around 80 per cent of the total value of the invoices. When the factor/invoice discounter receives the invoice payments they release the 20 per cent residual to the client, less charges. The main charges are: an administration charge sometimes called a service or commission charge; and a discounting or finance charge (i.e., interest). Factors make administration charges for collecting debt contained in invoices and for credit management/sales ledger on behalf of clients. In the United Kingdom, they typically charge around 1-3 per cent of invoice values. As already mentioned, invoice discounters also advance funds against clients' invoices, but unlike factors, they do not provide administration services. A factor or discounter may have recourse to the client when a customer of that client refuses to pay an invoice that has been factored - this is known as recourse factoring. If there is no recourse then the service is known as non-recourse factoring. In the latter case, the factor will charge the client for insurance against bad debt.