2.5 Swaps

Swaps are transactions in which two parties agree to exchange payment streams based on a specified notional amount for a specified period. These streams are called the legs of the swap.

Usually, at least one of the legs has a rate that is variable.

The most important criterion is that it comes from an independent third party, to avoid any conflict of interest. For instance, LIBOR (London Interbank Offered Rate)

Swaps can be used to hedge certain risks or to speculate on changes in the underlying prices. Most swaps are traded over-the-counter (OTC), "tailor-made" for the counterparties. Some types of swaps are also exchanged on futures markets.

The five generic types of swaps, in order of their quantitative importance, are:

Interest rate swaps,

currency swaps,

credit swaps,

commodity swaps and

equity swaps.

Under an interest rate swap counterparties agree to pay either a fixed or floating rate denominated in a particular currency to the other counterparty. The fixed or floating rate is multiplied by a notional principal amount. This notional amount is generally not exchanged between counterparties, but is used only for calculating the size of cash flows to be exchanged.

By far the most common are fixed-for-floating or floating-for-floating swaps. The legs of the swap can be in the same currency or in different currencies (a sort of combination with a currency swap).

Fixed-for-fixed swaps in different currencies are also quite common. It is a form of a currency swap, to be discussed later. Thus it generally exists only in different currencies and helps to reduce the currency risk.

A currency swap (or cross currency swap) is a foreign exchange agreement between two parties to exchange a given amount of one currency for another and, after a specified period of time, to give back the original amounts swapped. Unlike interest rate swaps, currency swaps involve the exchange of the principal amount.

An equity swap is a swap where a set of future cash flows are exchanged between two counterparties. One of these cash flow streams will typically be based on a reference interest rate. The other will be based on the performance of a share of stock or stock market index.

A credit default swap (CDS) is a credit derivative between two counterparties, whereby one makes periodic payments to the other and receives the promise of a payoff if a third party defaults. The party that makes payments receives credit protection and is said to be the buyer, whilst the other party provides credit protection and is said to be the seller. The third party is called a reference entity.

Simply put, the risk of default is transferred from the holder of the fixed income security to the seller of the swap. Credit default swaps resemble an insurance policy, as they can be used by debt owners to hedge, or insure against credit events such as a default on a debt obligation.

A total return swap (TRORS) is a swap in which party A pays the total return of an asset, and party B makes periodic interest payments. The total return is the capital gain or loss, plus any interest or dividend payments. Note that if the total return is negative, then party A receives this amount from party B.

The TRORS, then, allows one party to derive the economic benefit of owning an asset without putting that asset on its balance sheet, and allows the other (which does retain that asset on its balance sheet) to buy protection against a potential decline in its value.

5. World

derivatives market

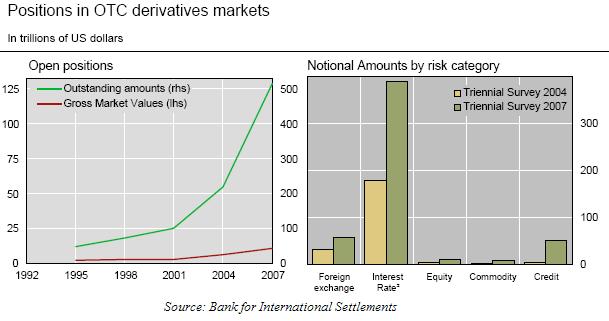

According to the survey by Bank for International Settlements, positions in the OTC derivatives market increased at a rapid pace during the last 3 years. Notional amounts outstanding of such instruments totaled $516 trillion at the end of June 2007, 135% higher than the level recorded in the 2004.ii

The statistical surveys shows that the volumes of both OTC and ET derivatives markets show exponential growth and are likely to continue enlarging with a rapid pace in future.