vk.com/id446425943

Russia

Energy: Integrated Oil & Gas

21 December 2018

Equities

Change of Recommendation

Russian Oil and Gas

Go after the oil price

The drop in oil prices (Brent has lost 35% since its October peak) has led to a tangible downward move in the futures curve. This, coupled with the relatively stable RUB rate, is to hit Russian oils’ profitability as early as in 4Q18, we believe. Having incorporated the up-to-date oil futures curve and the recent OPEC+ crude output cuts, we have downgraded the Russian oil sector to Sell and revised our 12-month Target Prices down 13-36%. Gazprom Neft, Surgut ords, Tatneft ords are Sells. Gazprom ords and Surgut prefs (on the stock performance, as they are up against peers since November) and Tatneft prefs are downgraded to Hold. Lukoil is kept on Hold thanks to the ongoing buyback and existing dividend policy.

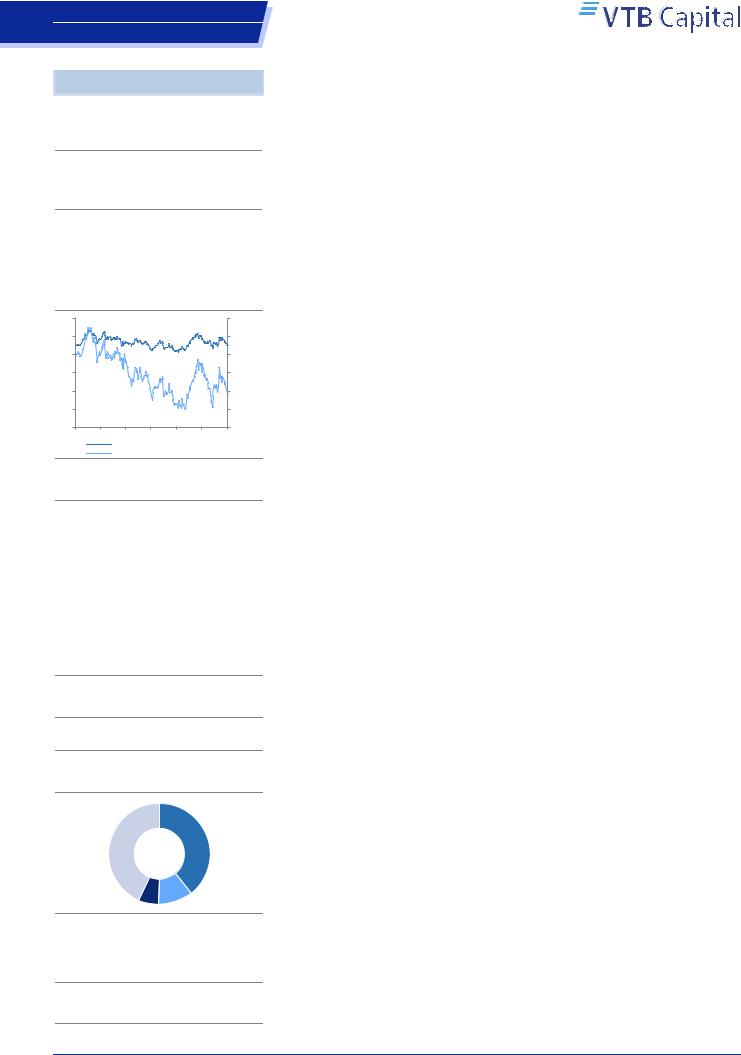

Shift down in oil futures curve is now in our models. We incorporate the up-to-date Brent futures curve (as reported by Bloomberg) and the respective RUB rates into our oil company models (Figure 1), as well as the OPEC+ production cut. As a result, we are downgrading Gazprom, Surgut prefs and Tatneft prefs to Hold from Buy (with new TPs of USD 2.30, USD 0.55 and USD 8.20, respectively), as well as Gazprom Neft and Surgut ords to Sell from Hold (USD 4.70 and USD 0.36), and reiterating our Sell for Tatneft ords (USD 7.00). Although we are cutting our TP for Lukoil 16% to USD 71, the ongoing buyback as well as the existing dividend policy (which implies growing DPS in RUB terms despite the decrease in the EPS) is set to provide good support for the stock, we think. Therefore, we rank Lukoil and Surgut prefs (due to the implied 17% DY) as better than the others.

Oil down 35%, but RTS O&G just 12%. We think the market might underestimate Russian oil names’ sensitivity to oil prices from their much increased exposure to numerous tax-breaks (see our Russian Oils Upstream - The Metamorphoses. Rise of Titans, of 5 October). Also, the OPEC+ agreement is likely to be destructive for select names (Tatneft’s TPs are down more than peers’ due to the much greater downward revision to crude production vs. the company’s guidance – see our Oil Sector – Update on the production cut renewal, of 12 December). The conversion of negative floating excise from subsidy into additional tax (see our Russian Oils Downstream - Merry Floating and a Happy New Year, of 19 December) is to be painful for companies with domestic market exposure. The surprising resilience of the local currency (at least partially motivated by the recent apparent lightening of sanctions pressures) is onerous for all exporters. All these negative factors combined make us to believe that the entire Russian O&G sector is vulnerable to downward repricing, unless oil prices recover back to USD 6570/bbl. This is the key risk to our investment case for the sector.

Dmitry Loukashov, CFA, Equities Analyst

+7 495 663 46 34 // dmitry.loukashov@vtbcapital.com

Ekaterina Rodina, Equities Analyst

+7 495 663 47 33 // ekaterina.rodina@vtbcapital.com

Alexander Donskoy, Equities Analyst

+7 495 660 67 88 // alexander.donskoy@vtbcapital.com

Artur Muradyants, Equity analyst

+7 495 663 46 38 // artur.muradyants@vtbcapital.com

Aydar Safin, Equities Analyst

+7 495 663 46 32 // aydar.safin@vtbcapital.com

Prices cited in the body of this report are as of the last close before, or the close on, 19 Dec 2018 (except where indicated otherwise). VTB Capital analysts update their recommendations periodically as required. This research report was prepared by the analyst(s) named above who is(are) associated with JSC VTB Capital and is distributed by JSC VTB Capital and VTB Capital PLC and their non-U.S. affiliates outside the United States. This VTB Capital research report is distributed to investors located within United States by Xtellus Capital Partners, Inc. (“Xtellus”) as a “third-party research report” as defined in Rule 2241(a)(14) and Rule 2242(a)(17) of the U.S. Financial Industry Regulatory Authority. Please refer to the Disclosures section of this report for other important disclosures, including the analyst certification and information required by regulation.

vk.com/id446425943 |

Russian Oil and Gas |

|

|

|

|

|

||

|

Russia |

|

|

|

|

|

|

|

|

Energy: Integrated Oil & Gas |

|

|

|

|

|

|

|

|

Companies Stocks mentioned |

|

|

|

|

|

|

|

|

Stock |

Rec. |

Rec. (previous) |

12mo Target |

Last |

ETR |

Upside |

DY, next |

|

|

|

|

Price |

Price |

|

|

12mo |

|

Tatneft DRs |

Sell |

Hold |

42.00 |

62.66 |

-28% |

-33% |

5% |

|

(ATAD LI,USD) |

(13 Nov 2018, 06:11 UTC) |

(19 Feb 2018, 05:02 UTC) |

|

|

|

|

|

|

Gazprom Neft DRs |

Sell |

Hold |

23.50 |

25.50 |

0% |

-8% |

8% |

|

(GAZ LI,USD) |

(from Hold) |

(13 Nov 2018, 06:11 UTC ) |

|

|

|

|

|

|

Gazprom ords |

Hold |

Buy |

2.30 |

2.27 |

8% |

1% |

7% |

|

(GAZP RX,USD) |

(from Buy) |

(19 Feb 2018, 05:02 UTC ) |

|

|

|

|

|

|

Lukoil DRs |

Hold |

Buy |

71.00 |

72.16 |

3% |

-2% |

5% |

|

(LKOD LI,USD) |

(13 Nov 2018, 06:11 UTC) |

(12 Jan 2018, 13:01 UTC) |

|

|

|

|

|

|

Lukoil ords |

Hold |

Buy |

71.00 |

72.82 |

2% |

-2% |

5% |

|

(LKOH RX,USD) |

(13 Nov 2018, 06:11 UTC) |

(12 Jan 2018, 13:01 UTC) |

|

|

|

|

|

|

Gazprom DRs |

Hold |

Buy |

4.60 |

4.49 |

9% |

3% |

7% |

|

(OGZD LI,USD) |

(from Buy) |

(19 Feb 2018, 05:02 UTC ) |

|

|

|

|

|

|

Gazprom Neft ords |

Sell |

Hold |

4.70 |

5.20 |

-2% |

-10% |

8% |

|

(SIBN RX,USD) |

(from Hold) |

(13 Nov 2018, 06:11 UTC ) |

|

|

|

|

|

|

Surgutneftegas ords |

Sell |

Hold |

0.36 |

0.41 |

-11% |

-13% |

2% |

|

(SNGS RX,USD) |

(from Hold) |

(8 Oct 2018, 06:10 UTC ) |

|

|

|

|

|

|

Surgutneftegas prefs |

Hold |

Buy |

0.55 |

0.58 |

11% |

-5% |

17% |

|

(SNGSP RX,USD) |

(from Buy) |

(23 Mar 2017, 12:03 UTC ) |

|

|

|

|

|

|

Tatneft ords |

Sell |

Hold |

7.00 |

10.59 |

-29% |

-34% |

5% |

|

(TATN RX,USD) |

(13 Nov 2018, 06:11 UTC) |

(19 Feb 2018, 05:02 UTC) |

|

|

|

|

|

|

Tatneft prefs |

Hold |

Buy |

8.20 |

7.42 |

18% |

11% |

7% |

|

(TATNP RX,USD) |

(from Buy) |

(30 Mar 2018, 06:03 UTC ) |

|

|

|

|

|

Source: Company data, Bloomberg, VTB Capital Research

Figure 1: Brent Futures Curve

USD/bbl

73

71

69

67

65

63

61

59

57

55

Feb-19 Apr-19 Jun-19 Aug-19 Oct-19 Dec-19 Feb-20 Apr-20 Jun-20 Aug-20 Oct-20 Dec-20 |

Feb-21 Apr-21 Jun-21 Aug-21 Oct-21 Dec-21 Feb-22 Apr-22 Jun-22 Aug-22 Oct-22 Dec-22 Feb-23 |

Brent Futures Curve (18 December) |

Brent Futures Curve (8 Nov) |

Source: Bloomberg, VTB Capital Research

21 December 2018 |

2 |

vk.com/id446425943

Russia

Energy: Integrated Oil & Gas

VTB Capital Facts & Forecasts

Russia

Energy / Integrated Oil & Gas

Gazprom

Prices as of: 19 December 2018

Ticker |

CCY |

Current |

12mo TP |

Rating |

GAZP RX |

USD |

2.27 |

2.30 |

Hold |

Share price performance, 12-mo

3 |

10% |

2.5 |

5% |

2 |

0% |

1.5 |

-5% |

1 |

-10% |

0.5 |

-15% |

0 |

-20% |

Dec Feb Apr Jun Aug Oct Dec

GAZP RX, USD, lhs

Relative to MOEX Index, %, rhs

Company description

Gazprom, Russia's largest gas producer, is controlled by the Russian state. The company accounts for 17% of the world's gas reserves and 72% of Russian gas reserves, producing 12% of all gas worldwide and 68% of that in Russia. In addition, it operates the world's largest gas transmission system. In 2017, the company exported 55% of its gas to Europe and FSU countries, with the other 45% being sold domestically. Apart from the gas business, Gazprom owns 95.7% of Gazprom Neft, one of the largest integrated oil companies in Russia. By the end of the 2000s, it had also gained control over a number of electricity and heat generating companies (Mosenergo, TGK 1 and OGK 2).

Company website

http://www.gazprom.com/

Shareholder structure

Other/Free |

Federal |

|

Agency for |

||

float |

State Property |

|

43% |

Management |

|

|

39% |

|

Treasury |

Rosneftegaz |

|

11% |

||

shares |

||

7% |

|

Source: Company data, VTB Capital Research

Research team

Ekaterina Rodina / +7 495 663 47 33

Aydar Safin / +7 495 663 46 32

Artur Muradyants / +7 495 663 46 38

Russian Oil and Gas

Last model update on: 21 December 2018

|

IFRS |

2016 |

2017 |

2018F |

2019F |

2020F |

|

2021F |

||

|

Company data |

|

|

|

|

|

|

|

|

|

|

Weighted avg # shares, mn |

|

23,674 |

23,674 |

23,674 |

23,674 |

23,674 |

|

23,674 |

|

|

Avg market cap, USD mn |

48,645 |

48,893 |

52,137 |

52,137 |

52,137 |

52,137 |

|

||

|

EV, USD mn |

80,265 |

89,927 |

91,250 |

90,039 |

82,809 |

80,341 |

|

||

|

Ratios & analysis |

|

|

|

|

|

|

|

|

|

|

P/E, x |

|

3.6x |

4.3x |

2.5x |

2.6x |

2.4x |

|

2.5x |

|

|

EV/EBITDA, x |

4.3x |

3.7x |

2.4x |

2.7x |

2.2x |

|

2.3x |

||

|

P/B, x |

|

0.3x |

0.3x |

0.3x |

0.2x |

0.2x |

|

0.2x |

|

|

FCF yield, % |

5.9% |

-7.2% |

8.9% |

7.9% |

21.2% |

15.2% |

|

||

|

Dividend yield (ords), % |

6.4% |

5.8% |

6.1% |

8.3% |

11.3% |

10.6% |

|

||

|

Dividend yield (prefs), % |

|

|

|

|

|

|

|

|

|

|

EPS(ords), USD |

0.60 |

0.52 |

0.92 |

0.88 |

0.96 |

0.90 |

|

||

|

CFPS, USD |

0.99 |

0.86 |

1.52 |

1.41 |

1.52 |

1.50 |

|

||

|

Free CFPS, USD |

0.13 |

(0.16) |

0.20 |

0.18 |

0.48 |

0.34 |

|

||

|

DPS (ords), USD |

0.14 |

0.13 |

0.14 |

0.19 |

0.26 |

0.24 |

|

||

|

Payout ratio (ords), % |

22.0% |

23.2% |

14.1% |

20.0% |

25.0% |

25.0% |

|

||

|

BPS(ords), USD |

7.97 |

8.81 |

8.82 |

9.63 |

10.47 |

11.17 |

|

||

|

Revenues growth, % |

|

-9% |

23% |

16% |

-7% |

4% |

|

0% |

|

|

EBITDA, chg |

|

-32% |

31% |

51% |

-11% |

11% |

|

-4% |

|

|

EPS growth, % |

|

10% |

-14% |

77% |

-4% |

9% |

|

-7% |

|

|

EBIT margin, % |

12% |

13% |

22% |

20% |

20% |

19% |

|

||

|

EBITDA margin, % |

21.2% |

22.7% |

29.5% |

28.3% |

30.3% |

28.8% |

|

||

|

Net margin, % |

15.6% |

10.9% |

16.6% |

17.2% |

18.1% |

16.8% |

|

||

|

ROE, % |

7.8% |

6.1% |

10.8% |

9.5% |

9.6% |

8.4% |

|

||

|

ROIC, % |

2.7% |

3.8% |

8.4% |

6.4% |

6.7% |

5.8% |

|

||

|

Capex/Revenues, % |

22% |

21% |

24% |

24% |

20% |

22% |

|

||

|

Capex/Depreciation, x |

2.4x |

2.3x |

3.1x |

2.7x |

2.0x |

|

2.1x |

||

|

Net debt/Equity, % |

17% |

20% |

19% |

17% |

12% |

11% |

|

||

|

Net debt/EBITDA, x |

1.6x |

1.6x |

1.0x |

1.1x |

0.8x |

|

0.8x |

||

|

Net interest cover, x |

10.1x |

16.3x |

36.2x |

32.4x |

35.3x |

|

32.1x |

||

|

Income statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Revenues |

91,122 |

112,183 |

130,344 |

120,968 |

125,901 |

126,464 |

|

||

|

Cost of sales |

(71,780) |

(86,755) |

(91,934) |

(86,687) |

(87,808) |

(90,073) |

|

||

|

SG&A and other opexp. |

|

|

|

|

|

|

|

|

|

|

EBITDA |

19,342 |

25,428 |

38,410 |

34,281 |

38,093 |

36,391 |

|

||

|

Depreciation & amortization |

|

(8,523) |

(10,508) |

(10,128) |

(10,630) |

(12,344) |

|

(12,989) |

|

|

Operating profit |

10,819 |

14,920 |

28,282 |

23,651 |

25,749 |

23,402 |

|

||

|

Non-operating gains /(exp.) |

|

6,781 |

(170) |

(3,907) |

(348) |

0 |

|

0 |

|

|

EBIT |

10,819 |

14,920 |

28,282 |

23,651 |

25,749 |

23,402 |

|

||

|

Net interest income/(exp.) |

327 |

521 |

331 |

310 |

367 |

695 |

|

||

|

Profit before tax |

19,163 |

17,446 |

27,956 |

26,862 |

29,366 |

27,347 |

|

||

|

Income tax |

(4,295) |

(4,304) |

(5,170) |

(4,968) |

(5,431) |

(5,057) |

|

||

|

Minority interests |

(678) |

(901) |

(1,088) |

(1,046) |

(1,143) |

(1,064) |

|

||

|

Net income |

14,190 |

12,241 |

21,698 |

20,849 |

22,792 |

21,225 |

|

||

|

Cash flow statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash flow from operations |

23,430 |

20,342 |

36,041 |

33,349 |

36,003 |

35,600 |

|

||

|

Working capital changes |

2,725 |

(697) |

- |

477 |

(276) |

321 |

|

||

|

Capex |

(20,414) |

(24,091) |

(31,245) |

(29,088) |

(24,603) |

(27,434) |

|

||

|

Other investing activities |

(2,352) |

1,042 |

(439) |

- |

- |

- |

|

||

|

Free cash flow |

3,016 |

(3,749) |

4,797 |

4,261 |

11,399 |

8,166 |

|

||

|

Dividends paid |

(2,778) |

(3,288) |

(2,842) |

(3,050) |

(4,170) |

(5,698) |

|

||

|

Net change in borrowings |

303 |

7,138 |

(1,574) |

- |

- |

- |

|

||

|

Other financing cash flow |

(4,391) |

(1,280) |

22 |

- |

- |

- |

|

||

|

Movement in cash |

|

(6,894) |

(475) |

1,469 |

1,211 |

7,230 |

|

2,468 |

|

|

Balance sheet summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash and equivalents |

14,841 |

15,138 |

13,482 |

14,693 |

21,923 |

24,391 |

|

||

|

PP&E |

189,636 |

217,796 |

213,114 |

231,572 |

243,831 |

258,276 |

|

||

|

Goodwill |

1,736 |

1,831 |

1,639 |

1,639 |

1,639 |

1,639 |

|

||

|

Investments |

12,227 |

15,599 |

16,456 |

16,456 |

16,456 |

16,456 |

|

||

|

Other assets |

|

60,488 |

66,280 |

67,688 |

65,635 |

66,405 |

|

66,889 |

|

|

Total assets |

|

278,928 |

316,644 |

312,378 |

329,995 |

350,253 |

|

367,650 |

|

|

Interest bearing debt |

|

46,650 |

56,710 |

53,549 |

53,549 |

53,549 |

|

53,549 |

|

|

Other liabilities |

43,647 |

51,333 |

50,035 |

48,459 |

48,952 |

49,757 |

|

||

|

Total liabilities |

90,296 |

108,043 |

103,584 |

102,008 |

102,501 |

103,307 |

|

||

|

Total shareholder's equity |

182,906 |

201,893 |

201,617 |

219,764 |

238,386 |

253,913 |

|

||

|

Minority interest |

5,726 |

6,708 |

7,177 |

8,223 |

9,366 |

10,430 |

|

||

|

Net working capital |

9,878 |

8,973 |

7,195 |

6,619 |

7,077 |

6,932 |

|

||

|

Net Debt |

31,620 |

41,033 |

39,113 |

37,902 |

30,672 |

28,204 |

|

||

|

Capital |

229,556 |

258,603 |

255,166 |

273,313 |

291,935 |

307,462 |

|

||

|

|

|

|

|

|

|

|

|

|

|

21 December 2018 |

3 |

vk.com/id446425943

Russia

Energy: Integrated Oil & Gas

VTB Capital Facts & Forecasts

Russia

Energy / Integrated Oil & Gas

Gazprom Neft

Prices as of: 19 December 2018

Ticker |

CCY |

Current |

12mo TP |

Rating |

SIBN RX |

USD |

5.20 |

4.70 |

Sell |

Share price performance, 12-mo

8 |

30% |

6 |

20% |

4 |

10% |

2 |

0% |

0 |

-10% |

Dec Feb Apr Jun Aug Oct Dec

SIBN RX, USD, lhs

Relative to MOEX Index, %, rhs

Company description

Gazprom Neft is the fourth largest oil producer in Russia. The company's proved oil reserves, according to SPE-PRMS standards, stand at 2.78bn toe, which implies almost 14 years of crude production (R/P ratio), well above global oil majors. The main upstream assets are located in Western Siberia. In 2017, the company (excluding joint ventures) produced 49.65mmt of liquids, a YoY increase of 4.1% even within the framework of the OPEC+ limitations. The main drivers of the continuing production ramp up were the Novoportovskoye and Prirazlomnoye greenfields, which together produced 8.6mmt of liquids last year, up 69% YoY. The company's main oil processing asset, the 21.6mmt/a Omsk Oil Refinery, is one of the most advanced oil refineries in Russia. In 2017, Gazprom Neft refined 40.1mmt of crude oil, down 4.2% on the year before.

Company website

http://www.gazprom-neft.com/

Shareholder structure

Free float 4%

Gazprom

96%

Source: Company data, VTB Capital Research

Research team

Dmitry Loukashov, CFA / +7 495 663 46 34

Ekaterina Rodina / +7 495 663 47 33

Alexander Donskoy / +7 495 660 67 88

Aydar Safin / +7 495 663 46 32

Artur Muradyants / +7 495 663 46 38

Russian Oil and Gas

Last model update on: 21 December 2018

|

IFRS |

2016 |

2017 |

2018F |

2019F |

2020F |

|

2021F |

||

|

Company data |

|

|

|

|

|

|

|

|

|

|

Weighted avg # shares, mn |

4,718 |

4,718 |

4,718 |

4,718 |

4,718 |

4,718 |

|

||

|

Avg market cap, USD mn |

11,847 |

17,587 |

24,660 |

24,660 |

24,660 |

24,660 |

|

||

|

EV, USD mn |

21,750 |

27,646 |

33,089 |

33,025 |

31,664 |

30,053 |

|

||

|

Ratios & analysis |

|

|

|

|

|

|

|

|

|

|

P/E, x |

4.0x |

4.1x |

4.1x |

4.2x |

3.5x |

|

3.3x |

||

|

EV/EBITDA, x |

4.0x |

3.6x |

3.3x |

3.6x |

3.1x |

|

2.8x |

||

|

P/B, x |

0.5x |

0.6x |

0.7x |

0.6x |

0.5x |

|

0.5x |

||

|

FCF yield, % |

-7.9% |

6.5% |

11.2% |

8.2% |

13.7% |

16.5% |

|

||

|

Dividend yield (ords), % |

7.3% |

6.4% |

8.0% |

8.2% |

9.9% |

10.4% |

|

||

|

Dividend yield (prefs), % |

|

|

|

|

|

|

|

|

|

|

EPS(ords), USD |

0.63 |

0.92 |

1.27 |

1.22 |

1.48 |

1.56 |

|

||

|

CFPS, USD |

1.02 |

1.53 |

1.71 |

1.57 |

1.78 |

1.83 |

|

||

|

Free CFPS, USD |

|

(0.20) |

0.24 |

0.58 |

0.43 |

0.72 |

|

0.86 |

|

|

DPS (ords), USD |

|

0.18 |

0.24 |

0.41 |

0.43 |

0.52 |

|

0.54 |

|

|

Payout ratio (ords), % |

|

28.9% |

26.0% |

32.6% |

34.8% |

34.8% |

|

34.8% |

|

|

BPS(ords), USD |

|

5.05 |

6.11 |

7.58 |

8.73 |

10.09 |

|

11.40 |

|

|

Revenues growth, % |

|

-7% |

36% |

19% |

-11% |

5% |

|

3% |

|

|

EBITDA, chg |

9% |

38% |

31% |

-9% |

13% |

3% |

|

||

|

EPS growth, % |

66% |

45% |

38% |

-4% |

21% |

5% |

|

||

|

EBIT margin, % |

14% |

15% |

18% |

17% |

20% |

21% |

|

||

|

EBITDA margin, % |

21.7% |

22.1% |

24.4% |

24.8% |

26.7% |

26.7% |

|

||

|

Net margin, % |

11.8% |

12.6% |

14.7% |

15.8% |

18.3% |

18.7% |

|

||

|

ROE, % |

13.3% |

16.1% |

17.9% |

15.0% |

15.7% |

14.6% |

|

||

|

ROIC, % |

7.1% |

9.0% |

10.8% |

8.5% |

10.2% |

10.1% |

|

||

|

Capex/Revenues, % |

23% |

18% |

13% |

15% |

13% |

12% |

|

||

|

Capex/Depreciation, x |

3.0x |

2.5x |

1.9x |

1.9x |

2.0x |

|

1.9x |

||

|

Net debt/Equity, % |

|

42% |

35% |

24% |

20% |

15% |

|

10% |

|

|

Net debt/EBITDA, x |

1.8x |

1.3x |

0.8x |

0.9x |

0.7x |

|

0.5x |

||

|

Net interest cover, x |

|

|

|

|

|

|

|

|

|

|

Income statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Revenues |

25,286 |

34,336 |

40,843 |

36,467 |

38,211 |

39,425 |

|

||

|

Cost of sales |

(18,153) |

(24,891) |

(28,983) |

(25,637) |

(26,145) |

(26,971) |

|

||

|

SG&A and other opexp. |

|

(1,643) |

(1,844) |

(1,896) |

(1,792) |

(1,859) |

|

(1,910) |

|

|

EBITDA |

5,490 |

7,601 |

9,964 |

9,038 |

10,207 |

10,544 |

|

||

|

Depreciation & amortization |

(1,936) |

(2,416) |

(2,801) |

(2,904) |

(2,572) |

(2,418) |

|

||

|

Operating profit |

3,554 |

5,184 |

7,163 |

6,134 |

7,635 |

8,126 |

|

||

|

Non-operating gains /(exp.) |

154 |

(134) |

(603) |

(178) |

(201) |

(201) |

|

||

|

EBIT |

3,554 |

5,184 |

7,163 |

6,134 |

7,635 |

8,126 |

|

||

|

Net interest income/(exp.) |

(346) |

(258) |

(230) |

(108) |

(196) |

(196) |

|

||

|

Profit before tax |

3,870 |

5,573 |

7,883 |

7,401 |

8,791 |

9,282 |

|

||

|

Income tax |

(743) |

(951) |

(1,507) |

(1,248) |

(1,334) |

(1,448) |

|

||

|

Minority interests |

(142) |

(281) |

(388) |

(374) |

(454) |

(477) |

|

||

|

Net income |

|

2,985 |

4,340 |

5,988 |

5,778 |

7,003 |

|

7,357 |

|

|

Cash flow statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash flow from operations |

4,791 |

7,227 |

8,069 |

7,416 |

8,419 |

8,619 |

|

||

|

Working capital changes |

227 |

905 |

- |

- |

- |

- |

|

||

|

Capex |

(5,738) |

(6,120) |

(5,310) |

(5,397) |

(5,046) |

(4,569) |

|

||

|

Other investing activities |

924 |

854 |

- |

- |

- |

- |

|

||

|

Free cash flow |

|

(932) |

1,145 |

2,759 |

2,019 |

3,373 |

|

4,050 |

|

|

Dividends paid |

|

(57) |

(907) |

(1,131) |

(1,954) |

(2,012) |

|

(2,439) |

|

|

Net change in borrowings |

|

(953) |

61 |

|

|

|

|

|

|

|

Other financing cash flow |

|

(10) |

(20) |

|

|

|

|

|

|

|

Movement in cash |

|

(1,201) |

977 |

1,629 |

64 |

1,361 |

|

1,611 |

|

|

Balance sheet summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash and equivalents |

|

554 |

1,573 |

3,202 |

3,266 |

4,627 |

|

6,238 |

|

|

PP&E |

|

28,461 |

35,630 |

40,940 |

46,337 |

51,383 |

|

55,952 |

|

|

Goodwill |

|

1,157 |

1,288 |

1,288 |

1,288 |

1,288 |

|

1,288 |

|

|

Investments |

694 |

181 |

181 |

181 |

181 |

181 |

|

||

|

Other assets |

11,154 |

12,196 |

12,196 |

12,196 |

12,196 |

12,196 |

|

||

|

Total assets |

42,020 |

50,868 |

57,807 |

63,268 |

69,675 |

75,855 |

|

||

|

Interest bearing debt |

11,151 |

11,813 |

11,812 |

11,812 |

11,812 |

11,812 |

|

||

|

Other liabilities |

7,060 |

10,251 |

10,252 |

10,252 |

10,252 |

10,252 |

|

||

|

Total liabilities |

18,211 |

22,064 |

22,064 |

22,064 |

22,064 |

22,064 |

|

||

|

Total shareholder's equity |

22,424 |

26,966 |

33,517 |

38,604 |

44,557 |

50,260 |

|

||

|

Minority interest |

1,385 |

1,838 |

2,226 |

2,600 |

3,054 |

3,531 |

|

||

|

Net working capital |

1,989 |

454 |

453 |

453 |

453 |

453 |

|

||

|

Net Debt |

9,903 |

10,058 |

8,429 |

8,365 |

7,004 |

5,393 |

|

||

|

Capital |

33,575 |

38,779 |

45,329 |

50,416 |

56,369 |

62,072 |

|

||

|

|

|

|

|

|

|

|

|

|

|

21 December 2018 |

4 |

vk.com/id446425943

Russia

Energy: Integrated Oil & Gas

VTB Capital Facts & Forecasts

Russia

Energy / Integrated Oil & Gas

Lukoil

Prices as of: 19 December 2018

Ticker |

CCY |

Current |

12mo TP |

Rating |

LKOH RX |

USD |

72.82 |

71.00 |

Hold |

Share price performance, 12-mo

100 |

25% |

80 |

20% |

|

|

60 |

15% |

|

|

|

10% |

40 |

5% |

|

|

20 |

0% |

|

|

0 |

-5% |

Dec Feb Apr Jun Aug Oct Dec

LKOH RX, USD, lhs

Relative to MOEX Index, %, rhs

Company description

Lukoil is Russia's largest non-state-owned integrated oil and gas company. In 2017, it produced 84.8mmt (down 5% YoY) of crude oil (including oil produced within international projects) which makes it the second largest oil producer in Russia. Refining occurs in Russia (in the Central region and Timano-Pechora) and abroad (Romania, Bulgaria, Italy and the Netherlands). The company's total proved reserves of crude amounted to 12bn bbl according to SEC standards as of the end of 2017, thus representing a robust 19 years of liquids reserves life. Total refining in 2017 was 73.8mmt (up 11% YoY).

Company website

http://www.lukoil.com/

Shareholder structure

Treasury shares 5%

Management of the company 39%

Other/Free float 56%

Source: Company data, VTB Capital Research

Research team

Dmitry Loukashov, CFA / +7 495 663 46 34

Ekaterina Rodina / +7 495 663 47 33

Alexander Donskoy / +7 495 660 67 88

Aydar Safin / +7 495 663 46 32

Artur Muradyants / +7 495 663 46 38

Russian Oil and Gas

Last model update on: 21 December 2018

|

IFRS |

2016 |

2017 |

2018F |

2019F |

2020F |

|

2021F |

||

|

Company data |

|

|

|

|

|

|

|

|

|

|

Weighted avg # shares, mn |

|

850.6 |

850.6 |

750.6 |

750.6 |

750.6 |

|

750.6 |

|

|

Avg market cap, USD mn |

30,536 |

37,177 |

51,675 |

51,675 |

51,675 |

51,675 |

|

||

|

EV, USD mn |

37,465 |

41,802 |

52,883 |

52,284 |

50,552 |

48,885 |

|

||

|

Ratios & analysis |

|

|

|

|

|

|

|

|

|

|

P/E, x |

|

11.8x |

6.2x |

5.5x |

8.7x |

7.3x |

|

7.0x |

|

|

EV/EBITDA, x |

4.0x |

3.4x |

3.1x |

4.1x |

3.6x |

|

3.4x |

||

|

P/B, x |

|

0.7x |

0.7x |

0.8x |

0.7x |

0.6x |

|

0.5x |

|

|

FCF yield, % |

10.5% |

9.6% |

12.6% |

6.8% |

8.5% |

8.6% |

|

||

|

Dividend yield (ords), % |

7.8% |

6.6% |

4.6% |

4.8% |

5.0% |

5.2% |

|

||

|

Dividend yield (prefs), % |

|

|

|

|

|

|

|

|

|

|

EPS(ords), USD |

3.63 |

8.44 |

13.36 |

8.39 |

9.96 |

10.38 |

|

||

|

CFPS, USD |

13.19 |

15.28 |

20.16 |

15.60 |

16.90 |

17.40 |

|

||

|

Free CFPS, USD |

4.51 |

5.01 |

9.21 |

4.93 |

6.19 |

6.25 |

|

||

|

DPS (ords), USD |

3.34 |

3.43 |

3.37 |

3.50 |

3.65 |

3.80 |

|

||

|

Payout ratio (ords), % |

77.3% |

34.0% |

23.8% |

39.5% |

34.7% |

34.6% |

|

||

|

BPS(ords), USD |

62.56 |

71.24 |

96.25 |

107.7 |

120.7 |

134.1 |

|

||

|

Revenues growth, % |

|

-17% |

31% |

26% |

-19% |

2% |

|

3% |

|

|

EBITDA, chg |

|

-19% |

31% |

27% |

-25% |

8% |

|

4% |

|

|

EPS growth, % |

|

-35% |

133% |

58% |

-37% |

19% |

|

4% |

|

|

EBIT margin, % |

8% |

9% |

10% |

8% |

9% |

9% |

|

||

|

EBITDA margin, % |

14.0% |

14.0% |

14.1% |

13.1% |

13.9% |

14.1% |

|

||

|

Net margin, % |

4.0% |

7.1% |

7.8% |

6.1% |

7.1% |

7.2% |

|

||

|

ROE, % |

5.8% |

11.9% |

13.9% |

7.8% |

8.3% |

7.8% |

|

||

|

ROIC, % |

7.0% |

8.5% |

10.8% |

6.6% |

6.9% |

6.7% |

|

||

|

Capex/Revenues, % |

10% |

9% |

6% |

8% |

8% |

8% |

|

||

|

Capex/Depreciation, x |

1.6x |

1.6x |

1.5x |

1.5x |

1.5x |

|

1.6x |

||

|

Net debt/Equity, % |

13% |

8% |

2% |

1% |

-1% |

-3% |

|

||

|

Net debt/EBITDA, x |

0.6x |

0.3x |

0.1x |

0.0x |

(0.1x) |

|

(0.2x) |

||

|

Net interest cover, x |

8.9x |

18.5x |

22.1x |

14.5x |

32.9x |

|

34.8x |

||

|

Income statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Revenues |

77,941 |

101,739 |

128,406 |

103,393 |

105,711 |

108,671 |

|

||

|

Cost of sales |

(64,120) |

(84,655) |

(107,611) |

(87,222) |

(88,313) |

(90,532) |

|

||

|

SG&A and other opexp. |

(2,925) |

(2,833) |

(2,660) |

(2,616) |

(2,707) |

(2,841) |

|

||

|

EBITDA |

10,896 |

14,251 |

18,135 |

13,555 |

14,691 |

15,298 |

|

||

|

Depreciation & amortization |

|

(4,646) |

(5,571) |

(5,487) |

(5,211) |

(5,271) |

|

(5,333) |

|

|

Operating profit |

6,250 |

8,680 |

12,648 |

8,344 |

9,420 |

9,965 |

|

||

|

Non-operating gains /(exp.) |

|

(1,824) |

223 |

223 |

(306) |

(333) |

|

(333) |

|

|

EBIT |

6,250 |

8,680 |

12,648 |

8,344 |

9,420 |

9,965 |

|

||

|

Net interest income/(exp.) |

(481) |

(209) |

(278) |

(170) |

177 |

177 |

|

||

|

Profit before tax |

4,063 |

8,983 |

12,966 |

8,217 |

9,613 |

10,158 |

|

||

|

Income tax |

(967) |

(1,778) |

(2,899) |

(1,897) |

(2,111) |

(2,339) |

|

||

|

Minority interests |

(13) |

(28) |

(39) |

(24) |

(29) |

(30) |

|

||

|

Net income |

3,084 |

7,177 |

10,028 |

6,295 |

7,473 |

7,789 |

|

||

|

Cash flow statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash flow from operations |

11,217 |

12,998 |

15,134 |

11,707 |

12,682 |

13,060 |

|

||

|

Working capital changes |

749 |

(428) |

|

|

|

|

|

|

|

|

Capex |

(7,413) |

(8,766) |

(8,224) |

(8,003) |

(8,034) |

(8,365) |

|

||

|

Other investing activities |

(299) |

(112) |

- |

- |

- |

- |

|

||

|

Free cash flow |

3,835 |

4,261 |

6,910 |

3,704 |

4,648 |

4,695 |

|

||

|

Share issue (reacquisition) |

|

(162) |

|

|

|

|

|

|

|

|

Dividends paid |

(1,949) |

(2,425) |

(2,921) |

(2,528) |

(2,630) |

(2,742) |

|

||

|

Net change in borrowings |

(175) |

(987) |

|

|

|

|

|

|

|

|

Other financing cash flow |

|

(755) |

(665) |

(571) |

(576) |

(286) |

|

(286) |

|

|

Movement in cash |

|

61 |

1,183 |

3,417 |

599 |

1,732 |

|

1,667 |

|

|

Balance sheet summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash and equivalents |

4,309 |

5,736 |

9,153 |

9,753 |

11,484 |

13,151 |

|

||

|

PP&E |

55,911 |

62,069 |

70,293 |

78,296 |

86,330 |

94,695 |

|

||

|

Goodwill |

711 |

717 |

717 |

717 |

717 |

717 |

|

||

|

Investments |

|

2,957 |

3,192 |

3,192 |

3,192 |

3,192 |

|

3,192 |

|

|

Other assets |

|

18,785 |

19,019 |

19,019 |

19,019 |

19,019 |

|

19,019 |

|

|

Total assets |

|

82,673 |

90,733 |

102,374 |

110,977 |

120,742 |

|

130,774 |

|

|

Interest bearing debt |

11,517 |

10,701 |

10,701 |

10,701 |

10,701 |

10,701 |

|

||

|

Other liabilities |

17,944 |

19,435 |

19,435 |

19,435 |

19,435 |

19,435 |

|

||

|

Total liabilities |

29,461 |

30,136 |

30,136 |

30,136 |

30,136 |

30,136 |

|

||

|

Total shareholder's equity |

53,100 |

60,468 |

72,070 |

80,648 |

90,386 |

100,387 |

|

||

|

Minority interest |

112 |

129 |

168 |

192 |

221 |

251 |

|

||

|

Net working capital |

3,543 |

4,453 |

4,453 |

4,453 |

4,453 |

4,453 |

|

||

|

Net Debt |

6,929 |

4,625 |

1,208 |

608 |

(1,123) |

(2,790) |

|

||

|

Capital |

64,617 |

71,168 |

82,771 |

91,349 |

101,087 |

111,088 |

|

||

|

|

|

|

|

|

|

|

|

|

|

21 December 2018 |

5 |

vk.com/id446425943

Russia

Energy: Integrated Oil & Gas

VTB Capital Facts & Forecasts

Russia

Energy / Integrated Oil & Gas

Surgutneftegas

Prices as of: 19 December 2018

Ticker |

CCY |

Current |

12mo TP |

Rating |

SNGS RX |

USD |

0.41 |

0.36 |

Sell |

Share price performance, 12-mo

0.6 |

10% |

|

0.5 |

0% |

|

0.4 |

||

|

||

0.3 |

-10% |

|

0.2 |

-20% |

|

0.1 |

||

|

||

0 |

-30% |

Dec Feb Apr Jun Aug Oct Dec

SNGS RX, USD, lhs

Relative to MOEX Index, %, rhs

Company description

Surgutneftegas is the third largest publicly traded oil company in Russia in terms of consolidated production, with 60.5mnt crude output in 2017. It concentrates on developing conventional oil reserves in Western Siberia, which accounts for 85% of the company's total oil production. The decline in oil production at matured fields (2% annually on average) is compensated for by increasing production at the Talakanskoye group of greenfields (around 9mmt of oil this year, we estimate). As a result, Surgutneftegas' actual oil production CAGR has been close to zero since 2008, when Talakanskoye was launched, with average output of 1.2mmbd. Surgutneftegas also owns the Kirishi Oil Refinery, located in northwest Russia, which has total installed capacity of 20mmt per year.

Company website

http://www.surgutneftegas.ru/en/main/

Shareholder structure

Free float |

NCPs |

|

27% |

||

incorporated by |

||

|

||

|

Surgutneftegas |

|

|

73% |

Source: Company data, VTB Capital Research

Research team

Dmitry Loukashov, CFA / +7 495 663 46 34

Ekaterina Rodina / +7 495 663 47 33

Alexander Donskoy / +7 495 660 67 88

Aydar Safin / +7 495 663 46 32

Artur Muradyants / +7 495 663 46 38

Russian Oil and Gas

Last model update on: 21 December 2018

|

IFRS |

2016 |

2017 |

2018F |

2019F |

2020F |

|

2021F |

||

|

Company data |

|

|

|

|

|

|

|

|

|

|

Weighted avg # shares, mn |

|

43,428 |

43,428 |

43,428 |

43,428 |

43,428 |

|

43,428 |

|

|

Avg market cap, USD mn |

21,940 |

21,539 |

19,240 |

19,240 |

19,240 |

19,240 |

|

||

|

EV, USD mn |

13,653 |

6,230 |

2,412 |

2,150 |

1,309 |

193.0 |

|

||

|

Ratios & analysis |

|

|

|

|

|

|

|

|

|

|

P/E, x |

|

neg |

6.4x |

1.5x |

3.3x |

3.0x |

|

2.8x |

|

|

EV/EBITDA, x |

2.6x |

1.0x |

0.1x |

0.2x |

0.0x |

|

neg |

||

|

P/B, x |

|

0.4x |

0.3x |

0.3x |

0.3x |

0.2x |

|

0.2x |

|

|

FCF yield, % |

5.7% |

15.8% |

11.5% |

7.5% |

8.3% |

10.1% |

|

||

|

Dividend yield (ords), % |

2.1% |

2.1% |

2.3% |

2.2% |

2.2% |

2.2% |

|

||

|

Dividend yield (prefs), % |

1.9% |

4.2% |

16.8% |

7.6% |

8.4% |

9.0% |

|

||

|

EPS(ords), USD |

(0.021) |

0.077 |

0.28 |

0.13 |

0.14 |

0.15 |

|

||

|

CFPS, USD |

0.090 |

0.14 |

0.12 |

0.10 |

0.10 |

0.11 |

|

||

|

Free CFPS, USD |

0.028 |

0.078 |

0.047 |

0.031 |

0.035 |

0.042 |

|

||

|

DPS (ords), USD |

0.010 |

0.010 |

0.0096 |

0.0089 |

0.0089 |

0.0089 |

|

||

|

DPS (prefs) |

0.010 |

0.022 |

0.097 |

0.044 |

0.049 |

0.052 |

|

||

|

Payout ratio (ords), % |

n/a |

11.1% |

2.9% |

5.9% |

5.3% |

5.0% |

|

||

|

Payout ratio (prefs), % |

|

n/a |

5.1% |

6.3% |

6.2% |

6.3% |

|

6.3% |

|

|

BPS(ords), USD |

|

1.31 |

1.44 |

1.56 |

1.63 |

1.72 |

|

1.81 |

|

|

Revenues growth, % |

|

-7% |

32% |

25% |

-19% |

6% |

|

6% |

|

|

EBITDA, chg |

-2% |

15% |

39% |

-29% |

3% |

2% |

|

||

|

EPS growth, % |

-107% |

-460% |

259% |

-55% |

10% |

6% |

|

||

|

EBIT margin, % |

26% |

23% |

28% |

23% |

23% |

22% |

|

||

|

EBITDA margin, % |

33.1% |

28.8% |

32.2% |

28.3% |

27.5% |

26.5% |

|

||

|

Net margin, % |

neg |

16.6% |

47.7% |

26.8% |

27.8% |

27.6% |

|

||

|

ROE, % |

n/m |

5.3% |

17.7% |

7.7% |

8.0% |

8.0% |

|

||

|

ROIC, % |

15.5% |

13.2% |

13.6% |

10.0% |

9.2% |

8.6% |

|

||

|

Capex/Revenues, % |

18% |

14% |

13% |

16% |

14% |

12% |

|

||

|

Capex/Depreciation, x |

2.3x |

2.4x |

3.1x |

3.1x |

2.8x |

|

2.5x |

||

|

Net debt/Equity, % |

-15% |

-24% |

-25% |

-24% |

-24% |

-24% |

|

||

|

Net debt/EBITDA, x |

(1.6x) |

(2.6x) |

(2.1x) |

(3.0x) |

(3.0x) |

|

(3.1x) |

||

|

Net interest cover, x |

|

(29.5x) |

(17.0x) |

(35.5x) |

(23.7x) |

(24.5x) |

|

(25.0x) |

|

|

Income statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Revenues |

15,222 |

20,137 |

25,088 |

20,261 |

21,534 |

22,930 |

|

||

|

Cost of sales |

(8,780) |

(12,709) |

(15,429) |

(12,993) |

(13,969) |

(15,204) |

|

||

|

SG&A and other opexp. |

|

(1,407) |

(1,624) |

(1,576) |

(1,544) |

(1,646) |

|

(1,661) |

|

|

EBITDA |

5,035 |

5,804 |

8,083 |

5,724 |

5,919 |

6,065 |

|

||

|

Depreciation & amortization |

|

(1,150) |

(1,136) |

(1,063) |

(1,027) |

(1,072) |

|

(1,117) |

|

|

Operating profit |

3,885 |

4,668 |

7,020 |

4,697 |

4,847 |

4,948 |

|

||

|

Non-operating gains /(exp.) |

(6,570) |

(2,104) |

5,911 |

274 |

19 |

19 |

|

||

|

EBIT |

3,885 |

4,668 |

7,020 |

4,697 |

4,847 |

4,948 |

|

||

|

Net interest income/(exp.) |

1,610 |

1,659 |

1,717 |

1,669 |

2,476 |

2,807 |

|

||

|

Profit before tax |

(1,077) |

4,223 |

14,648 |

6,640 |

7,342 |

7,774 |

|

||

|

Income tax |

152 |

(886) |

(2,677) |

(1,202) |

(1,359) |

(1,433) |

|

||

|

Minority interests |

(1) |

(1) |

(4) |

(2) |

(2) |

(2) |

|

||

|

Net income |

(926) |

3,336 |

11,967 |

5,436 |

5,981 |

6,339 |

|

||

|

Cash flow statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash flow from operations |

3,913 |

6,102 |

5,383 |

4,501 |

4,539 |

4,611 |

|

||

|

Working capital changes |

(164) |

294 |

(19) |

(19) |

(19) |

(19) |

|

||

|

Capex |

(2,696) |

(2,745) |

(3,324) |

(3,148) |

(3,040) |

(2,799) |

|

||

|

Other investing activities |

(306) |

(2,238) |

- |

- |

- |

- |

|

||

|

Free cash flow |

1,222 |

3,366 |

2,059 |

1,353 |

1,499 |

1,812 |

|

||

|

Dividends paid |

(1,107) |

(447) |

(541) |

(1,091) |

(658) |

(697) |

|

||

|

Net change in borrowings |

|

372 |

1,406 |

- |

- |

- |

|

- |

|

|

Other financing cash flow |

|

(103) |

(205) |

- |

- |

- |

|

- |

|

|

Movement in cash |

|

26 |

1,886 |

1,519 |

262 |

841 |

|

1,116 |

|

|

Balance sheet summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash and equivalents |

1,787 |

3,812 |

5,330 |

5,592 |

6,433 |

7,549 |

|

||

|

PP&E |

21,953 |

24,839 |

28,163 |

31,311 |

34,351 |

37,150 |

|

||

|

Goodwill |

|

3 |

0 |

- |

- |

- |

|

- |

|

|

Investments |

|

36,904 |

41,219 |

41,219 |

41,219 |

41,219 |

|

41,219 |

|

|

Other assets |

|

4,005 |

3,735 |

3,736 |

3,736 |

3,736 |

|

3,736 |

|

|

Total assets |

64,652 |

73,605 |

78,448 |

81,858 |

85,739 |

89,654 |

|

||

|

Interest bearing debt |

1,480 |

3,202 |

3,202 |

3,202 |

3,202 |

3,202 |

|

||

|

Other liabilities |

6,371 |

7,674 |

7,674 |

7,674 |

7,674 |

7,674 |

|

||

|

Total liabilities |

7,850 |

10,877 |

10,876 |

10,876 |

10,876 |

10,876 |

|

||

|

Total shareholder's equity |

56,798 |

62,724 |

67,567 |

70,977 |

74,858 |

78,773 |

|

||

|

Minority interest |

4 |

5 |

9 |

11 |

13 |

15 |

|

||

|

Net working capital |

2,029 |

2,168 |

2,168 |

2,168 |

2,168 |

2,168 |

|

||

|

Net Debt |

(8,287) |

(15,309) |

(16,828) |

(17,090) |

(17,931) |

(19,047) |

|

||

|

Capital |

58,277 |

65,926 |

70,769 |

74,179 |

78,060 |

81,975 |

|

||

21 December 2018 |

6 |

vk.com/id446425943

Russia

Energy: Integrated Oil & Gas

VTB Capital Facts & Forecasts

Russia

Energy / Integrated Oil & Gas

Tatneft

Prices as of: 19 December 2018

Ticker |

CCY |

Current |

12mo TP |

Rating |

TATN RX |

USD |

10.59 |

7.00 |

Sell |

Share price performance, 12-mo

15 |

40% |

|

30% |

10 |

20% |

|

|

5 |

10% |

|

|

|

0% |

0 |

-10% |

Dec Feb Apr Jun Aug Oct Dec

TATN RX, USD, lhs

Relative to MOEX Index, %, rhs

Company description

Tatneft is the fifth largest oil producer in Russia, with 29mmt output in 2017. The majority of its operations are located in the Volga-Urals, with the Romashkinskoye field being the company's core producing asset (in 2017, it accounted for 52% of its total production volumes). Tatneft is also developing the Ashalchinskoye natural bitumen field, where 1.2mnt of high viscous crude oil was produced in 2017. At the end of 2011, Tatneft constructed the first line of its oil refinery (TANECO) in Nizhnekamsk. TANECO is a greenfield refinery and petrochemical complex with a current throughput capacity of 8.7mmt per annum.

Company website

http://www.tatneft.ru/

Shareholder structure

Svyazinvestneftekhim

26%

Quasi-

Treasury

3%

Other/Free

float

71%

Source: Company data, VTB Capital Research

Research team

Dmitry Loukashov, CFA / +7 495 663 46 34

Ekaterina Rodina / +7 495 663 47 33

Alexander Donskoy / +7 495 660 67 88

Aydar Safin / +7 495 663 46 32

Artur Muradyants / +7 495 663 46 38

Russian Oil and Gas

Last model update on: 21 December 2018

|

IFRS |

2016 |

2017 |

2018F |

2019F |

2020F |

|

2021F |

||

|

Company data |

|

|

|

|

|

|

|

|

|

|

Weighted avg # shares, mn |

|

2,257 |

2,251 |

2,251 |

2,251 |

2,251 |

|

2,251 |

|

|

Avg market cap, USD mn |

11,183 |

15,146 |

23,436 |

23,436 |

23,436 |

23,436 |

|

||

|

EV, USD mn |

9,849 |

14,019 |

21,662 |

20,357 |

20,206 |

19,641 |

|

||

|

Ratios & analysis |

|

|

|

|

|

|

|

|

|

|

P/E, x |

|

7.2x |

7.3x |

6.4x |

9.7x |

8.9x |

|

7.8x |

|

|

EV/EBITDA, x |

4.1x |

4.5x |

4.5x |

5.8x |

5.2x |

|

4.5x |

||

|

P/B, x |

|

1.0x |

1.2x |

1.6x |

1.3x |

1.2x |

|

1.0x |

|

|

FCF yield, % |

6.0% |

11.9% |

8.9% |

3.7% |

4.5% |

3.3% |

|

||

|

Dividend yield (ords), % |

7.7% |

9.3% |

8.9% |

5.0% |

5.5% |

6.2% |

|

||

|

Dividend yield (prefs), % |

13.8% |

13.7% |

12.7% |

7.1% |

7.8% |

8.9% |

|

||

|

EPS(ords), USD |

0.71 |

0.94 |

1.65 |

1.09 |

1.20 |

1.36 |

|

||

|

CFPS, USD |

0.93 |

1.45 |

1.81 |

1.30 |

1.43 |

1.61 |

|

||

|

Free CFPS, USD |

0.31 |

0.81 |

0.95 |

0.39 |

0.48 |

0.35 |

|

||

|

DPS (ords), USD |

0.39 |

0.64 |

0.94 |

0.53 |

0.58 |

0.66 |

|

||

|

DPS (prefs) |

0.39 |

0.64 |

0.94 |

0.53 |

0.58 |

0.66 |

|

||

|

Payout ratio (ords), % |

51.5% |

63.6% |

53.3% |

45.4% |

45.2% |

45.2% |

|

||

|

Payout ratio (prefs), % |

|

3.6% |

4.5% |

3.7% |

3.2% |

3.2% |

|

3.2% |

|

|

BPS(ords), USD |

|

5.18 |

5.54 |

6.69 |

8.18 |

9.20 |

|

10.71 |

|

|

Revenues growth, % |

|

-8% |

34% |

22% |

-20% |

8% |

|

10% |

|

|

EBITDA, chg |

-3% |

29% |

54% |

-27% |

11% |

13% |

|

||

|

EPS growth, % |

-1% |

32% |

76% |

-34% |

10% |

14% |

|

||

|

EBIT margin, % |

22% |

21% |

28% |

24% |

25% |

26% |

|

||

|

EBITDA margin, % |

25.1% |

24.2% |

30.4% |

27.5% |

28.3% |

28.9% |

|

||

|

Net margin, % |

16.1% |

15.9% |

22.8% |

18.8% |

19.1% |

19.7% |

|

||

|

ROE, % |

13.8% |

17.1% |

24.8% |

13.4% |

13.1% |

12.8% |

|

||

|

ROIC, % |

11.0% |

13.0% |

19.4% |

11.9% |

11.9% |

12.1% |

|

||

|

Capex/Revenues, % |

14% |

11% |

12% |

16% |

15% |

18% |

|

||

|

Capex/Depreciation, x |

4.4x |

3.4x |

4.4x |

4.8x |

4.8x |

|

6.1x |

||

|

Net debt/Equity, % |

-11% |

-9% |

-12% |

-17% |

-16% |

-16% |

|

||

|

Net debt/EBITDA, x |

(0.5x) |

(0.4x) |

(0.4x) |

(0.9x) |

(0.8x) |

|

(0.8x) |

||

|

Net interest cover, x |

|

37.0x |

52.5x |

91.9x |

64.5x |

72.2x |

|

82.2x |

|

|

Income statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Revenues |

9,917 |

13,292 |

16,230 |

13,060 |

14,085 |

15,560 |

|

||

|

Cost of sales |

(6,603) |

(8,917) |

(10,495) |

(8,687) |

(9,242) |

(10,110) |

|

||

|

SG&A and other opexp. |

|

(829) |

(1,162) |

|

|

|

|

|

|

|

EBITDA |

2,485 |

3,213 |

4,936 |

3,585 |

3,982 |

4,496 |

|

||

|

Depreciation & amortization |

|

(322) |

(426) |

(438) |

(426) |

(448) |

|

(471) |

|

|

Operating profit |

2,162 |

2,786 |

4,498 |

3,159 |

3,534 |

4,025 |

|

||

|

Non-operating gains /(exp.) |

(28) |

(14) |

123 |

6 |

- |

- |

|

||

|

EBIT |

2,162 |

2,786 |

4,498 |

3,159 |

3,534 |

4,025 |

|

||

|

Net interest income/(exp.) |

23 |

58 |

39 |

38 |

38 |

38 |

|

||

|

Profit before tax |

2,102 |

2,803 |

4,660 |

3,203 |

3,572 |

4,063 |

|

||

|

Income tax |

(520) |

(679) |

(958) |

(748) |

(878) |

(983) |

|

||

|

Minority interests |

19 |

(13) |

1 |

(3) |

(3) |

(19) |

|

||

|

Net income |

1,601 |

2,110 |

3,704 |

2,452 |

2,691 |

3,061 |

|

||

|

Cash flow statement summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash flow from operations |

2,108 |

3,261 |

4,073 |

2,927 |

3,209 |

3,631 |

|

||

|

Working capital changes |

184 |

(113) |

|

|

|

|

|

|

|

|

Capex |

(1,427) |

(1,456) |

(1,941) |

(2,049) |

(2,129) |

(2,851) |

|

||

|

Other investing activities |

(396) |

(69) |

- |

- |

- |

- |

|

||

|

Free cash flow |

696 |

1,834 |

2,132 |

878 |

1,080 |

780 |

|

||

|

Share issue (reacquisition) |

- |

- |

|

|

|

|

|

|

|

|

Dividends paid |

|

(369) |

(1,859) |

(1,484) |

(2,183) |

(1,232) |

|

(1,345) |

|

|

Net change in borrowings |

|

(120) |

(60) |

|

|

|

|

|

|

|

Other financing cash flow |

|

- |

0 |

|

|

|

|

|

|

|

Movement in cash |

890 |

(588) |

647 |

(1,305) |

(151) |

(565) |

|

||

|

Balance sheet summary, USD mn |

|

|

|

|

|

|

|

|

|

|

Cash and equivalents |

1,271 |

743 |

1,390 |

1,390 |

1,390 |

1,390 |

|

||

|

PP&E |

|

9,622 |

11,310 |

13,251 |

15,300 |

17,429 |

|

20,280 |

|

|

Goodwill |

|

- |

26 |

26 |

26 |

26 |

|

26 |

|

|

Investments |

|

1,687 |

2,106 |

2,106 |

2,106 |

2,106 |

|

2,106 |

|

|

Other assets |

5,466 |

5,042 |

5,042 |

5,042 |

5,042 |

5,042 |

|

||

|

Total assets |

18,046 |

19,227 |

21,815 |

23,864 |

25,993 |

28,844 |

|

||

|

Interest bearing debt |

892 |

813 |

813 |

(492) |

(643) |

(1,208) |

|

||

|

Other liabilities |

5,466 |

5,936 |

5,936 |

5,936 |

5,936 |

5,936 |

|

||

|

Total liabilities |

6,359 |

6,749 |

6,749 |

5,444 |

5,293 |

4,728 |

|

||

|

Total shareholder's equity |

11,598 |

12,359 |

14,948 |

18,299 |

20,576 |

23,973 |

|

||

|

Minority interest |

89 |

119 |

118 |

121 |

124 |

143 |

|

||

|

Net working capital |

852 |

926 |

926 |

926 |

926 |

926 |

|

||

|

Net Debt |

(1,334) |

(1,127) |

(1,774) |

(3,079) |

(3,230) |

(3,795) |

|

||

|

Capital |

|

12,491 |

13,171 |

15,761 |

17,807 |

19,933 |

|

22,765 |

|

|

|

|

|

|

|

|

|

|

|

|

21 December 2018 |

7 |

vk.com/id446425943 |

Russian Oil and Gas |

Russia |

|

Energy: Integrated Oil & Gas |

|

Disclosures

Production and Distribution of VTB Capital Research Reports outside the United States

The information and opinions contained within VTB Capital research reports are prepared by research analysts associated with JSC VTB Capital, VTB Capital PLC and their non-U.S. affiliates (each such entity, a “VTB Group entity,” and all such entities collectively, the “VTB Group”), as indicated on the front page of this VTB Capital research report. Research reports produced by VTB Group entities are distributed under the VTB Capital logo (each such research report, a “VTB Capital research report”). This VTB Capital research report is distributed outside the United States by VTB Group entities.

Distribution of VTB Capital Research Reports to Investors within the United States

This VTB Capital research report is distributed to investors located within the United States by Xtellus Capital Partners Inc. (“Xtellus”), a broker-dealer registered with the U.S. Securities and Exchange Commission (the “SEC”) and a member of the Financial Industry Regulatory Authority (“FINRA”). Xtellus had no involvement in the preparation of this VTB Capital research report, and is distributing this VTB Capital research report to investors located within the United States as a “third-party research report” as defined in Rule 2241(a)(14). Xtellus has accepted responsibility for the content of this VTB Capital research report to the extent required by SEC guidance under Rule 15a-6.6 under the U.S. Securities Exchange Act of 1934 (the “Exchange Act”). Transactions in securities discussed in this VTB Capital research report must be effected by VTB Group entities with U.S. investors through Xtellus in accordance with Rule 15a-6. If you are an investor located within the United States, you should contact Xtellus if you wish to communicate with the VTB Capital research analysts who wrote this report, or you wish to conduct any transactions in securities described in this report.

Relationship between VTB and Xtellus

Xtellus is the successor entity of VTB Capital Inc, which was an SEC-registered broker dealer and affiliate of the VTB Group. The VTB Group sold its interest in VTB Capital Inc. with effect from August 31st 2018 to a newly formed holding company, Khepri Capital, LLC, an entity established and owned by certain VTB Capital Inc. personnel. In connection with the sale, VTB Capital Inc. was re-named Xtellus. While the VTB Group no longer has any ownership interest in Xtellus, Xtellus continues to provide certain services to VTB Group entities. Specifically, Xtellus (i) acts as agent for VTB Group entities pursuant to Rule 15a-6 under the Exchange Act in connection with securities transactions effected by VTB Group entities with U.S. investors, and (ii) is the exclusive distributor of VTB Capital research reports into the United States. Xtellus receives fees for research and Rule 15a-6 intermediation services it provides to VTB Capital Group entities, including fees for the right to distribute Xtellus research reports outside the United States. While the VTB Group no longer has any ownership interest in Xtellus, in light of the research and Rule 15a-6 service arrangements between the VTB Group and Xtellus, this VTB Capital research report includes disclosures pursuant to FINRA Rule 2241(h)(4) and FINRA Rule 2242(g)(3) applicable to VTB Group entities as if such VTB Group entities were affiliates of Xtellus. The inclusion of these affiliate disclosures should not be construed as implying that any VTB Group entity is affiliated with Xtellus for any other purpose.

Conflict of Interest Disclosures.

VTB Group entities do and seek to do business with companies covered in their research reports. Thus, investors should be aware that the VTB Group may have a conflict of interest that could affect the objectivity of this research report. Investors should consider this research report as only a single factor in making their investment decision. Where an issuer referred to in this report is not included in the disclosure table, the issuer is either considered not to be covered by VTB Capital Research, or the reference is considered to be incidental and therefore the issuer is not a subject company within this report.

Certain disclosures on the companies covered by this VTB Capital research report are set forth below. Additional disclosures on the companies covered by this report can be obtained by accessing the following webpages:

Research disclosures webpage - http://research.vtbcapital.com/ServicePages/Disclosures.aspx.

Investment Recommendations disclosures webpage – https://www.vtbcapital.com/about/information-disclosure/investment- recommendations/

Additional disclosures on the companies covered by this report can be obtained by writing to the offices listed on the back page. In order to receive i) a summary of any basis of the valuation or methodology and the underlying assumptions used to either evaluate a financial instrument or an issuer, or to set a price target for a financial instrument, as well as an indication and a summary of any changes in the valuation, methodology or underlying assumptions; ii) detailed information about the valuation or methodology and the underlying assumptions in any non-proprietary models; or iii) material information about the proprietary models used; please consult the VTB Capital Research web-site at https://research.vtbcapital.com or contact the authors of this document.

21 December 2018 |

8 |

vk.com/id446425943 |

Russian Oil and Gas |

|

|

|

|

Russia |

|

|

|

|

Energy: Integrated Oil & Gas |

|

|

|

|

Issuer Specific Disclosures |

|

|

|

|

Disclosure checklist |

|

|

|

|

Company |

Ticker |

Recent price |

Disclosure |

|

Gazprom |

GAZP RX |

153.0 (RUB) |

4a, 5a, 6a, 9a, 12a |

|

Gazprom Neft |

SIBN RX |

350.7 (RUB) |

4a, 5a, 6a, 9a |

|

Lukoil |

LKOH RX |

4,910 (RUB) |

4a |

|

Surgutneftegas |

SNGS RX |

27.89 (RUB) |

4a |

|

Tatneft |

TATN RX |

714.3 (RUB) |

4a |

4a. VTB Capital or an affiliated company is a provider of liquidity and/or a market maker in the securities of the relevant issuer at the time this research report was published. VTB Capital or an affiliated company will buy and sell securities of the relevant issuer on a principal basis.

5a. VTB Capital or an affiliated company has been lead manager or co-lead manager over the previous 12 months of a public offering of securities of the relevant issuer.

6a. VTB Capital or an affiliated company is party to an agreement that has been in effect during the previous 12 months, or has received compensation during the previous 12 months, from the relevant issuer relating to the provision of investment banking services.

9a. VTB Capital or an affiliated company expects to receive or intends to seek investment banking related compensation from the relevant issuer within the next 3 months.

12a. VTB Capital or an affiliated company has a long shareholding position exceeding 0.5% of the total issued share capital in the relevant issuer.

Analysts Certification

The research analyst(s) whose name(s) appear on this VTB Capital research report certify pursuant to SEC Regulation AC that: i) all of the views expressed in this research report accurately reflect their personal views about the subject security or issuer, and ii) no part of the research analysts’ compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analysts in this VTB Capital research report.

The research analysts whose names appear on VTB Capital research reports received compensation that is based upon various factors including VTB Capital Group’s total revenues, a portion of which are generated by VTB Capital Group’s investment banking activities.

Investment Ratings

VTB Capital uses a three-tiered Investment Rating system for stocks under coverage: Buy, Hold, or Sell.

The three main ratings correspond to the next 12-month Expected Total Return (ETR), defined as the difference between the Target Price and the Last Price as indicated by Bloomberg divided by that Last Price plus the expected Dividend Yield over the next 12 months. Under this Investment Ratings system, Buy, Hold, and Sell have the following meanings: (as of the publishing date):

BUY: ETR exceeds plus 20% or more HOLD: ETR is between zero and plus 20% SELL: ETR is less than zero

VTB Capital Research confirms that published Buy, Hold or Sell ratings conform to these definitions at the time a Target Price is established or an Investment Rating is revised. Between such revisions, day-to-day movements in the prices of financial instruments could result in a temporary discrepancy between the Investment Rating and the aforementioned definition. Analysts address such discrepancies based on their scale and duration.

UNDER REVIEW: In the event that significant information about an issuer is due to be announced or is expected to become public in the foreseeable future, or the analyst needs time to evaluate such information, which was announced recently, s/he might choose to place that issuer Under Review. This means that the analyst is suspending the previously published financial forecasts, Target Price and investment rating in order to review them while waiting for the impending information. As such, they are no longer valid and should not be relied upon.

RESTRICTED: In certain circumstances, VTB Capital is not able to communicate issuer ratings due to internal policy and/or law and regulations. In this case, any revision of the financial forecasts, Target Prices and Investment Ratings will be carried out only after the Restricted status is removed.

Notwithstanding the above, VTB Capital may from time to time issue investment recommendations predicated on a different time horizon (such as short-term trading recommendations) to that which is described above. Where VTB Capital issues such an investment recommendation, the use of an alternative time horizon for the purpose of formulating such investment recommendation might result in differences between such investment recommendation and any investment rating published in accordance with the Investment Rating system described above. In addition, short-term trading recommendations may result in short-term price movements contrary to the recommendations in this research report.

21 December 2018 |

9 |

vk.com/id446425943 |

Russian Oil and Gas |

Russia |

|

Energy: Integrated Oil & Gas |

|

The below table details the distribution of VTB Capital’s Investment Ratings on the basis of the three-tier recommendation system described above.

VTB Capital Ratings Distribution