газпром инвестиции

.pdfvk.com/id446425943

ENVIRONMENTAL POLICY AND ENERGY EFFICIENCY

COST OF ENERGY RESOURCES SAVED

through energy efficiency and energy saving programs

80

RUB 64bn

60

40

20

0

RUB bn |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

Total |

|

GAS USAGE FOR TECHNOLOGICAL NEEDS of new trunk pipelines (relative comparison1)

80 |

3-FOLD DECREASE |

|

|

60 |

|

40 |

|

20 |

|

0 |

|

RUB bn |

Central Corridor 2 |

Yamal-Europe |

Ukhta-Torzhok |

Bovanenkovo-Ukhta |

Nord Stream 1,2, |

|

|

|

|

|

TurkStream |

14

KEY PERFORMANCE INDICATOR (KPI)

target value by 2025 (compared to 2014 basis year)

Reduction of energy resources |

Reduction of greenhouse gases |

consumption for own |

emissions per unit of products |

technological usage (per unit) |

sold (СО2-equivalent per toe) |

- 5.9 % |

- 6.6 % |

|

|

GAZPROM APPLIES CERTIFIED ENVIRONMENTAL MANAGEMENT SYSTEM (ISO 14001:2015)

1 |

Normalized to same transportation distance (taken as 4,000 km for comparison purposes) |

|

2 |

Urengoy–Pomary–Uzhgorod pipeline(via Ukraine) |

STRATEGY |

|

|

|

vk.com/id446425943

LOW CARBON FOOTPRINT LEADER

CARBON FOOTPRINT OF GAZPROM’S PRODUCTION:

THE LOWEST AMONG ENERGY COMPANIES

Sands/Bitumen (LHS)

100%

90%

80%

447

70%

60%

50%

40%

378 376 375 371 371

30%

20%

10%

0%

Suncor |

Husky |

Petrobras |

Lukoil |

Rosneft |

Canadian Natural |

Crude/Condensate (LHS) |

|

NGL (LHS) |

|

Gas (LHS) |

|

|

Intensity (kgCO2e/boe) (LHS) |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

500 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

400 |

363 |

357 |

357 |

358 |

355 |

355 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

350 |

|

352 |

353 |

|

348 |

350 |

350 |

347 |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

346 |

346 |

345 |

337 |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

335 |

330 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

323 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

315 |

300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

250 |

Marathon Oil |

Occidental |

Hess |

Chevron |

Murphy Oil |

BP |

ConocoPhillips |

ExxonMobil |

Devon Energy |

Apache |

Total |

Eni |

Statoil |

OMW |

Shell |

Anadarko |

BHP Billiton |

Repsol |

Encana |

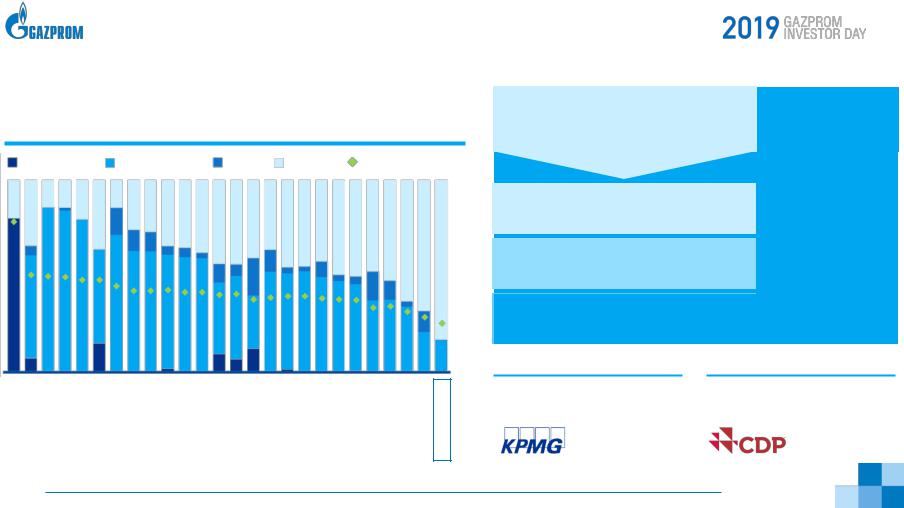

GAZPROM |

|

15 Source: CDP (2017)

STAGES IN REACHING THE

CLIMATE CHANGE GOALS

SWITCHING TO NATURAL GAS from less ecologically friendly fuels (coal power, petroleum motor fuels)

Introduction of METHANE-HYDROGEN in various sectors (without costly infrastructure changes)

Transition to hydrogen energy based on efficient low-emission technologies of

HYDROGEN PRODUCTION FROM METHANE

Proposed measures, if implemented, lead to significant emissions reduction (cumulative, EU example)

Up to 18 %

Up to 35 %

Up to 80 %

Gazprom’s GHG Emissions |

Gazprom is the leader of annual |

|

CDP Russian climate rating |

||

Reports are verified by KPMG |

||

|

STRATEGY

vk.com/id446425943

GAZPROM AT A GLANCE

SHARE IN RUSSIA’S GAS PRODUCTION |

CONVENTIONAL RESERVES |

VERTICAL INTEGRATION AND |

|

|

SINGLE EXPORT CHANNEL |

2018–2035 |

|

|

2/3+ |

~100 % |

|

|

MARKET SHARE |

|

|

EUROPE |

CHINA |

|

2018–2035 |

2018–2035 |

|

35%+ |

0%13% |

IMPORT INDEPENDENCE |

CONTRACT PORTFOLIO |

|

PRODUCTION AND TRANSPORT1 |

3+ tcm |

|

~ 95 % |

||

|

2018 |

|

1 |

Excluding equipment for LNG complex |

|

2 |

I.е. nominal capacity of Nord Stream 2, TurkStream, Powerof Siberia |

|

16 |

|

|

ADDITIONAL TRANSPORT

CAPACITY2

~125 bcm

~125 bcm

TO BE LAUNCHED IN 2019

#20251 HELIUM PRODUCER

IN THE WORLD

2035 |

|

#1 |

SUPPLIER |

TO EUROPE |

|

AND CHINA |

AVERAGE INVESTMENT

(GAS BUSINESS)

1 2018–2035

~RUB trln / year

At 01.01.2019 exchange rate (~ USD 14 bn)

STRATEGY

vk.com/id446425943

EXPORT

ELENA BURMISTROVA

Director General,

Gazprom Export

vk.com/id446425943

GAZPROM BREAKS ONE RECORD AFTER ANOTHER

EUROPEAN GAS BALANCE

100% |

4% |

8% |

8% |

3% |

|

|

5% |

|

8% |

4% |

|

|||||

|

|

|

9% |

|

||||||||||||

|

|

|

|

11% |

|

|

|

|

|

|

|

|||||

90% |

17% |

|

10% |

|

|

11% |

|

|

13% |

|

||||||

13% |

|

|

|

10% |

11% |

|

||||||||||

|

|

|

|

|

|

|

|

|

||||||||

80% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

70% |

27% |

26% |

30% |

30% |

|

|

31% |

|

|

|

|

|||||

|

|

|

|

33% |

34% |

37% |

|

|||||||||

|

|

|

|

|

|

|

|

|||||||||

60% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

50% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30% |

52% |

53% |

52% |

56% |

|

|

53% |

|

|

|

|

|||||

|

|

|

|

|

|

48% |

47% |

|

|

|||||||

|

|

|

|

|

|

|

46% |

|

||||||||

20% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2011 |

2012 |

2013 |

2014 |

|

|

2015 |

2016 |

2017 |

2018E |

|||||||

|

|

|

Indigenous production |

|

Gazprom's export |

|

LNG |

|

|

Other Imports |

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

||||||||

In 2018 Gazprom’s sales to the European market were record high of 201.8 bcm1 compared with 194.4 bcm in 2017 and 150.3 bcm in 2011.

Gazprom’s share in European consumption was up to 36.7% in 2018 vs. 34.2% in 2017 and 27.3% in 2011

Gazprom met about half of the incremental demand in 2018 and proved its ability to fill in growing supply/demand gap

While modestly increasing their share in 2018, LNG supplies to Europe still remain significantly below the 2011 record high level

Gazprom average export price increased by 24.6% yoy, up to $245.5/mcm

|

Source: PJSC Gazprom,Eurostat, National Statistics, IEA, IHS Markit |

|

|

18 |

1 |

Under Gazprom Export and Gazprom Schweiz contracts |

EXPORT |

|

|

||

|

|

||

vk.com/id446425943

UNFAVORABLE WEATHER CONDITIONS STALLED GAS DEMAND

GROWTH IN EUROPE

EUROPEAN GAS BALANCE , BCM1

|

|

|

|

|

+17.1 % |

|

|

-3.4 % |

600 |

551.4 |

542.1 |

540.5 |

|

|

541.8 |

568.8 |

549.5 |

485.6 |

506.8 |

|

||||||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

500 |

|

|

|

|

|

|

|

|

400 |

47.5% |

46.5% |

47.7% |

44.6% |

47.9% |

51.9% |

53.6% |

53.7% |

|

|

|

|

|||||

|

|

|

|

|

|

|

||

300 |

|

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

52.5% |

53.5% |

52.3% |

55.4% |

52.1% |

48.1% |

46.4% |

46.3% |

100 |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

|

|

|

|

In 2018 European demand for natural gas was down by 19 bcm compared with 2017 due to unfavorable weather conditions but was still 64 bcm above 2014.

Gas demand recovery trend originated from structural factors. In 2018 natural gas retained its position in European power generation

Declining indigenous production over the last years contributed to increased need for import

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018E |

||||

|

|

|

Indigenous production |

|

Imports requirementsCon umptionConsumption |

|

|

|

|||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||

|

1Hereinafter except as otherwise noted: European countries |

GCV = 8,850 kcal/cm, t = 20°C |

|

|

|||||||

19 |

with Turkey (excluding CIS and Baltics) |

|

|

|

Source: IEA, Eurostat, National Statistics, IHS Markit |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXPORT

vk.com/id446425943

MAJOR SUPPLIERS TO EUROPEAN MARKETS

DELIVERIES BY EUROPE’S MAJOR EXPORTERS AND PRODUCERS, BCM

|

|

|

201.8 |

|

|

|

Exporters |

|

|

|

|

Internal producers |

|

|

||||||||||||||

|

|

194.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2017 |

|

|

|

2018 |

|

|

|

150 |

|

|

|

|

|

|

|

|

|

|

|

|

134.8 |

130.5 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

100 |

|

|

|

49.4 |

48.4 |

|

|

|

|

|

|

|

|

|

|

|

45.0 |

43.7 |

|

|

39.5 |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

35.4 |

|

|

|

|

|

|

|

36.9 |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

24.1 |

23.4 |

26.5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PJSC GAZPROM |

|

ALGERIA |

|

|

QATAR |

|

OTHER LNG |

|

NORWAY* |

1 |

|

|

|

|

UNITED |

|

NETHERLANDS |

|||||||||

|

|

|

|

|

(INCL. LNG) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

KINGDOM |

|

|

|

|

||||

1Including domestic consumption, pipeline and LNG deliveries from Norway to the European market, but not LNG to Asia and America

Source: PJSC Gazprom, Eurostat, National Statistics, IEA

20

In 2018, Gazprom marked another record year, while deliveries of other suppliers except for LNG contracted

The Netherlands inched further on the path of becoming a net importer

On 2 March 2018, Gazprom set an absolute record in terms of daily export deliveries at 713.4 mmcm/d, demonstrating its robust ability

of being a swing supplier at a time of demand spikes

EXPORT

vk.com/id446425943

GAZPROM’S EXPORT ROUTES

CAPACITY UTILIZATION OF MAIN ROUTES FOR GAS SUPPLIES TO EUROPE IN 20181

|

|

Gazprom transport |

Other |

|

|

120% |

|

routes |

|

suppliers |

|

|

|

107% |

|

|

|

|

|

|

|

|

|

100% |

|

|

92% |

|

|

|

|

83% |

|

84% |

|

80% |

|

|

|

|

|

|

|

|

65% |

|

|

60% |

|

|

|

|

|

|

|

|

|

41% |

|

40% |

|

30% |

|

|

31% |

|

|

|

25% |

||

|

|

|

|

|

|

20% |

|

|

|

|

|

0% |

|

|

|

|

|

|

Finland Blue Stream |

via Belarus Nord Stream via Ukraine2 |

from Lybia3 from Algeria3 from Norway3 |

LNG 3 |

|

|

|

||||

1Deliveries under the contracts of Gazprom Export LLC

2Capacity remains unclear due to lack of accurate data on current state of the Ukrainian pipeline system

3Pipeline exports

4Including LNG trading between European countries and capacity of FSRUs

21 Source: ENTSOG, Bloomberg, IHS Markit

Gazprom transport routes demonstrated high level of capacity utilization in 2018

Utilization rate of the competing routes was at the same level or even declined

Utilization rate of LNG terminals in Europe increased from 29% in 2017 to 31% in 2018 as a result of increased LNG deliveries

EXPORT

vk.com/id446425943

GROWTH VECTOR: CHINA IS NOW WORLD’S TOP NATURAL GAS IMPORTER

GAS DEMAND IN CHINA, |

|

CHINA REMAINS THE KEY DRIVER OF |

|

GAS SUPPLY IN CHINA, |

BCM |

|

NATURAL GAS DEMAND GROWTH IN ASIA: |

|

BCM |

|

|

|

|

|

|

|

|

|

|

450

400

350

300

250

200

150

100

50

0

22

440

277

237

206

193

179

Gas demand: +17% YOY1

LNG imports: +40% YOY

Pipeline gas imports: +21% YOY

Total gas imports: +32% YOY

Gas production: +7% YOY

In 2018 Chinese gas import growth continued and China became the largest net importer of natural gas in the world (overtaking Japan).

450 |

|

|

440 |

|

|

|

|

400 |

|

|

~9% (38 bcm) |

350 |

|

|

Gazprom |

|

|

pipeline gas |

|

|

|

277 |

|

300 |

|

supplies share |

|

237 |

|

||

250 |

74 |

by 2025 |

|

|

Chinese |

||

|

53 |

||

200 |

|

demand |

|

|

51 |

||

|

42 |

|

|

150 |

|

|

|

|

|

|

|

100 |

|

157 |

|

50 |

147 |

|

|

|

|

|

|

0 |

|

|

|

-50 |

|

|

|

|

2017 |

2018E |

2025F |

2014 |

2015 |

2016 |

2017 |

2018E |

2025F |

|

|

indigenous production |

|

|

|||||||||

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

LNG imports |

|

|

|

|

|

|

|

|

|

|

1 |

Numbers below reflect 2018 growth as compared to 2017 |

|

|

pipeline gas exports2 |

|||||

|

|

||||||||

|

|

||||||||

|

|

|

|||||||

2 |

Pipeline gas exports from mainland China to Hong Kong and Macau |

|

|

|

|||||

*The difference between gas consumption and total gas supply is due to gas in transit, volumes in storage, losses and statistical discrepancies Source: IEA; General Administration of Customs, National Bureau of Statistics, National Development and Reform Commission, National

Energy Administration, People’s Republic of China; CNPC Research Institute of Economics and Technology

pipeline gas imports

(incl. from Russia via Eastern Route in 2025F)

EXPORT

vk.com/id446425943

EUROPEAN MARKET IS NOT THE FIRST OPTION FOR US LNG

ECONOMICS OF LNG SUPPLIES FROM USA

|

600 |

|

USD/mcm |

500 |

|

400 |

||

|

300

200

100

0

1 |

|

TTF, Month Ahead and Futures |

US LNG breakeven prices (full cycle costs)* |

|

|

Germany border price (BAFA) |

|

Japanese LNG Import Price |

|

||

S. Korean LNG Import Price |

|

Asian spot prices (actual and forecast) |

|

17.1 |

|

|

14.2 |

USD/mmbtu |

|

11.4 |

||

|

8.5

5.7

2.8

0.0

Hub prices significantly increased above both short-run marginal and full cycle costs of US LNG making its deliveries to Europe economically viable

However, European market is not a first choice for LNG from the USA due to higher attractiveness of other markets

1 Calculated on the basis of Henry Hub Futures prices, P = HH * 115% + X, where X – costs of liquefaction, shipping to Europe, regasification

Source: IMF, Korea Customs Service, Bloomberg, IHS Markit

23 |

|

EXPORT |

|