References—645

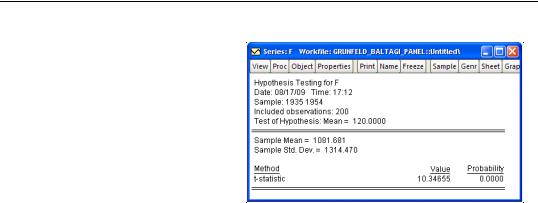

Similarly, suppose you wish to perform a hypothesis testing on a single series. Open the window for the series F, and select View/

Descriptive Statistics & Tests/ Simple Hypothesis Tests.... Enter “120” in the edit box for testing the mean value of the stacked series against a null of 120. EViews displays the results of a simple hypothesis test for the mean of the 200 observation stacked data.

While a wide variety of stacked analyses are supported, various views and procedures are not available in panel structured workfiles. You may not, for example, perform seasonal adjustment or estimate VAR or VEC models with the stacked panel.

References

Breitung, Jörg (2000). “The Local Power of Some Unit Root Tests for Panel Data,” in B. Baltagi (ed.),

Advances in Econometrics, Vol. 15: Nonstationary Panels, Panel Cointegration, and Dynamic Panels, Amsterdam: JAI Press, p. 161–178.

Choi, I. (2001). “Unit Root Tests for Panel Data,” Journal of International Money and Finance, 20: 249– 272.

Fisher, R. A. (1932). Statistical Methods for Research Workers, 4th Edition, Edinburgh: Oliver & Boyd.

Hadri, Kaddour (2000). “Testing for Stationarity in Heterogeneous Panel Data,” Econometric Journal, 3, 148–161.

Hlouskova, Jaroslava and M. Wagner (2006). “The Performance of Panel Unit Root and Stationarity Tests: Results from a Large Scale Simulation Study,” Econometric Reviews, 25, 85-116.

Holzer, H., R. Block, M. Cheatham, and J. Knott (1993), “Are Training Subsidies Effective? The Michigan Experience,” Industrial and Labor Relations Review, 46, 625-636.

Im, K. S., M. H. Pesaran, and Y. Shin (2003). “Testing for Unit Roots in Heterogeneous Panels,” Journal of Econometrics, 115, 53–74.

Johansen, Søren (1991). “Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models,” Econometrica, 59, 1551–1580.

Kao, C. (1999). “Spurious Regression and Residual-Based Tests for Cointegration in Panel Data,” Journal of Econometrics, 90, 1–44.

Levin, A., C. F. Lin, and C. Chu (2002). “Unit Root Tests in Panel Data: Asymptotic and Finite-Sample Properties,” Journal of Econometrics, 108, 1–24.

Maddala, G. S. and S. Wu (1999). “A Comparative Study of Unit Root Tests with Panel Data and A New Simple Test,” Oxford Bulletin of Economics and Statistics, 61, 631–52.

Pedroni, P. (1999). “Critical Values for Cointegration Tests in Heterogeneous Panels with Multiple Regressors,” Oxford Bulletin of Economics and Statistics, 61, 653–70.