Vector Error Correction (VEC) Models—479

•The constant or linear trend term should not be included in the Exogenous Series edit box. The constant and trend specification for VECs should be specified in the Cointegration tab (see below).

•The lag interval specification refers to lags of the first difference terms in the VEC. For example, the lag specification “1 1” will include lagged first difference terms on the right-hand side of the VEC. Rewritten in levels, this VEC is a restricted VAR with two lags. To estimate a VEC with no lagged first difference terms, specify the lag as “0 0”.

•The constant and trend specification for VECs should be specified in the Cointegration tab. You must choose from one of the five Johansen (1995) trend specifications as explained in “Deterministic Trend Specification” on page 686. You must also specify the number of cointegrating relations in the appropriate edit field. This number should be a positive integer less than the number of endogenous variables in the VEC.

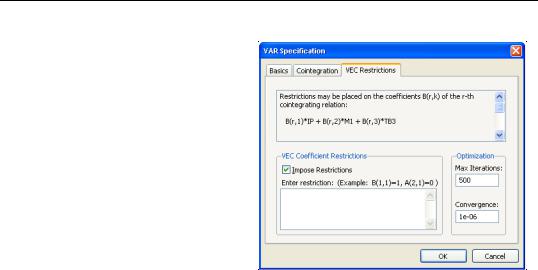

•If you want to impose restrictions on the cointegrating relations and/or the adjustment coefficients, use the Restrictions tab. “Imposing Restrictions” on page 481 describes these restriction in greater detail. Note that the contents of this tab are grayed out unless you have clicked the Vector Error Correction specification in the

VAR/VEC Specification tab.

Once you have filled the dialog, simply click OK to estimate the VEC. Estimation of a VEC model is carried out in two steps. In the first step, we estimate the cointegrating relations from the Johansen procedure as used in the cointegration test. We then construct the error correction terms from the estimated cointegrating relations and estimate a VAR in first differences including the error correction terms as regressors.

VEC Estimation Output

The VEC estimation output consists of two parts. The first part reports the results from the first step Johansen procedure. If you did not impose restrictions, EViews will use a default normalization that identifies all cointegrating relations. This default normalization expresses the first r variables in the VEC as functions of the remaining k – r variables, where r is the number of cointegrating relations and k is the number of endogenous variables. Asymptotic standard errors (corrected for degrees of freedom) are reported for parameters that are identified under the restrictions. If you provided your own restrictions, standard errors will not be reported unless the restrictions identify all cointegrating vectors.

The second part of the output reports results from the second step VAR in first differences, including the error correction terms estimated from the first step. The error correction terms are denoted CointEq1, CointEq2, and so on in the output. This part of the output has the same format as the output from unrestricted VARs as explained in “VAR Estimation Output” on page 461, with one difference. At the bottom of the VEC output table, you will see two log likelihood values reported for the system. The first value, labeled Log Likelihood (d.f. adjusted), is computed using the determinant of the residual covariance matrix (reported as

Vector Error Correction (VEC) Models—481

Obtaining Coefficients of a VEC

For VEC models, the estimated coefficients are stored in three different two dimensional arrays: A, B, and C. A contains the adjustment parameters a , B contains the cointegrating vectors b¢, and C holds the short-run parameters (the coefficients on the lagged first difference terms).

•The first index of A is the equation number of the VEC, while the second index is the number of the cointegrating equation. For example, A(2,1) is the adjustment coefficient of the first cointegrating equation in the second equation of the VEC.

•The first index of B is the number of the cointegrating equation, while the second index is the variable number in the cointegrating equation. For example, B(2,1) is the coefficient of the first variable in the second cointegrating equation. Note that this indexing scheme corresponds to the transpose of b .

•The first index of C is the equation number of the VEC, while the second index is the variable number of the first differenced regressor of the VEC. For example, C(2, 1) is the coefficient of the first differenced regressor in the second equation of the VEC.

You can access each element of these coefficients by referring to the name of the VEC followed by a dot and coefficient element:

var01.a(2,1)

var01.b(2,1)

var01.c(2,1)

To see the correspondence between each element of A, B, and C and the estimated coefficients, select View/Representations from the VAR toolbar.

Imposing Restrictions

Since the cointegrating vector b is not fully identified, you may wish to impose your own identifying restrictions when performing estimation.

Vector Error Correction (VEC) Models—483

A(i,1)*CointEq1 + A(i,2)*CointEq2 + ... + A(i,r)*CointEqr

Restrictions on the adjustment coefficients are currently limited to linear homogeneous restrictions so that you must be able to write your restriction as R vec(a) = 0 , where R is a known qk ¥ r matrix. This condition implies, for example, that the restriction,

A(1,1) = A(2,1)

is valid but:

A(1,1) = 1

will return a restriction syntax error.

One restriction of particular interest is whether the i-th row of the a matrix is all zero. If this is the case, then the i-th endogenous variable is said to be weakly exogenous with respect to the b parameters. See Johansen (1995) for the definition and implications of weak exogeneity. For example, if we assume that there is only one cointegrating relation in the VEC, to test whether the second endogenous variable is weakly exogenous with respect to b you would enter:

A(2,1) = 0

To impose multiple restrictions, you may either separate each restriction with a comma on the same line or type each restriction on a separate line. For example, to test whether the second endogenous variable is weakly exogenous with respect to b in a VEC with two cointegrating relations, you can type:

A(2,1) = 0

A(2,2) = 0

You may also impose restrictions on both b and a . However, the restrictions on b and a must be independent. So for example,

A(1,1) = 0

B(1,1) = 1

is a valid restriction but:

A(1,1) = B(1,1)

will return a restriction syntax error.

Identifying Restrictions and Binding Restrictions

EViews will check to see whether the restrictions you provided identify all cointegrating vectors for each possible rank. The identification condition is checked numerically by the rank of the appropriate Jacobian matrix; see Boswijk (1995) for the technical details. Asymptotic standard errors for the estimated cointegrating parameters will be reported only if the restrictions identify the cointegrating vectors.