Single-Equation Cointegration Tests—695

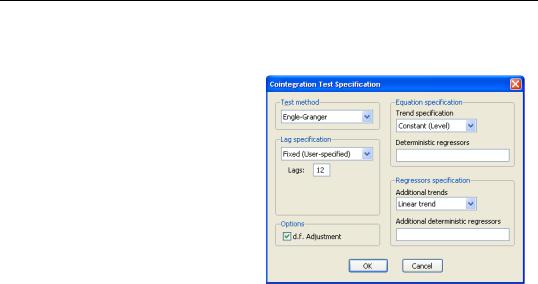

Test/Single-Equation Cointegration Test from the group toolbar or main menu. The Cointegration Test Specification page opens to prompt you for information about the test.

The combo box at the top allows you to choose between the default EngleGranger test or the Phillips-Ouliaris test. Below the combo are the options for the test statistic. The Engle-Granger test requires a specification for the number of lagged differences to include in the test regression, and whether to d.f. adjust the standard error estimate when forming the ADF test statistics. To match Hamilton’s example, we specify a Fixed (Userspecified) lag specification of 12, and retain the default d.f. correction of the standard error estimate.

The right-side of the dialog is used to specify the form of the cointegrating equation. The main cointegrating equation is described in the Equation specification section. You should use the Trend specification combo to choose from the list of pre-specified deterministic trend variable assumptions (None, Constant (Level), Linear Trend, Quadratic Trend). If you wish to include deterministic regressors that are not offered in the pre-specified list, you may enter the series names or expressions in the Deterministic regressors edit box. For our example, we will leave the settings at their default values, with the Trend specification set to Constant (Level), and no additional deterministic regressors specified.

The Regressors specification section should be used to specify any deterministic trends or other regressors that should be included in the regressors equations but not in the cointegrating equation. In our example, Hamilton points to evidence of non-zero drift in the regressors, so we will select Linear trend in the Additional trends combo.

Click on OK to compute and display the test results.

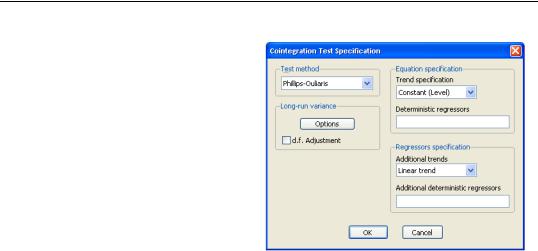

Single-Equation Cointegration Tests—697

The right-hand side of the dialog, which describes the cointegrating regression and regressors specifications, should be specified as before.

The left-hand side of the dialog changes to show a single Options button for controlling the estimation of the Long-run variance used in the Phillips-Ouliaris test, and the checkbox for d.f Adjustment of the variance estimates. The default settings instruct EViews to compute these long-run variances using a non-prewhitened

Bartlett kernel estimator with a fixed Newey-West bandwidth. We match the Hamilton example settings by turning off the d.f. adjustment and by clicking on the Options button and using the Bandwidth method combo to specify a User-specified bandwidth value of 13.

Click on the OK button to accept the Options, then on OK again to compute the test statistics and display the results: