378—Chapter 15. Super Models

Our new graph (which we have prettied-up) shows both baseline and scenario 1 results. Putting the deviation on a separate scale makes it easier to see the effect of this fiscal policy experiment. With a little luck, these results will get us a very good grade.

Simulating VARs

Models can be used for solving complicated systems of equations under different scenarios, as we’ve done above. Models can also be used for forecasting dynamic systems of equations. This is especially useful in forecasting from vector autoregressions.

Hint: The  feature in equations handles dynamic forecasting from a single equation quite handily. Here we’re talking about forecasting from multiple equation models.

feature in equations handles dynamic forecasting from a single equation quite handily. Here we’re talking about forecasting from multiple equation models.

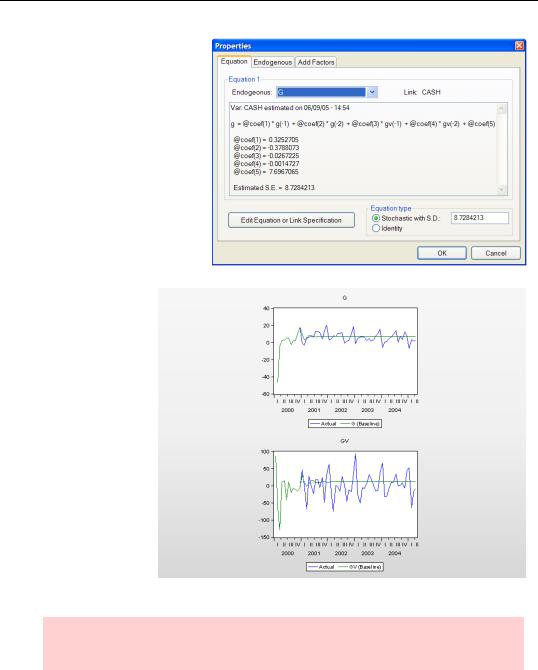

Open the workfile “currencymodel.wf1” which contains the vector autoregression estimated in Chapter 14, “A Taste of Advanced Estimation.” Create a new model object named CURRENCY_FORECAST. Copy

the VAR object CASH from the workfile window and paste it into the model, which now looks as shown to the right.

Simulating VARs—379

Double-click on the equation. The equation for G (growth in currency in the hands of the public) has been copied in together with the estimated coefficients and the estimated standard error of the error terms in the equation. Remember, this is a live link, so:

•If you re-estimate the VAR, the model will know to use the reestimated coefficients.

We can now use the model to forecast from the VAR. Click  , set the Solution sample to 2001 2005, and hit

, set the Solution sample to 2001 2005, and hit  . Then do

. Then do

Proc/Make Graph…. Check both Actuals and Active and set the

Sample for Graph to 2000M1 2005M4.

In this particular example, the vector autoregres-

sion did a good job of forecasting for several periods and essentially flatlined by a year out.

Hint: If you prefer, instead of creating a model and then copying in a VAR you can use Proc/Make Model from inside the VAR to do both at once.

The model taught in our introductory economics course was linear because it’s hard for people to solve nonlinear models. Computers are generally fine with nonlinear models,

380—Chapter 15. Super Models

although there are some nonlinear models that are too hard for even a computer to solve. For the most part though, the steps we just walked through would have worked just as well for a set of nonlinear equations.

Rich Super Models

The model object provides a rich set of facilities for everything from solving intro homework problems to solving large scale macroeconometric models. We’ve only been able to touch the surface. To help you explore further on your own, we list a few of the most prominent features:

•Models can be nonlinear. Various controls over the numerical procedures used are provided for hard problems. Diagnostics to track the solution process are also available when needed.

•Add factors can be used to adjust the value of a specified variable. You can even use add factors to adjust the solution for a particular variable to match a desired target.

•Equations can be implicit. Given an equation such as logy = x2 , EViews can solve for y. Add factors can be used for implicit equations as well.

•Stochastic simulations in which you specify the nature of the random error term for each equation are a built-in feature. This allows you to produce a statistical distribution of solutions in place of a point estimate.

•Equations can contain future values of variables. This means that EViews can solve dynamic perfect foresight models.

•Single-variable control problems of the following sort can be solved automatically. You can specify a target path for one endogenous variable and then instruct EViews to change the value of one exogenous variable that you specify in order to make the solved-for values of the endogenous variable match the target path.

Quick Review

A model is a collection of equations, either typed in directly or linked from objects in the workfile. The central feature of the model object is the ability to find the simultaneous solution of the equations it contains. Models also include a rich set of facilities for exploring various assumptions about the exogenous driving variables of the model and the effect of shocks to equations.