ARCH, etc.—351

Logit’s Forecast dialog offers a choice of predicting the index s, or the probability. Here we predict the probability.

The graph shown to the right plots the probability of union membership as a function of age. For comparison purposes, we’ve added a horizontal line marking the unconditional probability of union membership. A 60 year old is about three times as likely to be in a union as is a 20 year old.

ARCH, etc.

Have you tried About EViews on the Help menu and then clicked the  button? Only one Nobel prize winner (so far!) appears in the credits list. Which brings us to the topic of autoregressive conditional heteroskedasticity, or ARCH. ARCH, and members of the extended ARCH family, model time-varying variances of the error term. The simplest ARCH model is: yt = aˆ + bˆ xt + et

button? Only one Nobel prize winner (so far!) appears in the credits list. Which brings us to the topic of autoregressive conditional heteroskedasticity, or ARCH. ARCH, and members of the extended ARCH family, model time-varying variances of the error term. The simplest ARCH model is: yt = aˆ + bˆ xt + et

jt2= g0 + g1e2t – 1

In this ARCH(1) model, the variance of this period’s error term depends on the squared residual from the previous period.

352—Chapter 14. A Taste of Advanced Estimation

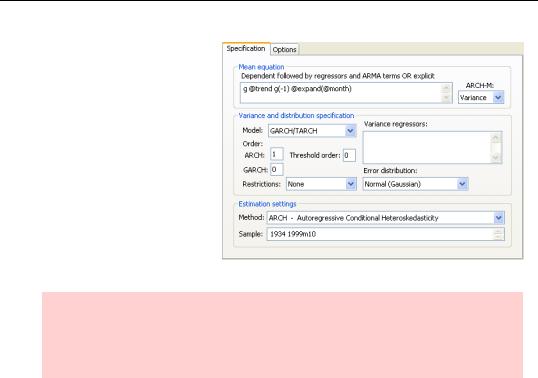

The residuals from the currency data used earlier showed noticeably persistent volatility, a sign of a potential ARCH effect. In EViews, all the action in specifying ARCH takes place in the Specification tab of the Equation Estimation dialog. To get to the right version of the Specification tab, choose ARCH -

Autoregressive Conditional Heteroskedasticity in the

Method dropdown of the Estimation settings field.

Hint: Unlike nearly all other EViews estimation procedures, ARCH requires a continuous sample. Define an appropriate sample in the Specification tab. If your sample includes a break, EViews will give an error message. In this example, we had to use a subset of our data to accommodate the continuous sample requirement.

ARCH, etc.—353

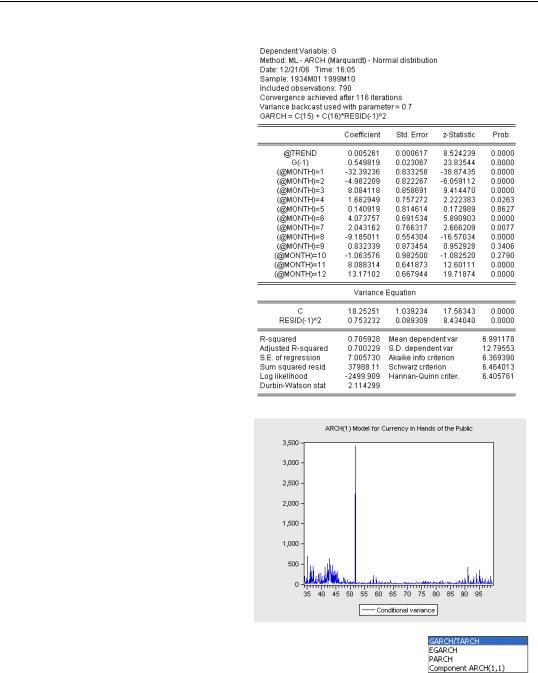

ARCH coefficients appear below the structural coefficients. The ARCH coefficient—our estimated g1 —is

both large, 0.75, and statistically significant, t = 8.4 .

In addition to the usual results, the

View menu offers Garch Graph.

Garch Graph provides a plot of the predicted conditional variance or the conditional standard deviation.

Selecting Garch Graph/Conditional Variance, we see that higher variances occur early and late in the sample, plus an enormous spike in 1952.

Perhaps the variance spike is really

there, or perhaps ARCH(1) isn’t the best model. EViews offers a wide choice from the extended ARCH family. The Model dropdown offers four broad choices. Each broad choice is further refined with various

options. Most simply, you can specify the order of the ARCH or GARCH (Generalized ARCH) model in the dialog fields just below Model.

354—Chapter 14. A Taste of Advanced Estimation

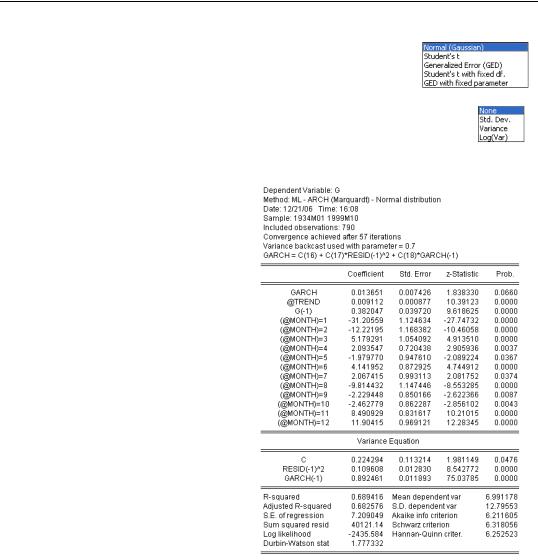

You can also choose from a variety of error distributions using the

Error distribution dropdown.

One of the most interesting applications of ARCH is to put the timevarying variance back into the structural equation. This is called ARCH-in-

mean, or ARCH-M, and is added to the specification using the ARCH-M dropdown menu in the upper right of the Specification tab.

Here we’ve changed the model to GARCH(1,1) and entered the variance in the structural equation. EViews labels the structural coefficient of the ARCH-M effect GARCH. Notice that the structural effect of ARCH-M is almost significant at the five percent level.