648 |

PART TEN MONEY AND PRICES IN THE LONG RUN |

wealth. Most farmers in the western part of the country were debtors. Their creditors were the bankers in the east. When the price level fell, it caused the real value of these debts to rise, which enriched the banks at the expense of the farmers.

According to populist politicians of the time, the solution to the farmers’ problem was the free coinage of silver. During this period, the United States was operating with a gold standard. The quantity of gold determined the money supply and, thereby, the price level. The free-silver advocates wanted silver, as well as gold, to be used as money. If adopted, this proposal would have increased the money supply, pushed up the price level, and reduced the real burden of the farmers’ debts.

The debate over silver was heated, and it was central to the politics of the 1890s. A common election slogan of the populists was “We Are Mortgaged. All But Our Votes.” One prominent advocate of free silver was William Jennings Bryan, the Democratic nominee for president in 1896. He is remembered in part for a speech at the Democratic party’s nominating convention in which he said, “You shall not press down upon the brow of labor this crown of thorns. You shall not crucify mankind upon a cross of gold.” Rarely since then have politicians waxed so poetic about alternative approaches to monetary policy. Nonetheless, Bryan lost the election to Republican William McKinley, and the United States remained on the gold standard.

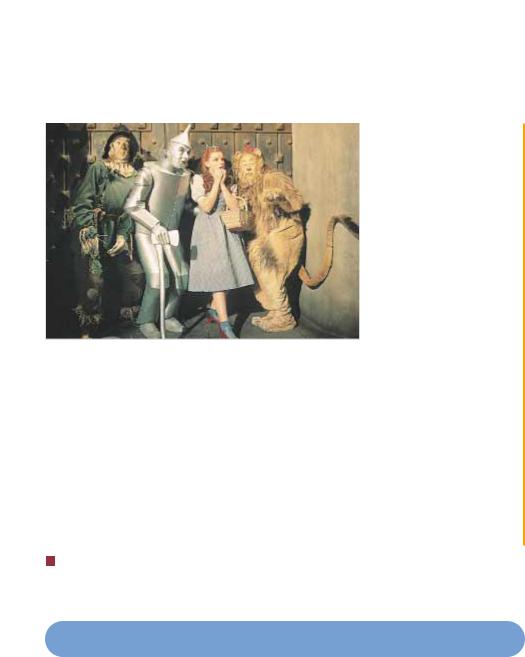

L. Frank Baum, the author of the book The Wonderful Wizard of Oz, was a midwestern journalist. When he sat down to write a story for children, he made the characters represent protagonists in the major political battle of his time. Although modern commentators on the story differ somewhat in the interpretation they assign to each character, there is no doubt that the story highlights the debate over monetary policy. Here is how economic historian Hugh Rockoff, writing in the August 1990 issue of the Journal of Political Economy, interprets the story:

DOROTHY: Traditional American values

TOTO: Prohibitionist party, also called the

Teetotalers

SCARECROW: Farmers

TIN WOODSMAN: Industrial workers

COWARDLY LION: William Jennings Bryan

MUNCHKINS: Citizens of the east

WICKED WITCH OF THE EAST: Grover Cleveland

WICKED WITCH OF THE WEST: William McKinley

WIZARD: Marcus Alonzo Hanna, chairman of the

Republican party

OZ: Abbreviation for ounce of gold

YELLOW BRICK ROAD: Gold standard

In the end of Baum’s story, Dorothy does find her way home, but it is not by just following the yellow brick road. After a long and perilous journey, she learns that the wizard is incapable of helping her or her friends. Instead, Dorothy finally discovers the magical power of her silver slippers. (When the book was

CHAPTER 28 MONEY GROWTH AND INFLATION |

649 |

AN EARLY DEBATE OVER

MONETARY POLICY

made into a movie in 1939, Dorothy’s slippers were changed from silver to ruby. Apparently, the Hollywood filmmakers were not aware that they were telling a story about nineteenth-century monetary policy.)

Although the populists lost the debate over the free coinage of silver, they did eventually get the monetary expansion and inflation that they wanted. In 1898 prospectors discovered gold near the Klondike River in the Canadian Yukon. Increased supplies of gold also arrived from the mines of South Africa. As a result, the money supply and the price level started to rise in the United States and other countries operating on the gold standard. Within 15 years, prices in the United States were back to the levels that had prevailed in the 1880s, and farmers were better able to handle their debts.

QUICK QUIZ: List and describe six costs of inflation.

CONCLUSION

This chapter discussed the causes and costs of inflation. The primary cause of inflation is simply growth in the quantity of money. When the central bank creates money in large quantities, the value of money falls quickly. To maintain stable prices, the central bank must maintain strict control over the money supply.

The costs of inflation are more subtle. They include shoeleather costs, menu costs, increased variability of relative prices, unintended changes in tax liabilities, confusion and inconvenience, and arbitrary redistributions of wealth. Are these costs, in total, large or small? All economists agree that they become huge during hyperinflation. But their size for moderate inflation—when prices rise by less than 10 percent per year—is more open to debate.

Although this chapter presented many of the most important lessons about inflation, the discussion is incomplete. When the Fed reduces the rate of money growth, prices rise less rapidly, as the quantity theory suggests. Yet as the economy makes the transition to this lower inflation rate, the change in monetary policy will have disruptive effects on production and employment. That is, even though monetary policy is neutral in the long run, it has profound effects on real variables in

650 |

PART TEN MONEY AND PRICES IN THE LONG RUN |

|

|

|

|

IN THE NEWS

How to Protect Your Savings from Inflation

3 percent, if someone had bought

30-year government bond yielding percent, he would have expected by now his investment would be 180 percent of its original value. However, after years of higher-than- d inflation, the investment is only 85 percent of its original

.

Because inflation has been modin recent years, many people today not worried about how it will affect savings. This complacency is danEven a low rate of inflation can seriously erode savings over long peri-

of time.

Imagine that you retire today with a invested in Treasury bonds pay a fixed $10,000 each year,

the reasons for short-run moneunderstanding of the causes and costs

Summar y

The overall level of prices in an economy adjusts to bring money supply and money demand into balance. When the central bank increases the supply of money, it causes the price level to rise. Persistent growth in the quantity of money supplied leads to continuing inflation.

The principle of monetary neutrality asserts that changes in the quantity of money influence nominal variables but not real variables. Most economists believe that monetary neutrality approximately describes the behavior of the economy in the long run.

652 |

PART TEN MONEY AND PRICES IN THE LONG RUN |

Key Concepts

quantity theory of money, p. 632 nominal variables, p. 633

real variables, p. 633 classical dichotomy, p. 633

effect, p. 640 shoeleather costs, p. 642 costs, p. 644

1.Explain how an increase in the value of money.

2.According to the quantity theory effect of an increase in the quantity

3.Explain the difference between variables, and give two examples the principle of monetary neutrality, affected by changes in the quantity

4.In what sense is inflation like a about inflation as a tax help

Fisher effect, how does an increase in affect the real interest rate and the

of inflation? Which of these costs do important for the U.S. economy?

than expected, who benefits—debtors

.

Problems and Applications

1.Suppose that this year’s money supply is $500 billion, nominal GDP is $10 trillion, and real GDP is $5 trillion.

a.What is the price level? What is the velocity of money?

b.Suppose that velocity is constant and the economy’s output of goods and services rises by 5 percent each year. What will happen to nominal GDP and the price level next year if the Fed keeps the money supply constant?

c.What money supply should the Fed set next year if it wants to keep the price level stable?

d.What money supply should the Fed set next year if it wants inflation of 10 percent?

2.Suppose that changes in bank regulations expand the availability of credit cards, so that people need to hold less cash.

a.How does this event affect the demand for money?

b.If the Fed does not respond to this event, what will happen to the price level?

c.If the Fed wants to keep the price level stable, what should it do?

3.It is often suggested that the Federal Reserve try to achieve zero inflation. If we assume that velocity is constant, does this zero-inflation goal require that the rate of money growth equal zero? If yes, explain why. If no, explain what the rate of money growth should equal.

4.The economist John Maynard Keynes wrote: “Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens.” Justify Lenin’s assertion.

5.Suppose that a country’s inflation rate increases sharply. What happens to the inflation tax on the holders of money? Why is wealth that is held in savings accounts not subject to a change in the inflation tax? Can you think of any way in which holders of savings accounts are hurt by the increase in the inflation rate?

6.Hyperinflations are extremely rare in countries whose central banks are independent of the rest of the government. Why might this be so?

658 |

PART ELEVEN THE MACROECONOMICS OF OPEN ECONOMIES |

closed economy

an economy that does not interact with other economies in the world

open economy

an economy that interacts freely with other economies around the world

country to specialize in producing those goods and services in which it has a comparative advantage.

So far our development of macroeconomics has largely ignored the economy’s interaction with other economies around the world. For most questions in macroeconomics, international issues are peripheral. For instance, when we discussed the natural rate of unemployment in Chapter 26 and the causes of inflation in Chapter 28, the effects of international trade could safely be ignored. Indeed, to keep their analysis simple, macroeconomists often assume a closed economy—an economy that does not interact with other economies.

Yet some new macroeconomic issues arise in an open economy—an economy that interacts freely with other economies around the world. This chapter and the next one, therefore, provide an introduction to open-economy macroeconomics. We begin in this chapter by discussing the key macroeconomic variables that describe an open economy’s interactions in world markets. You may have noticed mention of these variables—exports, imports, the trade balance, and exchange rates—when reading the newspaper or watching the nightly news. Our first job is to understand what these data mean. In the next chapter we develop a model to explain how these variables are determined and how they are affected by various government policies.

THE INTERNATIONAL FLOWS OF GOODS AND CAPITAL

expor ts

goods and services that are produced domestically and sold abroad

impor ts

goods and services that are produced abroad and sold domestically

net expor ts

the value of a nation’s exports minus the value of its imports, also called the trade balance

trade balance

the value of a nation’s exports minus the value of its imports, also called net exports

trade surplus

an excess of exports over imports

An open economy interacts with other economies in two ways: It buys and sells goods and services in world product markets, and it buys and sells capital assets in world financial markets. Here we discuss these two activities and the close relationship between them.

THE FLOW OF GOODS: EXPORTS, IMPORTS,

AND NET EXPORTS

As we first noted in Chapter 3, exports are domestically produced goods and services that are sold abroad, and imports are foreign-produced goods and services that are sold domestically. When Boeing, the U.S. aircraft manufacturer, builds a plane and sells it to Air France, the sale is an export for the United States and an import for France. When Volvo, the Swedish car manufacturer, makes a car and sells it to a U.S. resident, the sale is an import for the United States and an export for Sweden.

The net exports of any country are the value of its exports minus the value of its imports. The Boeing sale raises U.S. net exports, and the Volvo sale reduces U.S. net exports. Because net exports tell us whether a country is, in total, a seller or a buyer in world markets for goods and services, net exports are also called the trade balance. If net exports are positive, exports are greater than imports, indicating that the country sells more goods and services abroad than it buys from other countries. In this case, the country is said to run a trade surplus. If net

CHAPTER 29 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS |

659 |

“But we’re not just talking about buying a car—we’re talking about confronting this country’s trade deficit with Japan.”

exports are negative, exports are less than imports, indicating that the country sells fewer goods and services abroad than it buys from other countries. In this case, the country is said to run a trade deficit. If net exports are zero, its exports and imports are exactly equal, and the country is said to have balanced trade.

In the next chapter we develop a theory that explains an economy’s trade balance, but even at this early stage it is easy to think of many factors that might influence a country’s exports, imports, and net exports. Those factors include the following:

The tastes of consumers for domestic and foreign goods

The prices of goods at home and abroad

The exchange rates at which people can use domestic currency to buy foreign currencies

The incomes of consumers at home and abroad

The cost of transporting goods from country to country

The policies of the government toward international trade

As these variables change over time, so does the amount of international trade.

trade deficit

an excess of imports over exports

balanced trade

a situation in which exports equal imports

CASE STUDY THE INCREASING OPENNESS

OF THE U.S. ECONOMY

Perhaps the most dramatic change in the U.S. economy over the past five decades has been the increasing importance of international trade and finance. This change is illustrated in Figure 29-1, which shows the total value of goods and services exported to other countries and imported from other countries expressed as a percentage of gross domestic product. In the 1950s exports of goods and services averaged less than 5 percent of GDP. Today they are more than twice that level and still rising. Imports of goods and services have risen by a similar amount.