Consulting on productivity and performance improvement

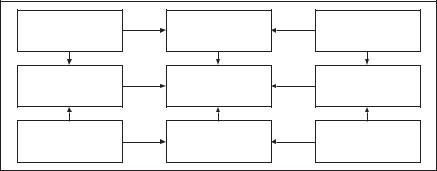

Figure 20.3 The contribution of productivity to profits

Change in |

Change in |

Change in |

sales volumes |

revenue |

selling prices |

Change in |

Change in |

Change in |

productivity |

profit |

price recovery |

Change in |

Change in |

Change in |

purchase quantity |

purchase costs |

purchase prices |

Source: Adapted from European Association of National Productivity Centres (EANPC): “Productivity, innovation, quality of working life and environment”, in Memorandum (Brussels), Feb. 1999, p. 6.

various stakeholders – customers, employees, stockholders, owners, suppliers and communities – an organization can avoid the shortsightedness that often results from focusing on a single measure of success.

As is the case with any organizational change (see Chapter 4), consultants may meet some resistance to productivity and performance measurement. Reasons may include potential misunderstanding and misuse of measurement, fear of exposure of inadequate performance, additional time and reporting demands, reduction of autonomy, and others. Implementing a productivity measurement system is an organizational change and should be managed as a change process.

20.3Approaches and strategies to improve productivity

There are many approaches to improving organizational productivity and performance, ranging from incremental, small-steps improvement to radical strategic changes. One of the most important tasks of the productivity consultant is to make conscious and educated judgements on the needs of the client organization. Does the organization have the potential and reserves to cope with incremental continuous improvements? Or is the client already in a situation where only radical strategic intervention can help? The two approaches will be considered separately.

Incremental continuous improvement

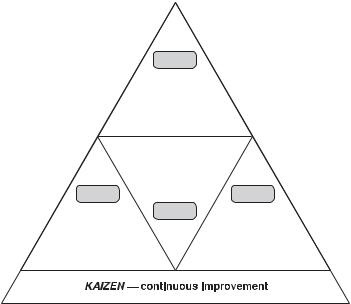

The essence of incremental continuous improvement is reflected in the kaizen approach developed in Japan and described in many publications. It involves making continuous small improvements that require little or no investment,

445

Management consulting

Figure 20.4 Kaizen building-blocks

|

TQM |

|

total |

|

quality |

|

management |

|

total |

|

productive |

|

maintenance |

TEI |

JIT |

|

TPM |

total |

just |

employee |

in |

involvement |

time |

Source: J. DeWeese: “The people–machine connection at Texas Instruments”, in National Productivity Review (New York), Summer 1999, p. 40.

involving all employees in making them, and providing structured opportunities, systems and tools for increasing productivity. Its main objectives could be, for example, eliminating waste, reducing defects, keeping the workplace tidy, improving quality, and developing good working habits. The main building-blocks of kaizen are total employee involvement (TEI), just-in-time (JIT), total productive maintenance (TPM) and TQM (figure 20.4).

For example, kaizen involves workers in maintenance operations by harnessing the symbiotic relationships between processes, operators and maintenance technicians through:

●taking positive actions to eliminate barriers to operator maintenance

●training operators to perform routine set-up and maintenance tasks

●supporting a steady stream of process modification projects, and

●rotating operators to interesting jobs elsewhere in the organization.

The most important task of continuous improvement is to achieve sustainable growth in productivity through elimination of all kinds of waste – of materials, energy, labour-time, machine-time – anything that does not provide value to the customer. Sources of waste could be poor design, inappropriate technology, wrong choice of materials, carelessness, improper work methods, material scrap, rejects, pollutants, movement inventories, machine breakdown, delays in obtaining

446

Consulting on productivity and performance improvement

repairs and other services, inefficient space utilization, employees’problems, idle money, work in process, and many others.

A preventive approach focused on reducing the generation of waste is most effective. The development of waste management indices, such as the reduction index, collection index, recovery index, and disposal index, at various stages of the process can help in monitoring and reducing waste and improving productivity. One such effective approach to reducing waste and improving the quality of environment is the green productivity approach developed and popularized recently by the Asian Productivity Organization (box 20.1).

Another important task of continuous improvement could be saving on small capital expenditures. Here we are not talking about strategic investments, but small amounts of money within the approved budget. But are they really small? Any company can create far more sustainable value by reducing its capital expenditures through rigorous evaluation of the small-ticket items that are usually rubber-stamped. Those “little” requests – which could take up to 80 per cent of the remaining budget after strategic items – often prove to be unnecessary (duplicating other requests) or very expensive. But few managers have the time, energy, or inclination to question their justification.

It may be useful to ask the following eight questions concerning small-ticket capital budget items, as suggested by T. Copeland:4

To operating managers:

●Is this your investment to make? Often a unit manager will overstep his or her boundaries and put in a request for an investment that is someone else’s responsibility.

●Does it really have to be new? Overall costs can be 30 to 40 per cent lower if a company continues using an existing machine for five more years instead of buying a new one.

●How are our competitors meeting compliance needs? A good way to combat conservative and costly compliance with different regulations is to require unit managers to look into the practices of other companies.

To senior managers:

●Is the left hand duplicating investment already made by the right? Many organizations with complicated operations have a tendency to accumulate excess capacity, sometimes up to 70 per cent.

●Are the trade-offs between profits and capital spending well understood?

Often managers will request new assets, neglecting future productivity and creating a culture that places earnings above all other performance measures.

●Are there signs of budget “massage”? It is common for unit managers to be reluctant to propose reductions in their capital spending, for fear that the head office will not be generous when they need an increase. On the other hand, asking for more money could provoke an encounter with internal auditors. So they “massage” the budget, shuffling expenditures between budgets items or spending money urgently before the end of the budget year.

447

Management consulting

Box 20.1 Green productivity practices

Steps |

Tasks |

||

I. |

Get started |

1. |

Formation of green productivity team |

|

|

2. |

Walk-through survey of the production |

|

|

|

process |

|

|

3. |

Preliminary identification of waste- |

|

|

|

generating operations |

II. |

Analyse process steps |

4. |

Detailed process study |

5.Preparation of process and activity flow chart

6.Preparation of materials balance

7.Identification and characterization of sources of waste

8.Assignment of costs to waste streams

III.Conduct energy audit 9. Causal analysis for waste generation from

known sources

|

10. |

Identification of energy usage areas |

|

11. |

Preparation of energy balance |

|

12. |

Identification of energy losses |

V. Generate waste |

13. |

Causal analysis for energy loss |

prevention options |

14. |

Process optimization studies |

|

15.Development of waste prevention options

V.Select waste prevention 16. Preliminary selection of workable options

solutions |

17. |

Assessment of technical feasibility |

|

||

|

18. |

Assessment of economic impact |

VI. Implement waste |

19. |

Evaluation of environmental aspects |

prevention solution |

20. |

Preparation of implementation plan |

|

21. |

Implementation of waste prevention |

|

|

solution |

VII. Study pollution control |

22. Monitoring and evaluation of results |

|

|

23. |

Treatability studies of effluents |

|

24. |

Design of appropriate pollution-control |

|

|

systems |

|

25. |

Implementation of pollution-control |

|

|

system |

VIII. Maintain green |

26. |

Performance evaluation of pollution- |

productivity |

|

control system |

|

27. |

Sustain waste prevention and control |

Go to step II |

28. |

Identify and select next focus area |

448

Consulting on productivity and performance improvement

Questions to be put at the end of the process:

●Are shared assets fully used? Businesses in networks may use a lot of shared assets, and are thus highly sensitive to slow-moving bureaucratic procedures. If shared assets are not fully used most of the time, it means that a company has problems with coordination.

●How fine-grained are capacity estimates? If measurements of need for equipment are not adequately fine-grained, managers can underestimate the capacity of equipment networks.

Quantum leaps and large-scale strategic improvements

“Quantum leap” improvements are necessary to achieve dramatic breakthroughs in products and services design and delivery, competitiveness, creation of new markets and similar. The changes are drastic and require considerable investment in new technology, equipment, and product development, as well as major changes in production processes. Such changes are normally organi- zation-wide and affect a large number of employees. The gains can be substantial and strategic in nature, but resistance and difficulties in implementation are likely to be much higher than with kaizen.

Approaches and programmes that produce major improvements in productivity and performance exhibit one common characteristic. They do not start by identifying and dissecting current problems, shortcomings and underutilized resources with the intention of devising a better method and so increasing productivity. Their starting-point is the client’s vision of the future and a strong desire to translate this vision into reality. This vision could be to become a sector leader, achieve a significant competitive advantage, offer a completely new sort of product or service, or cut costs by 30–40 per cent.

The most important method for achieving new and ambitious goals is strategic management coupled with productivity improvement programmes or projects (PIP). Strategic management requires a business strategy defining the business in which the organization operates (“the right things to do”) and capability strategies defining the organization’s general capabilities and operational competencies (“to do things right”). With this approach, productivity and performance improvement can be directed to a future purpose, which serves as the main common target and driving force for the consultant and the client. It helps the client organization to develop a long-term perspective within which to determine and realize short-term goals, and to learn to work towards its purpose over time. We mention below a few choices related to performance improvement that are emerging as a result of recent shifts in the business environment.

Innovative or adaptive strategies? The most basic choice, which makes the further design of strategy easier, is between an innovative and an adaptive strategy. An innovative strategy means investing in productive capability or new combinations of inputs which generate higher-quality, lower-cost outputs. In contrast, an adaptive strategy does not attempt to upgrade and recombine the firm’s

449

Management consulting

assets and inputs. In its extreme form, an adaptive strategy can entail disinvestments, which reduces the ability to create value tomorrow; it extracts value today without putting new value-creating capabilities in its place, thus reducing the ability to compete. An adaptive strategy can make sense in the short or medium term. An innovative strategy is a development process that takes time and a delay in its introduction can make it more difficult to develop an effective innovative response.

Competitive advantage through strategic capabilities. Winners in the global marketplace demonstrate management capability to coordinate and redeploy competencies within the organization. These dynamic capabilities must be tuned to customer needs; they should be unique or difficult to replicate so that products and services can be priced with little regard for competition. Any assets that can be bought and sold at an established price, that can readily be assembled through markets, or that can be replicated through formal contracts with a portfolio of business units cannot be considered as strategic. A capability that is difficult to replicate or imitate can be considered a distinctive competence.

Competitive growth strategies. Companies that select the growth path as their main direction have to apply special growth-oriented strategies. Growth is hard to achieve and even harder to sustain. Three general conclusions emerged from a 1999 review of the fastest-growing companies:5 young growing companies need to see themselves as much larger enterprises almost immediately; sustaining value-creating growth requires heavy investment in IT, R&D and capital assets; and the ability to form and manage alliances to share learning is a key strategy for companies of all sizes and in all sectors.

Moving down the value chain. Providing services is generally more lucrative than making products. The top companies are starting to create new business models to capture profits at the customer end of the value chain. They have gone “downstream”, towards the customer, to tap into valuable economic activity that occurs throughout the entire production cycle. Downstream markets offer important benefits besides revenue. They tend to have higher margins and require fewer assets than manufacturing. And because they tend to provide steady service-revenue streams, they often work against business cycles and provide more economic stability. To capture value downstream, producers have to expand their definition of the value chain, shift their focus from operations to customer allegiance, and look again at their vertical integration.

Customers as partners in innovations. Businesses today consider customers as an important source of information, and as partners in R&D and producttesting. Thanks largely to the Internet, consumers increasingly engage in active dialogue with manufacturers, and create and compete for value, becoming a new source of competence for corporations. For example, more than 650,000 customers tested a beta version of Windows 2000® and reported back on their ideas for changing some of the product features. The value of this collective R&D

450

Consulting on productivity and performance improvement

investment by customers was estimated at more than US$500 million.6 Dialogue with customers dramatically improves organizational flexibility.

The following assumptions are of critical importance in designing strategies for radical improvements in productivity and performance:

●The future is more important then the past.

●Intangibles are more important than tangibles.

●Speed is intrinsic to economic value.

●Derivatives become the core events.

●Wealth comes more often from the periphery than from the centre.

Combining strategies

The two strategic approaches to productivity improvement could be combined to give a third approach. While the two ways are contradictory to each other and should not be applied simultaneously, if applied successively they could be very effective. Kaizen could assist in eliminating evident waste and inefficiency before an organization undertakes a project for dramatic strategic improvement.

Learning from best practices through benchmarking

One of the best ways to improve company competitiveness and productivity is through benchmarking – studying how world-class companies operate. Productivity consultants should be aware of this important and popular method, which involves not only examining performance results but also understanding what lies behind them. Companies’ success may be based on optimal staffing structure, use of new technology, organizational design, ability to network, or many other things. But often the essence of their strategy is to bring all these elements together, forming combinations that change continuously, while at the same time pursuing innovation.

Benchmarking is a continuous process of assessing products and services against the toughest competitors or the companies recognized as industry leaders. It is a process of identifying and understanding outstanding practices in organizations anywhere in the world and adapting them to help in improving your company performance. It requires being humble enough to admit that others are better at something, and wise enough to try to learn how to match and even surpass them. Benchmarking can be applied in many areas, the most important of which are strategy, products, processes and competence. Benchmarking provides information needed to focus and support improvements, and develop a competitive advantage. In productivity analysis, benchmarking helps to identify specific activities and practices that ought to be changed. A good example of benchmarking is given in figure 20.5, which illustrates Nokia’s corporate fitness ratings in comparison with other computer and electronics companies.

Kari Tuominen provides an interesting and practical benchmarking model,7 which is described briefly in box 20.2.

451