Image_slides / part4_pca

.pdfDimensionality Reduction

December 7, 2012

1/36

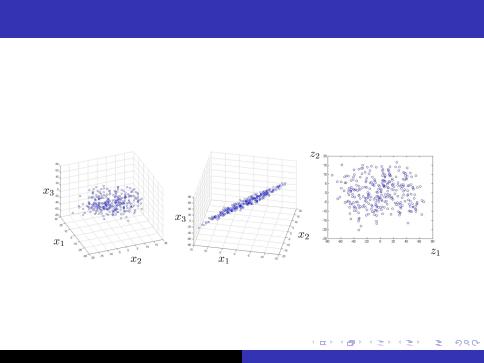

Objective

Reduce data from 3D to 2D

2/36

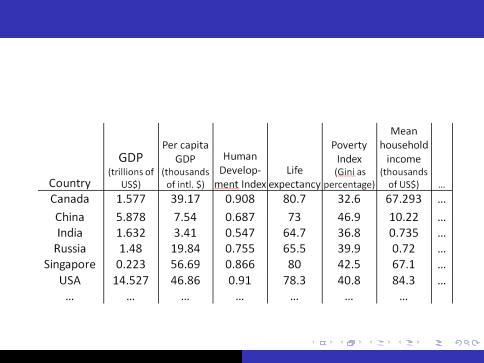

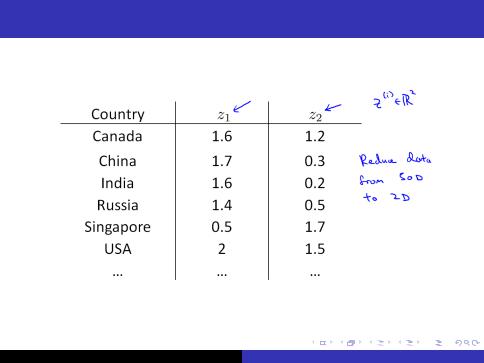

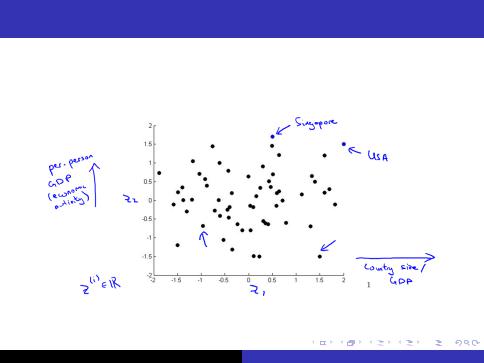

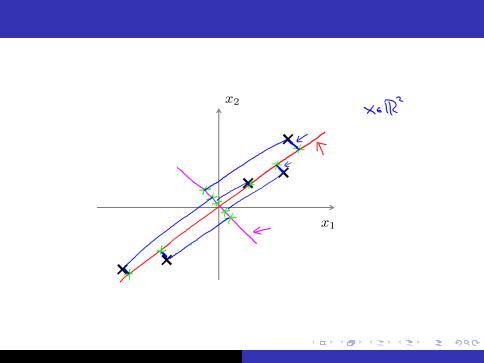

Motivating Example

3/36

Motivating Example

4/36

Motivating Example

5/36

Principal Component Analysis (PCA) problem formulation

6/36

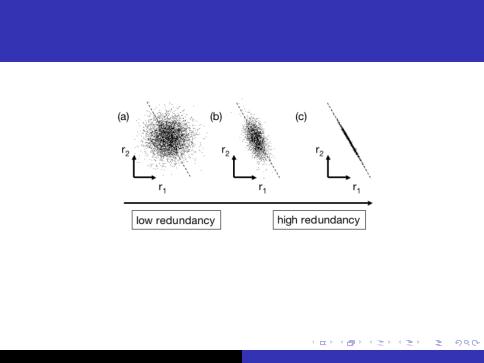

Principal Component Analysis (PCA) statistical problem formulation

1;1 |

0 |

|

I Covariation matrix for (a) 0 |

2;2 |

|

1;1 |

1;2 |

|

I Covariation matrix for (c) 2;1 |

2;2 |

7/36

Covariance

01

|

|

j |

|

|

j |

|

j |

|

X = x1 x2 |

|

xn |

|

|||||

|

|

j |

|

|

j |

|

j |

|

Let each x |

|

|

|

mean |

||||

@ |

1 |

|

i |

has zero |

|

A |

||

i;j = |

|

xiT xj |

|

|

|

|||

n 1 |

|

|

|

|||||

|

|

|

|

|

|

|

||

Ii = j - variance

Ii <> j - covariance

Iif i;j = 0 then xi and xj tottaly uncorrelated

SX = n 1 1 X T X - covariance matrix

8/36

Change of Basis

ILet P be the n n matrix. And each row is basis vector of new subspace

PX = |

0 |

p2 |

1 |

|

xj1 xj2 |

|

xjm |

|

|

|

|

p1 |

|

0 j |

|

|

|

1 |

|

|

B |

|

C |

j |

|

j |

|||

|

B |

pn |

C@ |

|

|

A |

|||

|

@ |

|

A |

|

|

|

|

|

|

where each jjpi jj = 1

IEach product pi xj - is the length of progection of each xj onto vector pi

IIn other words each product pi xj is the coordinate on axis pi

9/36

Desired Covariance Properties

IWe would like to nd matrix P such that the covariances between transformed feature vectors to be zero.

Sy = n 1 1Y T Y , where Y = PX

IIn this case we eliminate all redundancy.

IThe rows of matrix P are the principal components

10/36