6. NATURAL GAS

demand growth for gas in the transport sector. The ten-year development plan of Estonia’s transmission system operator (TSO), Elering1, projects overall gas demand to decline to 0.47 bcm by 2027 (Competition Authority, 2018).

Trade

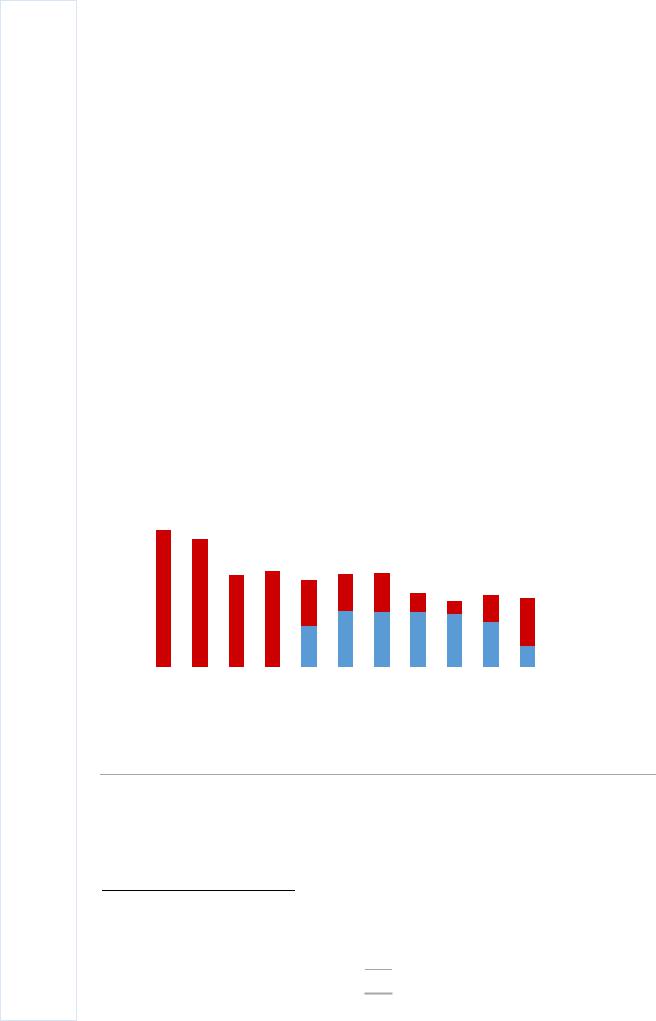

In 2017, Estonia’s total gas imports were 0.49 bcm (Figure 6.3). In line with the declining gas demand in the country, the volume of gas imports has fallen by 51% over the last decade.

Prior to 2014, only gas imports of Russian origin were possible, either directly imported from Russia or from the Inčukalns gas storage facility in Latvia. Estonia’s connection with the Klaipeda LNG terminal in Lithuania, commissioned in 2014, has made it possible for Estonia to develop more diversified import sources. However, gas from Lithuania is purchased on the gas exchange GET Baltic, and as deliveries from this exchange come either from Klaipeda LNG or from Russian gas delivered to Lithuania, gas imports via this route do not necessarily indicate diversification from Russian gas. Thus, while 31% of Estonia’s 2017 gas imports came through the connection with Latvia, including 12% from Lithuania, the predominant share of Estonia’s gas imports are still of Russian origin (Competition Authority, 2018).

Figure 6.3 Estonia’s natural gas imports by entry point, 2007-17

1.2 |

bcm |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Latvia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

0.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

0.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Russian |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

|

|

|

|||||||||||||||||||||||

IEA 2019. All rights reserved.

Estonia’s gas imports are predominately of Russian origin, either imported directly or through the interconnection with Latvia.

Source: IEA (2019b), Natural Gas Information 2019, www.iea.org/statistics.

Production of biomethane

Estonia has no domestic production of natural gas. However, the government has been supporting indigenous production of biomethane to promote both the security of natural

1 Annex A provides more detailed information about institutions and organisations with responsibilities related to the energy sector.

84