10. NATURAL GAS

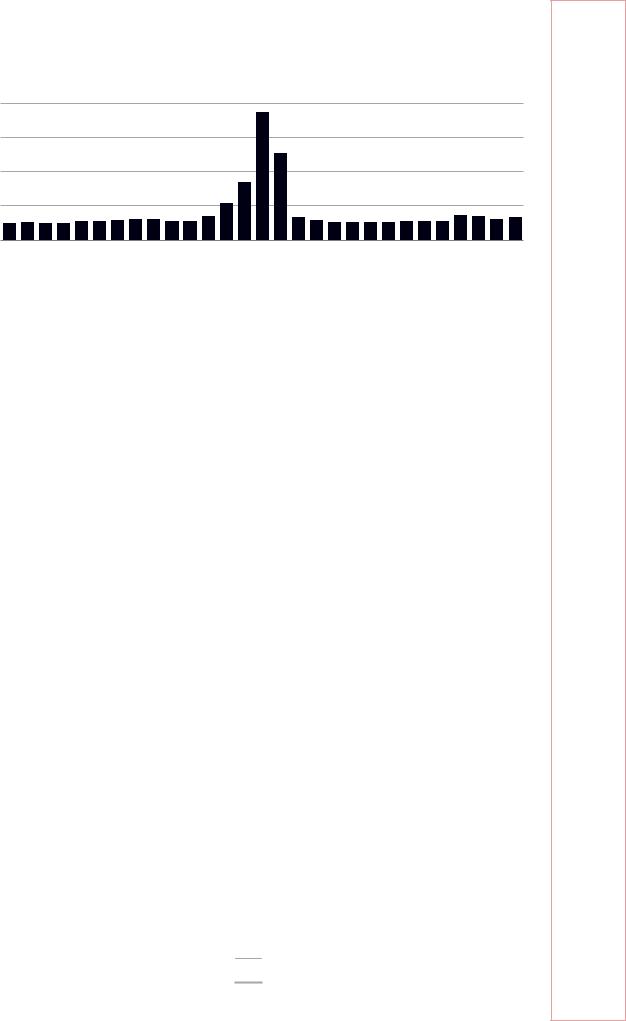

Figure 10.11 UK system average price (SAP), 15 February to 15 March 2018

Pence/therm

400

300

200

100

0 Feb15 Feb16 Feb17 Feb18 Feb19 Feb20 Feb21 Feb22 Feb23 Feb24 Feb25 Feb26 Feb27 Feb28 Mar01 Mar02 Mar03 Mar04 Mar05 Mar06 Mar07 Mar08 Mar09 Mar10 Mar11 Mar12 Mar13 Mar14 Mar15

Source: NGG (National Grid Gas) (2018a), Transmission Operational Data, NG, Warwick, www.nationalgridgas.com/data-and-operations/transmission-operational-data.

On the demand side:

Exports to Ireland were cut from 33.7 mcm on 28 February to 11.8 mcm on 1 March 2018.

The power sector diminished its gas burn from 58 Mm3 on 27 February to 38 Mm3 on 1 March 2018, with gas further losing its price competitiveness vis-à-vis other supply sources. Coal power generation increased to 25% of the system supply. Electricity imports increased by over 60% between 28 February and 3 March 2018 as electricity prices soared to reach a 10-year high.

Flows to industrial gas consumers decreased by around 2 mcm/d between 27 February and 1 March 2018. NG scaled back the off-peak exit capacity on the day, exercising a right included in the industrial users’ commercial contracts for capacity allocation.

The supply side reacted quickly as well:

Flows from the European continent through the BBL and the IUK interconnector pipelines rose by 150% from 32 Mm3 on 28 February to 80.3 Mm3 on 1 March 2018.

Norwegian deliveries to Easington through Langeled rose by ~20%, from 63 Mm3 on 28 February to 75 Mm3 on 1 March 2018.

Rough storage added 5 Mm3 to the market on 2 March 2018 (produced from cushion gas).

Simultaneously, weather conditions also started to improve, as shown by the CWW rising from -4 on 1 March to +4 on 5 March 2018. Heating demand fell and prices returned to typical seasonal levels.

Interlinkages of the gas and electricity systems

During the “Beast from the East” significant wind and coal-fired generation was able to support the high heating and power demand. This favourable outcome in 2018 may not be replicated in the future. Planned coal and nuclear closures, and cold but less windy weather, could diminish the power system’s support in a future event. The question arises as to the level of gas price and power system flexibility (interconnections and

197

ENERGY SECURITY

IEA. All rights reserved.