10. NATURAL GAS

functioning and all the CMA recommendations implemented. The Domestic Gas & Electricity (Tariff Cap) Bill received Royal Assent on 19 July 2018. The aim of the new legislation is to cap temporarily the energy prices for gas (or electricity) customers on standard variable and default tariffs. As recommended by the CMA, on 1 April 2017 Ofgem introduced the temporary cap for customers on prepayment meters, and is required to review the level of the cap at least every six months to ensure the level takes account of external factors, such as wholesale energy costs. The cap expires at the end of 2020, with one-year extensions possible until the end of 2023.

Security of gas supply

Legal framework

In GB, several bodies are in charge of security of gas supply, in line with EU and national laws and regulations. Although the GB gas market is the principle mechanism to guarantee security of supply, the government continuously reviews and monitors the security of gas supply.

BEIS is responsible for energy and climate change policy in the United Kingdom. BEIS leads the international engagement with key energy suppliers and monitors gas security. As the competent authority under the EU Gas Security Regulation (EU 2017/193), BEIS regularly prepares a risk assessment, preventive action plan, and emergency plan.

Ofgem is the independent regulator responsible for consumer protection, security of supply, supervising the gas market functioning, and assessing competition. Every year BEIS and Ofgem prepare the joint statutory security of supply report, which is delivered to parliament.

National Grid Gas (NGG), since 2019, National Grid System Operator (NGSO), has the responsibilities to maintain the balance of supply and demand on a daily basis, adequacy during peak demand periods, provide gas demand forecasts to market participants and plan the network in the ten-year horizon through the so-called annual ten year gas statement. In the short term, the UK gas market is incentivised to be in balance, thanks to imbalance charges imposed by NGSO on shippers who are not in balance at the end of the gas day (cash-out payments).

Adequacy of gas supply and demand

Over the next few years, the IEA expects a slight increase in the reliance on imports over the current level for Great Britain (IEA, 2018c). Production from the North Sea, which had increased in recent years, is expected to fall by around 8 bcm by 2023. On the demand side, there is little opportunity for natural gas demand to grow: coal generation is already at low levels thanks to the introduction of the CPF, and renewable generation continues to grow apace while electricity demand does not. The electricity CM mechanism is bringing forward a combination of new gas-fired plants, gas engines, demand response, and other smaller-scale options. Even the gas engines are expected to operate with relatively low capacity factors. Programmes to encourage consumers to use heat pumps will limit the expansion of natural gas consumption in the residential sector. Therefore, the IEA expects gas demand to fall about 5% (4 bcm) by 2023 (IEA, 2018c). This implies an increase of imports of around 4 bcm, which can be met by either pipeline or LNG.

193

ENERGY SECURITY

IEA. All rights reserved.

10. NATURAL GAS

Towards 2030, NG expects the annual gas demand to decline. In the NG UK future energy scenario report (NG, 2017), annual gas demand declines in all scenarios, but the actual decline will be determined by the pace of the deployment of distributed renewable energies and decarbonisation policies for heating and for the heat and power sector.

Short-term security and emergency response

Under the EU Gas Security of Supply Regulation, NGSO has to ensure the security of gas supply over a 1-in-20 peak gas demand scenario in the case of the loss of the largest infrastructure (N-1 rule).

In the 2018/19 Winter Outlook (NGSO, 2018), NGSO indicates that excepted peak demand could rise slightly above the historic peak demand, but that any loss of the largest infrastructure (81 million cubic metres per day [mcm/d]) could be covered thanks to a 575 mcm/d peak supply, which leaves a margin of 103 mcm/d.

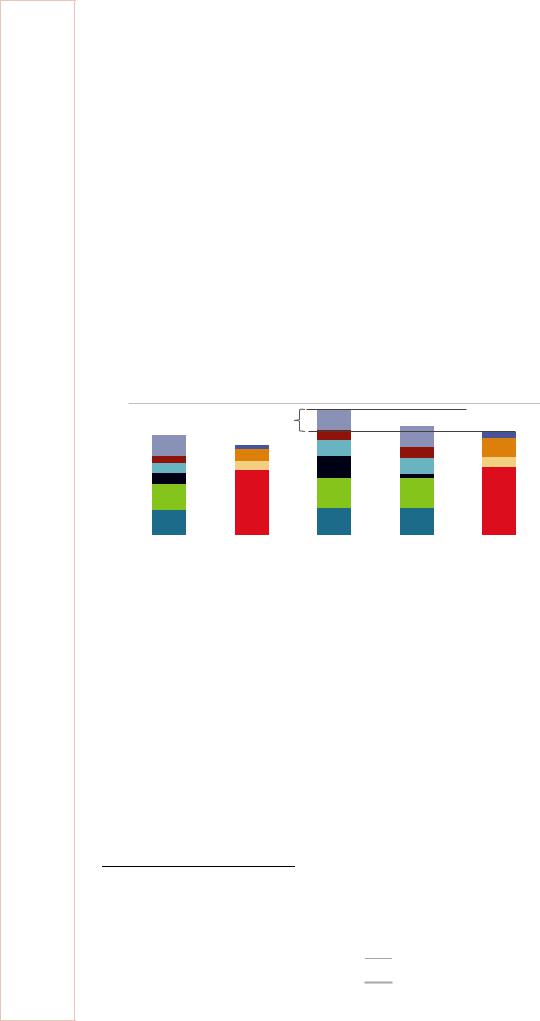

Figure 10.9 Gas supply and demand on a cold day and on a 1-in-20 peak gas day

700 |

Gas flow (mcm / day) |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

UKCS |

|

|

|

|

|

|

Peak supply |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Norway |

|

600 |

|

|

|

|

|

575 mcm/d |

|

Peak demand |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

Margin 103 mcm |

|

|

|

LNG |

|||

500 |

|

|

|

|

472 mcm/d |

|

|

IUK |

|||

452 mcm/d |

407 mcm/d |

|

|

|

|

||||||

400 |

|

|

|

|

|

|

|

BBL |

|||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

Storage |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

300 |

|

|

|

|

|

|

|

|

|

|

NDM |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||

200 |

|

|

|

|

|

|

|

|

|

|

DM exc. generation |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Electricity generation |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

Ireland |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

0 |

|

|

|

|

|

|

Cold day supply |

Cold day demand |

Peak supply |

Peak supply |

Peak demand |

||

|

||||||

|

|

|

|

(largest loss) |

|

Notes: NDM = non-daily metered; DM = daily metered

Source: NGSO (2018), Winter Outlook 2018/19.

Supply-side measures

The United Kingdom has significantly greater natural gas import potential than it currently utilises. Studies carried out by NGSO estimate that the range of supply diversity available to the UK markets (including storage) can deliver 103 mcm/d above the 1-in-20 year1 maximum daily demand of 472 mcm/d, with a peak supply deliverability of 575 mcm/d. The United Kingdom has a programme to maximise the economic recovery of indigenous resources, with the MER strategy of the OGA. The United Kingdom relies on a flexible short-range storage as well as three large LNG import facilities. Seasonal storage is no longer available with the closure of Rough storage, which leaves the GB market with a significantly lower storage capacity.

1 1-in-20 years peak daily demand is the level of daily demand that, in a long series of winters and with the connected load held at the levels appropriate to the winter in question, would be exceeded in one out of 20 winters, with each winter counted only once.

194

IEA. All rights reserved.

10. NATURAL GAS

Demand-side measures

The Significant Code Review by Ofgem found the gas market could benefit from a demand-side mechanism to enable large consumers of gas to reduce their demand to avoid an emergency. Ofgem approved the proposed centralised demand-side response (DSR) mechanism for large consumers by NG in October 2016.

Gas quality

Depending on the import origin, the quality of imported gas varies from the high Wobbe index of Norwegian gas to Dutch gas with a low Wobbe index. As domestic production has been in decline, the gas quality and internal gas transmission capacity have been identified as challenges. As the United Kingdom’s reliance on LNG and pipeline imports is set to increase, gas specifications will be a critical element for import flexibility. The latest specifications stem from 1996 when the Health and Safety Executive issued the Gas Safety (Management) Regulations 1996 for National Grid. The United Kingdom may be disadvantaged when procuring LNG on the international market because of the narrow gas specifications compared to those of other European countries (Jackson et al., 2005).

Recent supply disruptions

Regional gas market events during winter

A controlled shutdown of the Forties Pipeline System on 11 December 2017 resulted in the curtailment of about 40 mcm/d of gas that flowed from the St Fergus Gas Terminal – equivalent to around 12% of the national daily demand on a winter day. Other sources – notably from continental Europe – met this deficit until the pipeline returned to full operation on 30 December 2017. To manage the increased flows from Europe (from Belgium and the Netherlands), NGG temporarily reduced flows through the Bacton gas terminal to bring another compressor unit online. This routine process was completed by the end of the day, and allowed both interconnectors to import into the United Kingdom at near capacity.

Also, on 12 December 2017 there was an explosion at a gas pipeline hub in Baumgarten, Austria, as a result of a technical fault. Although there were no gas security-of-supply concerns for GB, transit through Austria to Southern Europe was impacted, which resulted in short-term price increases across Western Europe and, most notably, the declaration of a gas emergency in Italy. The Baumgarten hub returned to full operations by 13 December 2017. Italy drew on alternative interconnector flows, plus storage facilities, and weathered their emergency with no impact on supplies to consumers.

Despite these coincident events, at no time was Great Britain gas security threatened. NG were confident that supplies remained adequate throughout the period. In some ways, the events served as a test of the strength and flexibility of the gas supply system and market. Although security was not threatened, there was some impact on prices. UK wholesale day-ahead gas prices spiked (moderately) on 12 December 2017, but quickly fell to close at 67.3 pence/therm (compared to 57.7 pence/therm in the preceding week, when average temperatures were higher).

195

ENERGY SECURITY

IEA. All rights reserved.

10. NATURAL GAS

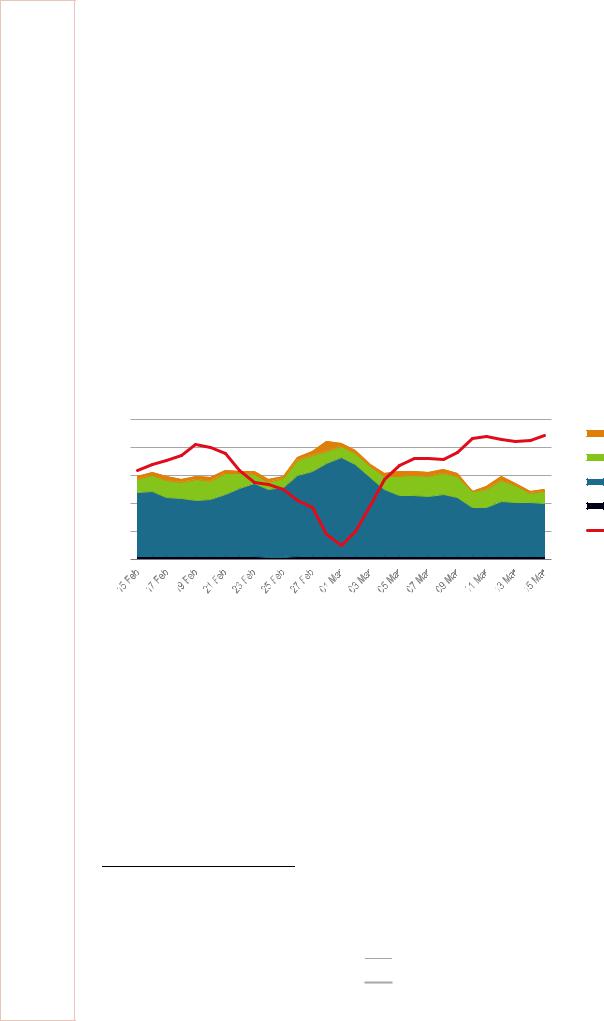

Cold spell during February 2018 – The “Beast from the East”

Starting on 24 February 2018 and ending on 4 March 2018, the United Kingdom and Ireland suffered a cold wave, the named “Beast from The East”, responsible for unseasonable low temperatures and heavy snowfall. According to NGG 1 March 2018 was the seventh coldest day in their 58-year weather record history and triggered the highest gas demand in seven years. However, the highest gas demand on record of 465 mcm/d (January 2010) also included exports via the IUK interconnector, which was flowing at full capacity. Once exports to the Republic of Ireland are accounted for, it is possible that 1 March 2018 is the highest domestic demand on record.

On 1 March 2018, NGG issued a gas deficit warning, which indicates that additional network balancing measures were potentially required on that day. This was in combination with a series of flow reductions that affected Norwegian assets, storage, LNG terminals, and UKCS production. As shown in Figure 10.10, demand from the distribution network (serving primarily households and commercial entities) rose the most significantly by over 100 mcm/d from 243 mcm on 24 February 2018 to 357 mcm on 1 March 2018 as the composite weather variable2 (CWW) dropped to -4.44.

Figure 10.10 UK gas demand, 15 February to 15 March 2018

mcm

500

400

300

200

100

0

Note: LDZ = local distribution zone. CWV = composite weather variable Source: IEA (2018d), Gas 2018, based on data from NG.

CWV |

9 |

|

|

Exports |

|

|

6 |

|

|

Power |

|

|

|

|

|

3 |

LDZ |

|

|

|

|

0 |

Industrial |

|

-3 |

CWV |

|

-6 |

|

To meet the rapidly climbing natural gas demand was challenged by the fact that the severe weather conditions caused a number of outages on some of the key supply infrastructure, which resulted in reduced flows from the Netherlands and from North Sea production, and further tightened the market. The gas system, already under stressed conditions, then suffered a further blow due to the unavailability of the regasification unit at the South Hook LNG terminal early in the morning of 1 March 2018. Soon after, NGG issued a gas deficit warning at 05:47 with the supply deficit estimated to be around 45 mcm. This was the first gas deficit warning issued since the winter storms of 2010. As a result of the tight market situation, gas prices in the United Kingdom soared on 1 March 2018 to a 20-year high, above 370 pence/therm (127 GBP/MWh, see Figure 10.11)3. The market reacted by optimising both the demand and the supply side.

2The CWV is a single measure of daily weather and is a function of actual temperature, wind speed, effective temperature, and seasonal normal effective temperature (Gasgovernance, 2014).

3The SAP reported by NG stood at 372 pence/therm.

196

IEA. All rights reserved.