4. RENEWABLE ENERGY

Heat from renewable energy

The government has put a strong focus on renewable heat policy under the EU RED and the ambitious long-term GHG emission targets under the 2008 Climate Change Act.

Part of this effort has been a more strategic approach, with the publication of a heat strategy in 2012 and an updated strategic document in 2013 (UK Government, 2013). Key aspects of this strategy focused on buildings and industrial heat decarbonisation and the role of heat networks. Subsequently, the government set up a Heat Networks Delivery Unit, made some funding available for district heating networks, and developed a set of industrial carbon reduction and energy efficiency roadmaps.

In the 2017 Clean Growth Strategy, the government set out plans to phase out, during the 2020s, the installation of high-carbon fossil fuel heating in new and existing homes currently not connected to the gas grid, and to invest in low-carbon heating by reforming the RHI, spending GBP 4.5 billion to support innovative low-carbon heat technologies in homes and businesses between 2016 and 2021.

Renewable Heat Incentive

The principal mechanism to support renewable heat in Great Britain is the RHI, which was established in 2011 for non-residential entities (businesses [including industry], public sector, and non-profit organisations) and in 2014 for residential users. A precursor programme, the Renewable Heat Premium Payment scheme, ran from 2011 to 2014. This provided around 16 000 grants to support investment in renewable heat technologies by households, social housing landlords, and community groups. A similar to the RHI scheme started in 2012 in Northern Ireland and closed to new applications in 2016. The GB scheme is expected to remain open until March 2021, subject to budget availability.

The RHI supports renewable heat technologies such as biomass, biomass cogeneration, biomethane injection to the gas grid, biogas, heat pumps, solar thermal, and geothermal. Owners of eligible plants apply to Ofgem after commissioning the installation and receive quarterly payments for either seven years (residential) or 20 years (nonresidential). Payments are based on the metered heat output or, in most domestic cases, on the estimated heat demand. RHI payments come from public (taxpayer) funds.

The deployment of renewable heat installations and the generation of renewable heat are monitored by Ofgem and BEIS and published on a monthly basis (UK Government, 2018a, for monthly updates see www.gov.uk/government/collections/renewable-heat- incentive-statistics.) As of mid-2018, there are over 18 000 non-domestic installations and over 63 000 domestic installations accredited to the RHI schemes (Table 4.1), compared to over 20 million gas boilers in the current housing stock (UK Government, 2018i).

Table 4.1 Key RHI statistics (data to end of August 2018)

|

Non-residential scheme |

Residential scheme |

Number of applications |

19 788 |

69 536 |

|

|

|

Number of accredited installations |

18 821 |

63 559 |

|

|

|

65

ENERGY SYSTEM TRANSFORMATION

IEA. All rights reserved.

4. RENEWABLE ENERGY

|

Non-residential scheme |

Residential scheme |

|

Number of installations in payment |

18 215 |

65 661 |

|

|

|

|

|

Installed capacity (MWth) of accredited |

4 210 |

817 |

|

installations |

|

|

|

|

|

|

|

Heat generated and paid for (GWh) |

26 404 (since November 2011) |

2 942 (since April 2014) |

|

|

|

|

|

Key technologies |

Biomass boilers (71% of heat |

Biomass boilers (52% of heat |

|

|

generated and paid for), |

generated), ASHPs |

(31%), |

|

biomethane (22%) |

GSHPs (16%), solar |

thermal |

|

|

(2%) |

|

Key sectors |

Agriculture (28%) |

Rural (80%) |

|

|

Accommodation/B&B (30%) |

|

|

Note: GSHP = ground source heat pump.

Source: UK Government (2018a), RHI Deployment Data, BIS, www.gov.uk/government/collections/renewable-heat- incentive-statistics accessed on 30 September 2018.

Box 4.2 Industrial aspects of renewable energy policy

The sustained support for renewable energy has reinforced supply chains across the renewables sector, particularly offshore wind. The United Kingdom is now among the world’s largest markets for offshore wind, with 13 700 people employed in the sector (7 900 direct jobs and 5 800 indirect). This has led offshore wind suppliers into United Kingdom-based manufacturing, which creates jobs and brings investment into the economy. The Siemens blade facility in Hull is just one example of this success. Indeed, there has been strong progress in attracting investment and promoting rejuvenation in areas such as Hull, Grimsby, Barrow-in-Furness, Great Yarmouth, Campbeltown, and Lowestoft through the development of a UK supply chain.

Moreover, the government’s ambition (outlined in its manifesto) to have a strong, industrialised UK supply chain is increasing its capacity to win export orders. An Offshore Wind Industry Council (OWIC) was set up to develop an ambitious business-led proposal for an offshore wind sector deal.

As a result of these initiatives, the domestic content of UK wind farms increased from 43% in 2015 to 48% in 2017. This means the offshore wind industry has almost hit its long-term target, set out by the OWIC, to source 50% of its work in Britain. The United Kingdom also has a strong track record in the supply of offshore wind development services, engineering design, and the supply of interarray cables and offshore substations. Approximately 75% of the value of operations and maintenance contracts for UK offshore wind farms are won by UK businesses.

In March 2019, the UK government concluded an Offshore Wind Sector Deal with the industry to boost economic growth and job opportunities in the UK. Based on the commitment from the government in 2018 to run regular Contracts for Difference auctions with a total funding of GBP 557 million, which would build up to 30 GW of offshore wind capacity, subject to costs coming down. Under the deal the industry is committed to invest GBP 250 million Offshore Wind Growth Partnership (OWGP) and the government expects the sector to continue cutting costs to lower their impact on bill payers while investing in and driving growth in the UK’s manufacturing base with UK content raised to 60% by 2030 (UK Government, 2019a).

66

IEA. All rights reserved.

4. RENEWABLE ENERGY

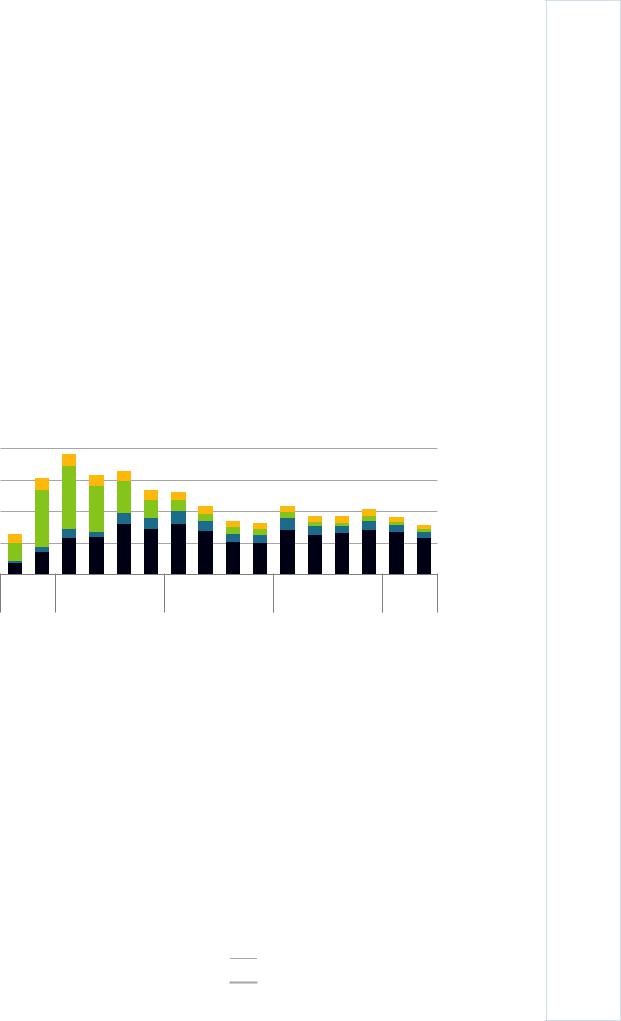

RHI spending has been consistently below budget and, furthermore, there was a slowdown of RHI accreditations after a reduction in the biomass tariffs (20% for the domestic tariff and 15% for small commercial installations) from April 2015. This resulted in a sharp decrease in the deployment of biomass boilers under the scheme, without a corresponding increase from other technologies. Non-residential installations saw a reduction of 23% (by capacity of accredited installations) from 2015 to 2016, and the number of residential installations fell even more dramatically. Subsequent to further tariff revisions from January 2017, deployment increased, especially for ASHPs whose tariffs were increased by 25%, but in 2018 the deployment dropped again, especially in the second quarter (Figure 4.7).

Overall, the results have been mixed. According to an assessment commissioned by the UK House of Commons’ Public Accounts Committee and published in May 2018, “the RHI has failed to meet its objectives or provide value for money for the GBP 23 billion expected total cost to taxpayers” (Public Accounts Committee, 2018). The report highlights that some RHI-funded installations may contribute to air pollution and BEIS and Ofgem could do more to monitor this impact by working with local government across GB. According to the report, there are also cases of fraud and non-compliance with the RHI application requirements.

Figure 4.7 Domestic RHI-accredited installations by technology, Q3 2014 - Q2 2018

Number of installations

4 000

Solar thermal

Solar thermal

3 000

Biomass

Biomass

2 000

GSHP

GSHP

1 000

ASHP

ASHP

0

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

2014 |

|

2015 |

|

|

2016 |

|

|

2017 |

|

2018 |

|||||

Notes: Excludes so-called legacy systems that were installed after the announcement of the plans to introduce the RHI and the actual launch of the domestic RHI.

Source: UK Government (2018a), RHI Deployment Data: August 2018, BEIS, accessed on 30 September 2018. www.gov.uk/government/collections/renewable-heat-incentive-statistics#monthly-deployment-data

The National Audit Office found the government had sufficiently adapted the scheme to new planning targets and controlled the scheme’s costs (to avoid the budget control problems that occurred on a similar scheme in Northern Ireland) (NAO, 2018). BEIS also conducted research into the RHI outcomes in general terms. Ofgem estimates rather low overpayments as a result of non-compliance with the scheme’s rules at 4.4% and 2.5% of the total scheme expenditure in 2016/17 (on the non-residential and residential RHI schemes, respectively).

Following the report, BEIS introduced legislative reforms to the RHI that tighten the scheme regulations to guard against non-compliance and manipulation of the scheme’s rules (UK Government, 2018f). In addition, BEIS and Ofgem put in place a new strategy to reduce the amount of fraudulent activity, quantify non-compliance, and establish the root causes of fraud and error across all the environmental and social schemes that Ofgem delivers on behalf of the government. These measures improved BEIS’ and

67

ENERGY SYSTEM TRANSFORMATION

IEA. All rights reserved.

4. RENEWABLE ENERGY

Ofgem’s ability to identify and tackle RHI gaming and non-compliance, and both organisations will continue to monitor this area to ensure taxpayers’ money is protected.

The RHI has its budget confirmed until April 2021. BEIS is developing its future policy framework to support low-carbon heating. It has commissioned an evaluation to understand consumer behaviours further, as well as the market and supply chain for renewable heating systems. This evaluation is expected to provide evidence on consumer-perceived access to renewable fuels as well as an understanding as to factors that influence consumer decisions to install renewable heating systems. A final report is expected in mid-2021, along with several interim reports.

A call for evidence on the future framework for heat in buildings was published in March 2018 (UK Government, 2018g). This sought views and evidence on actions the government could take during the 2020s to phase out high-carbon fossil fuel heating in off gas grid buildings, as a first step to developing a post-RHI policy.

Contrary to renewables-based electricity, which is financed by consumers through their energy bills, renewable heating is supported from the state budget (by taxpayers).

Table 4.2 shows the RHI budget and commitments made.

Table 4.2 RHI budget and committed spend (GBP million)

Year |

2016/17 |

2017/18 |

2018/19 |

2019/20 |

2020/21 |

Planned budget |

640 |

780 |

900 |

1010 |

1150 |

|

|

|

|

|

|

|

|

Committed spend |

|

|

|

Non-domestic RHI |

441 |

612 |

720 |

779 |

812 |

Domestic RHI |

92 |

106 |

117 |

122 |

125 |

Total |

533 |

719 |

838 |

901 |

937 |

Source: BEIS (2018b), UK Submission to the IEA for the 2018 in-depth review. Data to end of September 2018.

Heat Networks Investment Project

In parallel to the RHI, the government committed funding for district heating networks, which supplied around 2% of the United Kingdom’s heat in 2017. The GBP 320 million Heat Networks Investment Project (HNIP) capital investment programme is expected to support up to 200 projects by 2021 through grants and loans and other mechanisms. Funding can go to projects that use a minimum of 50% renewable or waste heat, or alternatively 75% co-generated heat. Potentially, the networks could therefore still be fully supplied by fossil fuels.

A first pilot round of funding of GBP 24 million ran from October 2016 to March 2017 and supported nine district heating projects – including five gas-fired co-generation plants, one gas boiler, one gas and biomass-fired co-generation plant, and one heat pump3 – that will deliver heat to 5 000 homes and 50 non-domestic buildings. Applications were limited to local authorities and other public sector bodies during the pilot phase. It is expected that these nine networks will supply around 85 000 MWh of heat per year, which would result in savings of 216 324 tonnes of carbon dioxide (tCO2) over the next 15 years. Following this pilot, the main funding round is expected to open at the end of 2018, with first year funding to be allocated by March 2019. The government plans to

3 The Sheffield District Energy Network project (energy from waste) will not go ahead.

68

IEA. All rights reserved.