China Power System Transformation |

Policy, market and regulatory frameworks for power system transformation |

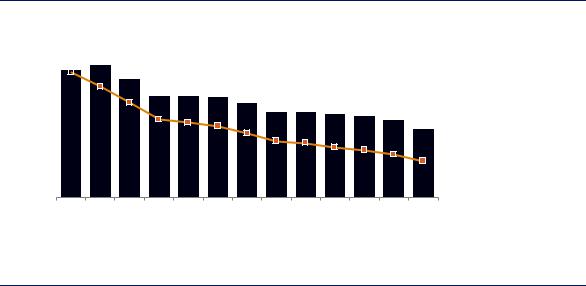

Figure 25. Installed generation capacity under legacy contracts and share of demand, 2017-29

45 |

GW |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

120% |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

100% |

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

80% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

60% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

0% |

|||||||||||||

|

|

||||||||||||||||||||||||||

Contracted

Contracted

capacity

Share of maximum demand

Share of maximum demand

Gradual phasing out of legacy contracts is expected to ensure a smooth transition to a competitive market without compromising security of supply.

Transition from the private-party regime (self-supply)

Under the restrictive legal framework prior to reform, private parties were allowed to produce energy for self-supply, either at their premises or at remote points, using the CFE transmission grid. Consumers under self-supply and co-generation agreements (that included both load and generation) prior to the new Electricity Industry Act were respected under the reform. In this case the law defined a transition model to allow these generators and consumers to transition, if they found it profitable, to the new regime.

Under the previous regime these societies were able to inject at one point of the grid and withdraw at another, upon the completion of investment in grid reinforcements, paid for by self-suppliers. This restrictive regime created incentives for a very inefficient operational scheme, since self-supply societies were not able to sell energy to CFE (or on the wholesale market after the reform) when they had surplus cheap capacity, or to buy from CFE (or from the wholesale market) when their capacity was more expensive.

The Electricity Industry Act provides incentives for these societies to leave this regime and incorporate into the wholesale market, providing financial transmission rights that hedge the risk due to their location. Leaving their old regime allows these societies to sell and buy electricity in the wholesale market when this is economic.

Treatment of “stranded costs” in the United States

The United States is another example of a country that has had to consider a transitional mechanism in the process of opening the market. As part of its activities to promote wholesale power competition, in 1997 FERC issued Order 888 to explicitly implement the principles to be followed in the open-access system, recognising that there could be transition costs. These costs were labelled “stranded costs”, and were used to identify “capital investments that are unrecoverable because of the transition to competition”.

In the US case, the risks faced by utilities in jurisdictions being opened to competition came from previous commitments made to satisfy expected demand, and the prospect that exiting clients would reduce the revenue base that the utilities relied on to pay for these commitments.

Page | 129

IEA. All rights reserved