Is the UK model working?

member of the audit committee provided he was independent when appointed as Chairman.

The current UK principles-based model appears to be having a positive impact on governance practice. However it still has some way to go in meeting the needs of all stakeholders, a primary requirement being the transparency of directors’ activities. So what are the alternatives?

Cross-border harmony

There are different approaches to corporate governance throughout the world, often reflecting the local cultural and economic realities. Should the UK be looking to define and pursue what it considers to be the best approach or should it be working to a common global corporate governance model in order to enable increased global comparability?

The European Corporate Governance Institute (ECGI) is seeking to address the issue of cross-border inconsistencies between governance models within Europe by leading a project: Modernising Company Law and Enhancing Corporate Governance in the European Union.

UK versus US governance environments

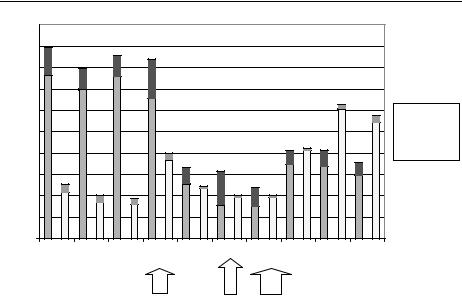

The US practice in the field of corporate governance and risk management is to implement a highly regulated environment. Since the introduction of SOX, there has been a decrease in new listings in the US, with only 354 companies listing in 20065 compared to 856 companies in 1999 (see Figure 11.1).

This is in stark contrast to the UK’s practice, now overseen by the Financial Reporting Council (FRC) which, through the Combined Code, promotes the principles-based approach.

It is this lighter touch to regulation which many believe stimulated the significant increase in the total number of flotations (domestic and foreign) on the LSE which increased to 576 companies in 2006 from 187 companies in 1999.6 This is also mirrored in the number of new foreign listings, where we are once again seeing growing confidence in UK markets – thirty-two new foreign listings in 2006.7 This no doubt reflects the liquidity of the UK market (there was a notable decrease in total UK listings from 2000 to 2003). However, the revision of the UK’s Combined Code in 2003, at the same time as an apparent market reaction against what is seen as the prohibitively expensive cost of complying with SOX, has turned the spotlight on the issue of principles-based regulation versus prescriptive rules. Recent announcements from the SEC and

5From World Federation of Exchanges, www.world-exchanges.org.

6From World Federation of Exchanges, www.world-exchanges.org.

7From World Federation of Exchanges, www.world-exchanges.org.

225

Simon Lowe

|

1000 |

|

|

|

|

|

|

|

|

|

|

900 |

|

|

|

|

|

|

|

|

|

|

800 |

|

|

|

|

|

|

|

|

|

listings |

700 |

|

|

|

|

|

|

|

|

|

600 |

|

|

|

|

|

|

|

|

|

|

new |

500 |

|

|

|

|

|

|

|

|

|

of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Number |

400 |

|

|

|

|

|

|

|

|

|

300 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

200 |

|

|

|

|

|

|

|

|

|

|

100 |

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

1997 |

1998 |

1999 |

2000 |

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

Ye ar

UK foreign

UK foreign

UK domestic

UK domestic

US foreign

US foreign

US domestic

US domestic

UK Combined |

|

SOX |

Revised UK Combined Code |

Code issued |

|

issued |

issued |

|

|

|

|

|

|

|

|

Figure 11.1 Comparison of US and UK listings 1997–2006

PCAOB suggest that the US is seeking to soften its stance, but this may be a case of too little too late.

Figure 11.1 shows the number of Initial Public Offerings (IPO) – both domestic and foreign – in the UK and the US from 1997 to 2006, together with the relevant dates when the UK and US corporate governance guidance was issued.8

The decline in US listings is commonly blamed both on the cost and demand SOX places on management resources and also on the reluctance of management, in the heavily litigious environment of the US, to adopt a more riskbased approach to controls assessment. What is reasonable risk to the informed director may not be viewed in the same light by the courts. But other factors are starting to drive a change in governance practice; the competition for new capital is coming from the more loosely regulated emerging markets – China, India, Middle East – not to mention the actual cost of the listing process in the US, where underwriting fees and professional advisory services’ costs are considerably more expensive. Economic consultants Oxera found that the same bank would charge higher fees for a listing in the US than in Europe.9 For

8From World Federation of Exchanges, www.world-exchanges.org.

9The Cost of Capital: An International Comparison, Oxera Consulting and London Stock Exchange, June 2006.

226