Unit three

PRICE AND PRICE SYSTEM IN A MARKET ECONOMY. MARKET EQUILIBRIUM |

Learning objectives

After studying this unit, you should be able to:

define the notion of price, price system, market price, equilibrium, equilibrium price, market equilibrium, excess demand (shortage), excess supply (surplus);

state the role of prices in the market economy;

distinguish between a market price and an equilibrium price, excess demand (shortage) and excess supply (surplus);

outline the key functions of prices such as rationing, signalling, and motivating/incentive.

Starting up

Task 1. Using the expressions from the table given on page 8, comment on the following quotations.

“Anybody can cut prices, but it takes brains to produce a better article.” (P.D. Armour)

“Cheat me in the price, but not in the goods.” (English proverb)

“Quality is remembered long after the price is forgotten.” (Gucci Family Slogan)

TEXT

As you remember a market economy is an economic system in which economic decisions and the pricing of goods and services are guided by the interactions of country's citizens and businesses and there is little government intervention or central planning. Prices are the key ingredients in a market economy because they make things happen. If buyers want to own some items badly, they will pay more for them. When sellers want to sell some items badly, they will lower their prices. Prices play such an important role in economic life that most democracies are often described as price-directed market economies.

The price system lies at the heart of any society. The price system is an economic system where prices are not set by government but by the interaction of supply and demand. Under such a system every commodity and every service has a price, i.e. the amount of money for which a unit of goods or services is sold and bought.

Price for a commodity is a reflection of supply of and demand for this commodity. The theory of supply and demand is the step toward understanding how market prices are determined and the way in which these prices help make production and consumption decisions.

The concepts of supply and demand have been introduced separately but it is time to put the two concepts together. In economic theory, the interaction of supply and demand is known as equilibrium.

One of the functions of markets is to find equilibrium prices that balance the supply of and demand for goods and services. An equilibrium price (also known as a market price) is one at which each producer can sell all he wants to produce and each consumer can buy all he demands. Naturally, producers always would like to charge higher prices. But they are limited by the law of demand. The law of supply puts a similar limit on consumers. They always prefer to pay a lower price than the current one.

At prices above the equilibrium price, the quantity supplied exceeds the quantity demanded, so a surplus or excess supply develops. A shortage or excess demand occurs at prices below the equilibrium price, when the quantity demanded is greater than the quantity supplied.

A decrease in demand leads to a decrease in both the equilibrium price and equilibrium quantity. An increase in supply produces a higher equilibrium quantity but a lower equilibrium price.

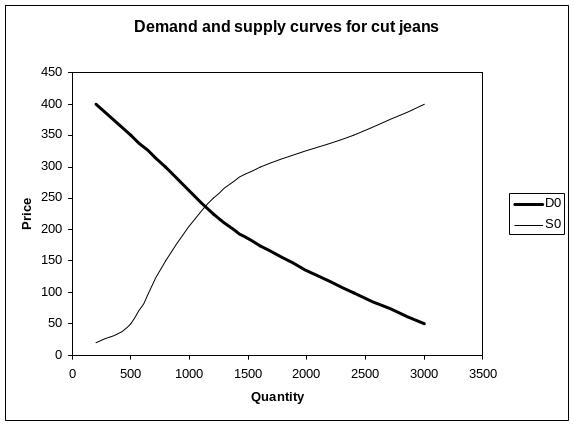

Graphically the situation can be represented by two curves: one showing the price-quantity combinations buyers will pay for, or the demand curve; and one showing the price-quantity combinations suppliers will bring into the market, or the supply curve. The buyers’ and sellers’ willingness and ability to buy and sell balance out the market, where demand and supply are in equilibrium, that is, where the curves intersect.

Demand and supply schedule for cut jeans

The quantity demanded |

Price |

The quantity supplied |

200 |

$400 |

3000 |

500 |

$350 |

2400 |

800 |

$300 |

1600 |

1200 |

$225 |

1200 |

1600 |

$175 |

800 |

2400 |

$100 |

500 |

3000 |

$50 |

200 |

Taking into account all mentioned above economists distinguish three key functions of prices as rationing, signalling, and motivating/incentive.

Rationing function. Since there is not enough of everything to go around* goods and services are allocated, or distributed, based on their price. To put it another way, the more scarce something is, the higher the price will be and the fewer people will want to buy it. Economists describe this as the rationing effect of prices. Prices serve to ration scarce resources when demand in a market outstrips supply. When there is a shortage, the price is bid up – leaving only those with the willingness and ability to pay with the effective demand necessary to purchase the product.

Signalling function. One of the things that prices do is carry information to buyers and sellers. Through their choices consumers send information to producers about the changing nature of needs and wants. Low prices are signals to buyers (consumers), who can now afford to purchase the things they want. When prices are high enough, they send a signal to sellers (producers), who can now earn a profit at the new price.

Motivation/incentive function. Price increases and decreases send messages to suppliers and potential suppliers of goods and services. Price increases attract additional producers. Price decreases drive producers out of the market. Production-motivating function of prices refers to the way prices encourage producers to increase or decrease the level of output.

Acting in accordance with the profit motive, business firms produce what the consumers desire. Producers can earn more revenues by responding to the consumer demand than by ignoring it. Those who sell goods at prices consumers are not willing to pay will suffer financial losses. In that way prices provide the answer to the question of What to produce.

Prices encourage business people to produce their goods at the lowest possible cost. The producers’ desire for profit leads them to introduce new production methods to lower production costs.

Firms that are efficient will produce more goods with fewer raw materials than firms that are inefficient. The quest for greater efficiency motivates producers to succeed in competitive activity. While these efforts are in the best interests of the sellers, all of consumers may benefit because they are provided with the things they want at lower costs. In such a way the price system carries out the task of determining how goods and services are produced.

Under the price system, each person’s income is determined in the market place. Some people are endowed with talent, skill, intelligence, education or special training and earn more, on the average, than those who are not. What the worker can buy with his wage will depend, in turn, upon the prices of the goods and services the worker would like to own. Consumers who are willing and able to pay the equilibrium price (or more) buy a desired product, while those who are unwilling or unable to pay this price have to do without this product. Thus, by assigning values to the work people perform, the price system answers the Who question.