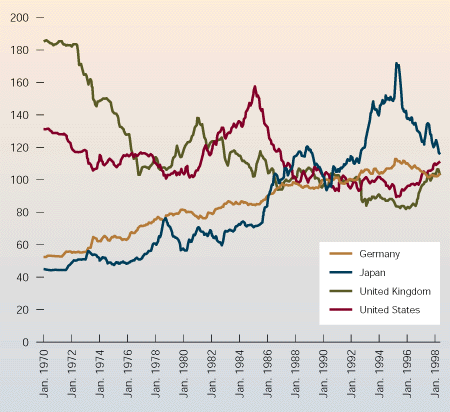

Figure 10.1

Long-Term Exchange Rate Trends

Source: JP Morgan, Effective Exchange Rate Index, 1970 - 98. (1990=100.)

real interest rates attracted foreign investors seeking high returns on financial assets. At the same time, political turmoil in other parts of the world, along with relatively slow economic growth in the developed countries of Europe, helped create the view that the United States was a good place to invest. These inflows of capital increased the demand for dollars in the foreign exchange market, which pushed the value of the dollar upward against other currencies.

The fall in the value of the dollar between 1985 and 1988 was caused by a combination of government intervention and market forces. The rise in the dollar, which priced US goods out of foreign markets and made imports relatively cheap, had contributed to a dismal trade picture. In 1985, the United States posted a record-high trade deficit of over $160 billion. This led to growth in demands for protectionism in the United States. In September 1985, the finance ministers and central bank governors of the so-called Group of Five major industrial countries (Great Britain, France, Japan, Germany, and the United States) met at the Plaza Hotel in New York and reached what was later referred to as the Plaza Accord. They announced that it would be desirable for most major currencies to appreciate vis-à-vis the US dollar and pledged to intervene in the foreign exchange markets, selling dollars, to encourage this objective. The dollar had already begun to weaken in the summer of 1985, and this announcement further accelerated the decline.

The dollar continued to decline until early 1987. The governments of the Group of Five even began to worry that the dollar might decline too far, so the finance ministers of the Group of Five met in Paris in February 1987 and reached a new agreement known as the Louvre Accord. They agreed that exchange rates had been realigned sufficiently and pledged to support the stability of exchange rates around their current levels by intervening in the foreign exchange markets when necessary to buy and sell currency. Although the dollar continued to decline for a few months after the Louvre Accord, the rate of decline slowed, and by early 1988 the decline had ended. Except for a brief speculative flurry around the time of the Persian Gulf War in 1991, the dollar has been relatively stable since then against most major currencies with the notable exception of the Japanese yen.

Thus, we see that in recent history the value of the dollar has been determined by both market forces and government intervention. Under a floating exchange rate regime, market forces have produced a volatile dollar exchange rate. Governments have responded by intervening in the market--buying and selling dollars--in attempting to limit the market's volatility and to correct what they see as overvaluation (in 1985) or potential undervaluation (in 1987) of the dollar. The frequency of government intervention in the foreign exchange markets explains why the current system is often referred to as a managed-float system or a dirty float system.

Fixed Versus Floating Exchange Rates

The breakdown of the Bretton Woods system has not stopped the debate about the relative merits of fixed versus floating exchange rate regimes. Disappointment with the system of floating rates in recent years has led to renewed debate about the merits of fixed exchange rates. In this section we review the arguments for fixed and floating exchange rate regimes.6We will discuss the case for floating rates before discussing why many commentators are disappointed with the experience under floating exchange rates and yearn for a system of fixed rates.

The Case for Floating Exchange Rates

The case for floating exchange rates has two main elements: monetary policy autonomy and automatic trade balance adjustments.

Monetary Policy Autonomy

It is argued that under a fixed system, a country's ability to expand or contract its money supply as it sees fit is limited by the need to maintain exchange rate parity. Monetary expansion can lead to inflation, which puts downward pressure on a fixed exchange rate (as predicted by PPP theory; see Chapter 9). Similarly, monetary contraction requires high interest rates (to reduce the demand for money). Higher interest rates lead to an inflow of money from abroad, which puts upward pressure on a fixed exchange rate. Thus, to maintain exchange rate parity under a fixed system, countries were limited in their ability to use monetary policy to expand or contract their economies.

Advocates of a floating exchange rate regime argue that removal of the obligation to maintain exchange rate parity would restore monetary control to a government. If a government faced with unemployment wanted to increase its money supply to stimulate domestic demand and reduce unemployment, it could do so unencumbered by the need to maintain its exchange rate. While monetary expansion might lead to inflation, this would lead to a depreciation in the country's currency. If PPP theory is correct, the resulting currency depreciation on the foreign exchange markets should offset the effects of inflation. Although under a floating exchange rate regime domestic inflation would have an impact on the exchange rate, it should have no impact on businesses' international cost competitiveness due to exchange rate depreciation. The rise in domestic costs should be exactly offset by the fall in the value of the country's currency on the foreign exchange markets. Similarly, a government could use monetary policy to contract the economy without worrying about the need to maintain parity. Trade Balance Adjustments

Under the Bretton Woods system, if a country developed a permanent deficit in its balance of trade (importing more than it exported) that could not be corrected by domestic policy, this would require the IMF to agree to a currency devaluation. Critics of this system argue that the adjustment mechanism works much more smoothly under a floating exchange rate regime. They argue that if a country is running a trade deficit, the imbalance between the supply and demand of that country's currency in the foreign exchange markets (supply exceeding demand) will lead to depreciation in its exchange rate. In turn, by making its exports cheaper and its imports more expensive, an exchange rate depreciation should correct the trade deficit.

The Case for Fixed Exchange Rates

The case for fixed exchange rates rests on arguments about monetary discipline, speculation, uncertainty, and the lack of connection between the trade balance and exchange rates.

Monetary Discipline

We have already discussed the nature of monetary discipline inherent in a fixed exchange rate system when we discussed the Bretton Woods system. The need to maintain a fixed exchange rate parity ensures that governments do not expand their money supplies at inflationary rates. While advocates of floating rates argue that each country should be allowed to choose its own inflation rate (the monetary autonomy argument), advocates of fixed rates argue that governments all too often give in to political pressures and expand the monetary supply far too rapidly, causing unacceptably high price inflation. A fixed exchange rate regime will ensure that this does not occur.