I.COMPARATIVE LAW, CONSTITUTIONS, POLITICS AND BUDGET SYSTEMS

Most of this book is confined to discussing the differences across countries in the budgetary provisions of constitutions and statutes. However, other legal instruments can, and do, govern budgetary processes and different countries assign different weights to the importance of constitutions, statute laws, regulations of various types, and extra-legal instruments. This part examines pertinent issues. Theory does not allow strong conclusions to be drawn. Although self-imposed budget-related norms are one way of limiting capriciousness in budget processes, the choice and combination of the legal and quasi-legal instruments intended to limit the powers and roles of specific actors in the budget processes appear arbitrary.

Budget rules, if embodied in law, are useful only if the rules are both enforceable and enforced in practice. For budget-related law, many provisions are “green lights” – they specify desirable features to be implemented by budget players. A few provisions of budget-related laws are “red lights” – rules that governments must not break. Courts are called on to make judgements for any “red light” infractions. Legal arrangements and laws for the enforcement of such rules differ widely across countries.2

Unless mandated constitutionally, the judiciary appears reluctant to enter into struggles that are inherently political in nature. Budget-related laws appear to be better confined to formalising agreements that would otherwise be respected on a voluntary basis – “self-enforcing” laws. The experience with coalition agreements in some countries suggests that voluntary pacts, if adhered to, are as effective as legally binding arrangements. Such voluntary agreements are even superior – in terms of achieving desirable fiscal objectives – to formal laws that are not respected.

Part II compares the extent to which law is used to specify budget players and processes, with a particular focus on 13 OECD member countries. Part III elaborates on which aspects of the budget system could usefully be incorporated in law, as opposed to voluntary restraints that are not legally binding. The remainder of Part I briefly examines what is meant by “budget processes”. Most of the subsequent discussion then addresses the question: “Why is the legal framework for budget systems organised so differently in OECD countries?”

2. Budget processes

2.1. Budgeting: a five-stage process

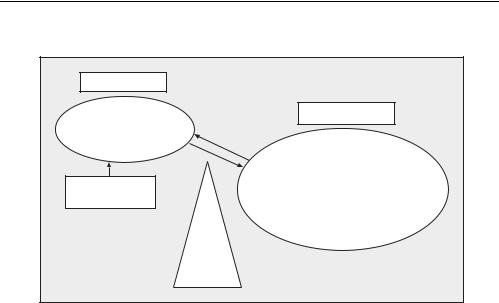

Five generic stages of annual budget processes can be identified (see Figure I.1). First the executive prepares a draft budget and submits it to the legislature. This is usually a two-step process: a Ministry of Finance (or equivalent) prepares a draft budget that incorporates the government’s expressed budget orientation; the draft budget prepared by bureaucrats is then approved by a Cabinet of ministers (or the equivalent for countries with

OECD JOURNAL ON BUDGETING – VOLUME 4 – NO. 3 – ISSN 1608-7143 – © OECD 2004 |

25 |

|

I.COMPARATIVE LAW, CONSTITUTIONS, POLITICS AND BUDGET SYSTEMS

Figure I.1. The roles of Parliament and the executive in the budget cycle

Parliament

2. Approves annual budget.

4.Controls implementation of the budget.

External audit

5.Independent audit.

The executive

1.Prepares budget (macro framework, fiscal policy strategy and priorities, detailed budget projections).

3.Executes budget (collects revenues, controls expenditures) and prepares reports for own use and for Parliament.

presidential political systems). This budget is submitted to the legislature for possible amendment and approval.

Second, at the Parliamentary stage, the budget is generally discussed in parliamentary committees, which may propose amendments. Once amendments are agreed in plenary session, the legislature approves the budget. Legal authority is provided to the executive for raising revenues if this is not ongoing. Formal adoption of the spending proposals means that legally binding upper limits are established for many expenditure categories.

The third stage is the implementation of the approved budget which is performed by the executive – and/or government agencies. In so doing, a central budget office (usually in the Ministry of Finance or the equivalent) monitors budget implementation and prepares periodic budget execution reports using a well-defined accounting system. The executive may be provided with the power to change the approved budget in the case of unforeseen emergencies, including major deviations in the macroeconomic framework underlying the budget law. A supplementary budget may be needed to confirm any such action by the executive. The executive may also be provided with other powers to modify the approved budget, including powers to change its composition (e.g. by virement or by using a reserve fund approved in the annual budget) or to control actual spending to a level below that approved, should economic circumstances dictate.

The fourth stage is parliamentary control of budget implementation. This takes place both during and, especially, after the close of the fiscal year.

26 |

OECD JOURNAL ON BUDGETING – VOLUME 4 – NO. 3 – ISSN 1608-7143 – © OECD 2004 |

|