Accounting For Dummies, 4th edition

.pdf290 Part IV: Preparing and Using Financial Reports

For a company you’ve invested in (or are considering investing in), I suggest that you do a quick read-through of the footnotes and identify the ones that seem to have the most significance. Generally, the most important footnotes are those dealing with the following matters:

Stock options awarded by the business to its executives: The additional stock shares issued under stock options dilute (thin out) the earnings per share of the business, which in turn puts downside pressure on the market value of its stock shares, assuming everything else remains the same.

Pending lawsuits, litigation, and investigations by government agencies: These intrusions into the normal affairs of the business can have enormous consequences.

Employee retirement and other post-retirement benefit plans: Your main concerns here should be whether these future obligations of the business are seriously underfunded. I have to warn you that this particular footnote is one of the most complex pieces of communication you’ll ever encounter. Good luck.

Debt problems: It’s not unusual for companies to get into problems with their debt. Debt contracts with lenders can be very complex and are financial straitjackets in some ways. A business may fall behind in making interest and principal payments on one or more of its debts, which triggers provisions in the debt contracts that give its lenders various options to protect their rights. Some debt problems are normal, but in certain cases lenders can threaten drastic action against a business, which should be discussed in its footnotes.

Segment information for the business: Public businesses have to report information for the major segments of the organization — sales and operating profit by territories or product lines. This gives a better glimpse of the different parts making up the whole business. (Segment information may be reported elsewhere in an annual financial report than in the footnotes, or you may have to go to the SEC filings of the business to find this information.)

These are a few of the important pieces of information you should look for in footnotes. But you have to stay alert for other critical matters that a business may disclose in its footnotes, so I suggest scanning each and every footnote for potentially important information. Finding a footnote that discusses a major lawsuit against the business, for example, may make the stock too risky for your stock portfolio.

Chapter 13: How Lenders and Investors Read a Financial Report 291

Checking for Ominous Skies in the Auditor’s Report

The value of analyzing a financial report depends on the accuracy of the report’s numbers. Understandably, top management wants to present the best possible picture of the business in its financial report. The managers have a vested interest in the profit performance and financial condition of the business; their yearly bonuses usually depend on recorded profit, for instance. As I mention several times in this book, the top managers and their accountants prepare the financial statements of the business and write the footnotes. This situation is somewhat like the batter in a baseball game calling the strikes and balls. Where’s the umpire?

Independent CPA auditors are like umpires in the financial reporting game. The CPA comes in, does an audit of the business’s accounting system and methods, and gives a report that is attached to the company’s financial statements.

Publicly owned businesses are required to have their annual financial reports audited by independent CPA firms, and many privately owned businesses have audits done, too, because they know that an audit report adds credibility to the financial report.

What if a private business’s financial report doesn’t include an audit report? Well, you have to trust that the business prepared accurate financial statements following authoritative accounting and financial reporting standards and that the footnotes to the financial statements cover all important points and issues.

Unfortunately, the audit report gets short shrift in financial statement analysis, maybe because it’s so full of technical terminology and accountant doublespeak. But even though audit reports are a tough read, anyone who reads and analyzes financial reports should definitely read the audit report. Chapter 15 provides more information on audits and the auditor’s report.

The auditor judges whether the business’s accounting methods are in accordance with appropriate accounting and financial reporting standards — generally accepted accounting principles (GAAP) for businesses in the United States. In most cases, the auditor’s report confirms that everything is hunkydory, and you can rely on the financial report. However, sometimes an auditor waves a yellow flag — and in extreme cases, a red flag. Here are the two important warnings to watch out for in an audit report:

The business’s capability to continue normal operations is in doubt because of what are known as financial exigencies, which may mean a low cash balance, unpaid overdue liabilities, or major lawsuits that the business doesn’t have the cash to cover.

292 Part IV: Preparing and Using Financial Reports

One or more of the methods used in the report are not in complete agreement with appropriate accounting standards, leading the auditor to conclude that the numbers reported are misleading or that disclosure is inadequate. (Look for language in the auditor’s report to this effect.)

Although auditor warnings don’t necessarily mean that a business is going down the tubes, they should turn on that light bulb in your head and make you more cautious and skeptical about the financial report. The auditor is questioning the very information on which the business’s value is based, and you can’t take that kind of thing lightly.

Also, just because a business has a clean audit report doesn’t mean that the financial report is completely accurate and aboveboard. As I discuss in Chapter 15, auditors don’t always catch everything, and they sometimes fail to discover major accounting fraud. Also, the implementation of accounting methods is fairly flexible, leaving room for interpretation and creativity that’s just short of cooking the books (deliberately defrauding and misleading readers of the financial report). Some massaging of the numbers is tolerated, which may mean that what you see on the financial report isn’t exactly an untarnished picture of the business. I explain window dressing and profit smoothing — two common examples of massaging the numbers — in Chapter 12.

Chapter 14

How Business Managers Use

a Financial Report

In This Chapter

Recognizing the limits of external financial statements

Locating detailed financial condition information

Identifying more in-depth profit information

Looking for additional cash flow information

If you’re a business manager, I strongly suggest that you read Chapter 13 before continuing with this one. Chapter 13 discusses how a business’s

lenders and investors read its financial reports. These stakeholders are entitled to regular financial reports so they can determine whether the business is making good use of their money. The chapter explains key ratios that the external stakeholders can use for interpreting the financial condition and profit performance of a business.

Business managers should understand the financial statement ratios in Chapter 13. Every ratio does double duty; it’s useful to business lenders and investors and equally useful to business managers. For example, the profit ratio and return on assets ratio are extraordinarily important to both the external stakeholders and the managers of a business — the first measures the profit yield from sales revenue, and the second measures profit on the assets employed by the business.

But as important as they are, the external financial statements do not provide all the accounting information that managers need to plan and control the financial affairs of a business. Managers need additional information. Managers who look no further than the external financial statements are being very shortsighted — they don’t have all the information they need to do their jobs. The accounts reported in external financial statements are like the table of contents of a book; each account is like a chapter title. Managers need to do more than skim chapter titles. As the radio personality Paul Harvey would say, managers need to look at the rest of the story.

294 Part IV: Preparing and Using Financial Reports

This chapter looks behind the accounts reported in the external financial statements. I explain the types of additional accounting information that managers need in order to control financial condition and performance, and to plan the financial future of a business.

Building on the Foundation of the External Financial Statements

Managers are problems solvers. Every business has some problems, perhaps even some serious ones. However, external financial statements are not designed to expose those problems. Except in extreme cases — in which the business is obviously in dire financial straits — you’d never learn about its problems just from reading its external financial statements. To borrow lyrics from an old Bing Crosby song, external financial statements are designed to “accentuate the positive, eliminate the negative . . . [and] don’t mess with Mister In-Between.”

Seeking out problems and opportunities

Business managers need more accounting information than what’s disclosed in external financial statements for two basic purposes:

To alert them to problems that exist or may be emerging that threaten the profit performance, cash flow, and financial condition of the business

To suggest opportunities for improving the financial performance and health of the business

A popular expression these days is “mining the data.” The accounting system of a business is a rich mother lode of management information, but you have to dig that information out of the accounting database. Working with the controller (chief accountant), a manager should decide what information she needs beyond what is reported in the external financial statements.

Avoiding information overload

Business manages are very busy people. Nothing is more frustrating than getting reams of information that you have no use for. For that reason, the controller should guard carefully against information overload. While some types of accounting information should stream to business managers on a regular basis, other types should be provided only on as as-needed basis.

Chapter 14: How Business Managers Use a Financial Report 295

Ideally, the controller reads the mind of every manager and provides exactly the accounting information that each manager needs. In practice, that can’t always happen, of course. A manager may not be certain about which information she needs and which she doesn’t. The flow of information has to be worked out over time.

Furthermore, how to communicate the information is open to debate and individual preferences. Some of the additional management information can be put in the main body of an accounting report, but most is communicated in supplemental schedules, graphs, and commentary. The information may be delivered to the manager’s computer, or the manager may be given the option to call up selected information from the accounting database of the business.

My point is simply this: Managers and controllers must communicate — early and often — to make sure managers get what they need without being swamped with unnecessary data. No one wants to waste precious time compiling reports that are never read. So before a controller begins the process of compiling accounting information for managers’ eyes only, be sure there’s ample communication about what each manager needs.

Gathering Financial

Condition Information

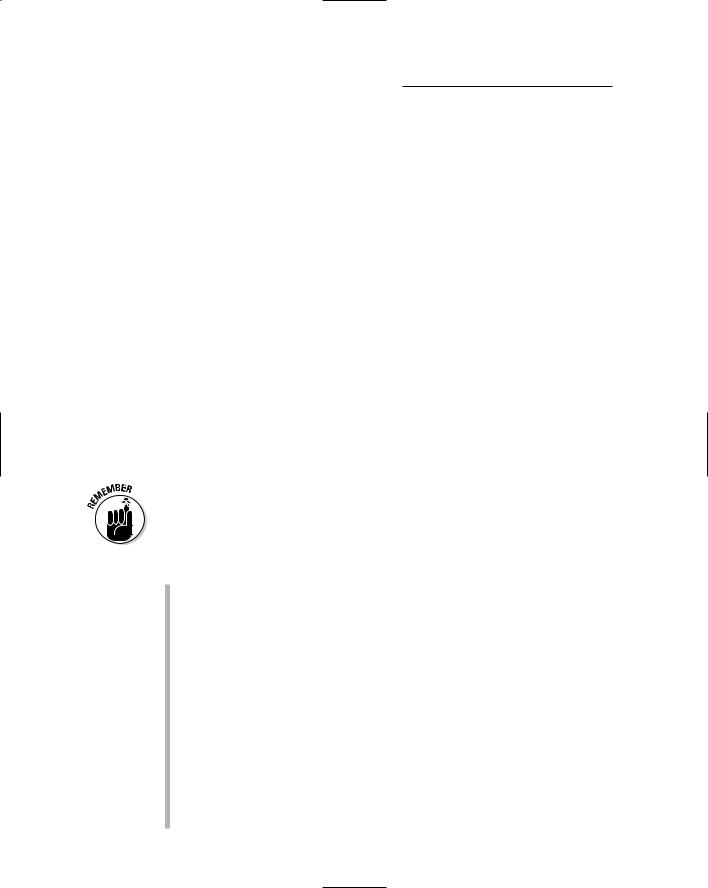

The balance sheet — one of three primary financial statements included in a financial report — summarizes the financial condition of the business. Figure 14-1 lists the basic accounts in a balance sheet, without dollar amounts for the accounts and without subtotals and totals. Just 12 accounts are given in Figure 14-1: five assets (counting fixed assets and accumulated depreciation as only one account), five liabilities, and two owners’ equity accounts. A business may report more than just these 12 accounts. For instance, a business may invest in marketable securities, or have receivables from loans made to officers of the business. A business may have intangible assets. A business corporation may issue more than one class of capital stock and would report a separate account for each class. And so on. The idea of Figure 14-1 is to focus on the core assets and liabilities of a typical business.

296 Part IV: Preparing and Using Financial Reports

|

Assets |

Liabilities |

|

Cash |

Accounts payable |

|

Accounts receivable |

Accrued expenses payable |

|

Inventory |

Income tax payable |

|

Prepaid expenses |

Short-term notes payable |

|

Fixed assets |

Long-term notes payable |

|

||

Figure 14-1: |

||

Hardcore |

Accumulated depreciation |

|

accounts |

|

|

reported in |

|

Owners’ Equity |

a balance |

|

Invested capital |

sheet. |

|

|

|

|

Retained earnings |

|

|

Cash

The external balance sheet reports just one cash account. But many businesses keep several bank checking and deposit accounts, and some (such as gambling casinos and food supermarkets) keep a fair amount of currency on hand. A business may have foreign bank deposits in euros, English pounds, or other currencies. Most businesses set up separate checking accounts for payroll; only payroll checks are written against these accounts.

Managers should monitor the balances in every cash account in order to control and optimize the deployment of their cash resources. So, information about each bank account should be reported to the manager.

Managers should ask these questions regarding cash:

Is the ending balance of cash the actual amount at the balance sheet date, or did the business engage in window dressing in order to inflate its ending cash balance? Window dressing refers to holding the books open after the ending balance sheet date in order to record additional cash inflow as if the cash was received on the last day of the period. Window dressing is not uncommon. (For more details, see Chapter 12.) If window dressing has gone on, the manager should know the true, actual ending cash balance of the business.

Were there any cash out days during the year? In other words, did the company’s cash balance actually fall to zero (or near zero) during the year? How often did this happen? Is there a seasonal fluctuation in cash flow that causes “low tide” for cash, or are the cash out days due to running the business with too little cash?

Are there any limitations on the uses of cash imposed by loan covenants by the company’s lenders? Do any of the loans require compensatory balances that require that the business keep a minimum balance relative

Chapter 14: How Business Managers Use a Financial Report 297

to the loan balance? In this situation the cash balance is not fully available for general operating purposes.

Are there any out-of-the-ordinary demands on cash? For example, a business may have entered into buyout agreements with a key shareholder or with a vendor to escape the terms of an unfavorable contract. Any looming demands on cash should be reported to managers.

Accounts receivable

A business that makes sales on credit has the accounts receivable asset — unless it has collected all its customers’ receivables by the end of the year, which is not very likely. To be more correct, the business has hundreds or thousands of individual accounts receivable from its credit customers. In its external balance sheet, a business reports just one summary amount for all its accounts receivable. However, this total amount is not nearly enough information for the business manager.

Here are questions a manager should ask about accounts receivable:

Of the total amount of accounts receivable, how much is current (within the normal credit terms offered to customers), slightly past due, and seriously past due? A past due receivable causes a delay in cash flow and increases the risk of it becoming a bad debt (a receivable that ends up being partially or wholly uncollectible).

Has an adequate amount been recorded for bad debts? Is the company’s method for determining its bad debts expense consistent year to year? Was the estimate of bad debts this period tweaked in order to boost or dampen profit for the period? Has the IRS raised any questions about the company’s method for writing off bad debts? (Chapter 7 discusses bad debts expense.)

Who owes the most money to the business? (The manager should receive a schedule of customers that shows this information.) Which customers are the slowest payers? Do the sales prices to these customers take into account that they typically do not pay on time?

It’s also useful to know which customers pay quickly to take advantage of prompt payment discounts. In short, the payment profiles of credit customers are important information for managers.

Are there “stray” receivables buried in the accounts receivable total? A business may loan money to its managers and employees or to other businesses. There may be good business reasons for such loans. In any case, these receivables should not be included with accounts receivable, which should be reserved for receivables from credit sales to customers. Other receivables should be listed in a separate schedule.

298 Part IV: Preparing and Using Financial Reports

Inventory

For businesses that sell products, inventory is typically a major asset. It’s also typically the most problematic asset from both the management and accounting points of view. First off, the manager should understand the accounting method being used to determine the cost of inventory and the cost of goods sold expense. (You may want to quickly review the section in Chapter 7 that covers this topic.) In particular, the manager should have a good feel regarding whether the accounting method results in conservative or liberal profit measures.

Managers should ask these questions regarding inventory:

How long, on average, do products remain in the warehouse before they are sold? The manager should receive a turnover analysis of inventory that clearly exposes the holding periods of products. Slow-moving products cause nothing but problems. The manager should ferret out products that have been held in inventory too long. The cost of these sluggish products may have to be written down or written off, and the manager has to authorize these accounting entries. The manager should review the sales demand for slow-moving products, of course.

If the business uses the LIFO method (last-in, first-out), was there a LIFO liquidation gain during the period that caused an artificial and one-time boost in profit for the year? (I explain this aspect of the LIFO method in Chapter 7.)

The manager should also request these reports:

Inventory reports that include side-by-side comparison of the costs and the sales prices of products (or at least the major products sold by the business). It’s helpful to include the mark-up percent for each product, which allows the manager to focus on mark-up percent differences from product to product.

Regular reports summarizing major product cost changes during the period, and forecasts of near-term changes. It may be useful to report the current replacement cost of inventory assuming it’s feasible to determine this amount.

Prepaid expenses

Generally, the business manager doesn’t need too much additional information on this asset. However, there may be a major decrease or increase in this asset from a year ago that is not consistent with the growth or decline in sales from year to year. The manager should pay attention to an abnormal change in the asset. Perhaps a new type of cost has to be prepaid now, such as insurance

Chapter 14: How Business Managers Use a Financial Report 299

coverage for employee safety triggered by an OSHA audit of the employee working conditions in the business. A brief schedule of the major types of prepaid expenses is useful.

Fixed assets and accumulated depreciation

Fixed assets is the all-inclusive term for the wide range of long-term operating assets used by a business — from buildings and heavy machinery to office furniture. Except for the cost of land, the cost of a fixed asset is spread over its estimated useful life to the business; the amount allocated to each period is called depreciation expense. The manager should know the company’s accounting policy regarding which fixed assets are capitalized (the cost is recorded in a fixed asset account) and which are expensed immediately (the cost is recorded entirely to expense at the time of purchase).

Most businesses adopt a cost limit below which minor fixed assets (a screwdriver, stapler, or wastebasket, for example) are recorded to expense instead of being depreciated over some number of years. The controller should alert the manager if an unusually high amount of these small cost fixed assets were charged off to expense during the year, which could have a significant impact on the bottom line.

The manager should be aware of the general accounting policies of the business regarding estimating useful lives of fixed assets and whether the straight-line or accelerated methods of allocation are used. Indeed, the manager should have a major voice in deciding these policies, and not simply defer to the controller. In Chapter 7, I explain these accounting issues.

Using accelerated depreciation methods may result in certain fixed assets that are fully depreciated. These assets should be reported to the manager — even though they have a zero book value — so the manager is aware that these fixed assets are still being used but no depreciation expense is being recorded for their use.

Generally, the manager does not need to know the current replacement costs of all fixed assets — just those that will be replaced in the near future. At the same time, it is useful for the manager to get a status report on the company’s fixed assets, which takes more of an engineering approach than an accounting approach. The status report includes information on the capacity, operating efficiency, and projected remaining life of each major fixed asset. The status report should include leased assets that are not owned by the business and which, therefore, are not included in the fixed asset account.

The manager needs an insurance summary report for all fixed assets that are (or should be) insured for fire and other casualty losses, which lists the types of coverage on each major fixed asset, deductibles, claims during the year,